BISICHI MINING PLC ANNUAL REPORT 2017

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Governance Independent auditor’s report<br />

KEY AUDIT MATTER<br />

HOW THE MATTER WAS ADDRESSED IN OUR AUDIT<br />

The risk that judgments, estimates and disclosure associated with<br />

the carrying value of Ezimbokedweni and impairment charges are<br />

inappropriate.<br />

As at 31 December 2016 the group’s net investment in Ezimbokedweni<br />

Mining (Pty) Limited (“Ezimbokedweni”), an equity accounted joint venture<br />

was £1.8m. The carrying value was dependent upon the ultimate completion<br />

of a sale and purchase agreement to acquire the Pegasus coal project in<br />

South Africa, under which a deposit had been paid by Ezimbokedweni.<br />

During the year the joint venture was placed into Business Rescue under<br />

the South African Companies Act by the group’s joint venture partner. The<br />

original deposit has been returned to Ezimbokodweni and as a result, the<br />

Board consider there to be no reasonable prospect of the Pegasus coal<br />

project transactionw completing.<br />

Further to these developments, the Board performed an impairment review<br />

of the carrying value of the net investment in Ezimbokedwini and recorded<br />

an impairment of the net investment of £1.8m, with any further movements<br />

since 31 December 2016 reflecting foreign exchange differences.<br />

The assessment of the carrying value, subsequent impairment and<br />

associated disclosure represented a significant focus for our audit.<br />

Additionally, the tax treatment of this transaction was considered to be an<br />

area of risk of material misstatement. This was also considered to be an<br />

area requiring specialist knowledge and expertise.<br />

We will have made specific inquiries of management and the Board to<br />

gain an understanding of the fact pattern and events during the year<br />

regarding Ezimbokedweni.<br />

We have reviewed minutes of Board meetings, legal documents and<br />

correspondence relating to the joint venture, the Business Rescue<br />

and assessments of the resulting financial position and interests of the<br />

joint venture.<br />

We have assessed the Board’s conclusion that the net investment is<br />

impaired based on the facts and circumstances, including assessment<br />

of the probability of value being recovered from the joint venture.<br />

We have assessed the tax treatment of the transaction applied by<br />

management in conjunction with our valuation specialists and those<br />

of the component auditor in South Africa.<br />

We have assessed the accounting entries in respect of the<br />

impairment as well as the disclosures in note 13 and the Key<br />

Estimates and Judgments note.<br />

Our findings<br />

We consider the judgements made by management relating to the impairment recorded by the group to be appropriate based on the<br />

developments during the year. We consider the disclosures at note 13 and the Key Estimates and Judgments note to be acceptable.<br />

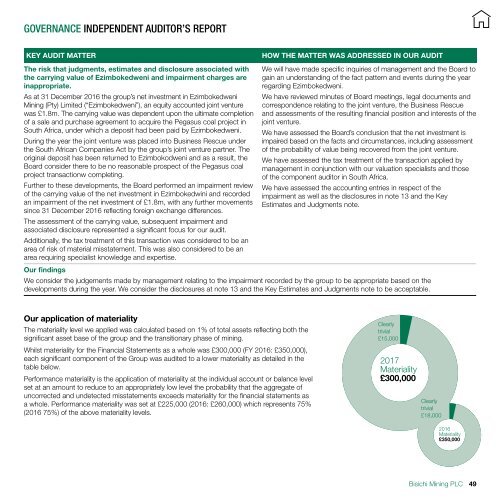

Our application of materiality<br />

The materiality level we applied was calculated based on 1% of total assets reflecting both the<br />

significant asset base of the group and the transitionary phase of mining.<br />

Whilst materiality for the Financial Statements as a whole was £300,000 (FY 2016: £350,000),<br />

each significant component of the Group was audited to a lower materiality as detailed in the<br />

table below.<br />

Performance materiality is the application of materiality at the individual account or balance level<br />

set at an amount to reduce to an appropriately low level the probability that the aggregate of<br />

uncorrected and undetected misstatements exceeds materiality for the financial statements as<br />

a whole. Performance materiality was set at £225,000 (2016: £260,000) which represents 75%<br />

(2016 75%) of the above materiality levels.<br />

Clearly<br />

trivial<br />

£15,000<br />

<strong>2017</strong><br />

Materiality<br />

£300,000<br />

Clearly<br />

trivial<br />

£18,000<br />

2016<br />

Materiality<br />

£350,000<br />

Bisichi Mining <strong>PLC</strong><br />

49