Manual para la Gestión Empresarial de las ... - CRECEmype

Manual para la Gestión Empresarial de las ... - CRECEmype

Manual para la Gestión Empresarial de las ... - CRECEmype

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Ministerio<br />

<strong>de</strong> <strong>la</strong> Producción<br />

Schweizerische Eidgenossenschaft<br />

Confédération suisse<br />

Confédérazione Svizzera<br />

Confédéraziun svizra<br />

Agencia Suiza <strong>para</strong> el <strong>de</strong>sarrollo<br />

y <strong>la</strong> cooperación COSUDE<br />

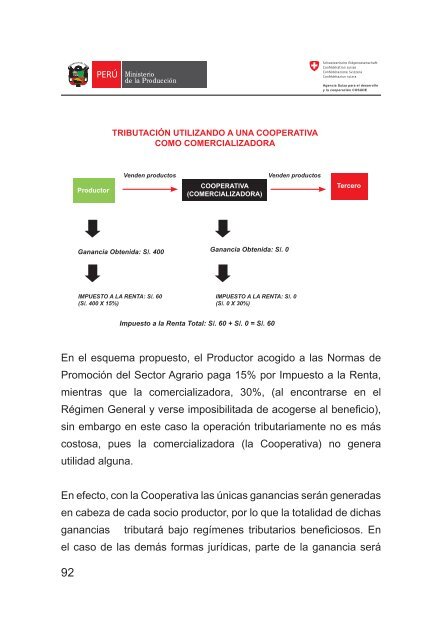

TRIBUTACIÓN UTILIZANDO A UNA COOPERATIVA<br />

COMO COMERCIALIZADORA<br />

Productor<br />

Ven<strong>de</strong>n productos<br />

Ven<strong>de</strong>n productos<br />

COOPERATIVA<br />

(COMERCIALIZADORA)<br />

Tercero<br />

Ganancia Obtenida: S/. 400<br />

Ganancia Obtenida: S/. 0<br />

IMPUESTO A LA RENTA: S/. 60<br />

(S/. 400 X 15%)<br />

IMPUESTO A LA RENTA: S/. 0<br />

(S/. 0 X 30%)<br />

Impuesto a <strong>la</strong> Renta Total: S/. 60 + S/. 0 = S/. 60<br />

En el esquema propuesto, el Productor acogido a <strong>la</strong>s Normas <strong>de</strong><br />

Promoción <strong>de</strong>l Sector Agrario paga 15% por Impuesto a <strong>la</strong> Renta,<br />

mientras que <strong>la</strong> comercializadora, 30%, (al encontrarse en el<br />

Régimen General y verse imposibilitada <strong>de</strong> acogerse al beneficio),<br />

sin embargo en este caso <strong>la</strong> operación tributariamente no es más<br />

costosa, pues <strong>la</strong> comercializadora (<strong>la</strong> Cooperativa) no genera<br />

utilidad alguna.<br />

En efecto, con <strong>la</strong> Cooperativa <strong>la</strong>s únicas ganancias serán generadas<br />

en cabeza <strong>de</strong> cada socio productor, por lo que <strong>la</strong> totalidad <strong>de</strong> dichas<br />

ganancias tributará bajo regímenes tributarios beneficiosos. En<br />

el caso <strong>de</strong> <strong>la</strong>s <strong>de</strong>más formas jurídicas, parte <strong>de</strong> <strong>la</strong> ganancia será<br />

92