You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

FULL REPORT NOW AVAILABLE VIA<br />

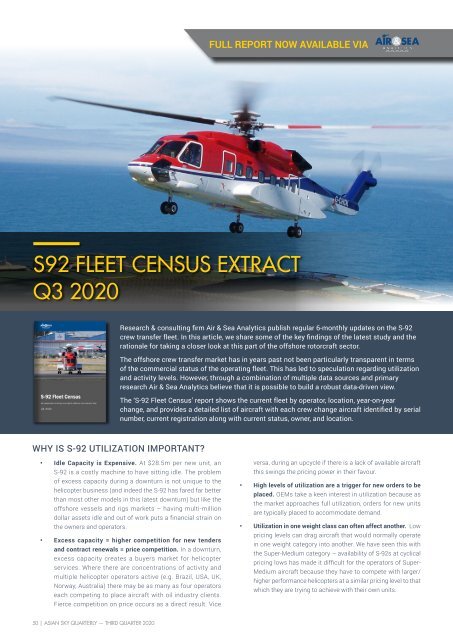

S92 FLEET CENSUS EXTRACT<br />

<strong>Q3</strong> <strong>2020</strong><br />

Research & consulting firm Air & Sea Analytics publish regular 6-monthly updates on the S-92<br />

crew transfer fleet. In this article, we share some of the key findings of the latest study and the<br />

rationale for taking a closer look at this part of the offshore rotorcraft sector.<br />

The offshore crew transfer market has in years past not been particularly transparent in terms<br />

of the commercial status of the operating fleet. This has led to speculation regarding utilization<br />

and activity levels. However, through a combination of multiple data sources and primary<br />

research Air & Sea Analytics believe that it is possible to build a robust data-driven view.<br />

The ‘S-92 Fleet Census’ report shows the current fleet by operator, location, year-on-year<br />

change, and provides a detailed list of aircraft with each crew change aircraft identified by serial<br />

number, current registration along with current status, owner, and location.<br />

WHY IS S-92 UTILIZATION IMPORTANT?<br />

• Idle Capacity is Expensive. At $28.5m per new unit, an<br />

S-92 is a costly machine to have sitting idle. The problem<br />

of excess capacity during a downturn is not unique to the<br />

helicopter business (and indeed the S-92 has fared far better<br />

than most other models in this latest downturn) but like the<br />

offshore vessels and rigs markets – having multi-million<br />

dollar assets idle and out of work puts a financial strain on<br />

the owners and operators.<br />

• Excess capacity = higher competition for new tenders<br />

and contract renewals = price competition. In a downturn,<br />

excess capacity creates a buyers market for helicopter<br />

services. Where there are concentrations of activity and<br />

multiple helicopter operators active (e.g. Brazil, USA, UK,<br />

Norway, Australia) there may be as many as four operators<br />

each competing to place aircraft with oil industry clients.<br />

Fierce competition on price occurs as a direct result. Vice<br />

versa, during an upcycle if there is a lack of available aircraft<br />

this swings the pricing power in their favour.<br />

• High levels of utilization are a trigger for new orders to be<br />

placed. OEMs take a keen interest in utilization because as<br />

the market approaches full utilization, orders for new units<br />

are typically placed to accommodate demand.<br />

• Utilization in one weight class can often affect another. Low<br />

pricing levels can drag aircraft that would normally operate<br />

in one weight category into another. We have seen this with<br />

the Super-Medium category – availability of S-92s at cyclical<br />

pricing lows has made it difficult for the operators of Super-<br />

Medium aircraft because they have to compete with larger/<br />

higher performance helicopters at a similar pricing level to that<br />

which they are trying to achieve with their own units.<br />

50 | ASIAN SKY QUARTERLY — THIRD QUARTER <strong>2020</strong>