Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

NOTES<br />

1<br />

2<br />

3<br />

4<br />

5<br />

6<br />

7<br />

8<br />

9<br />

10<br />

11<br />

12<br />

13<br />

14<br />

15<br />

16<br />

17<br />

18<br />

19<br />

20<br />

21<br />

22<br />

23<br />

24<br />

25<br />

26<br />

27<br />

28<br />

29<br />

30<br />

31<br />

32<br />

33<br />

34<br />

35<br />

36<br />

37<br />

38<br />

39<br />

40<br />

41<br />

42<br />

43<br />

44<br />

45<br />

46<br />

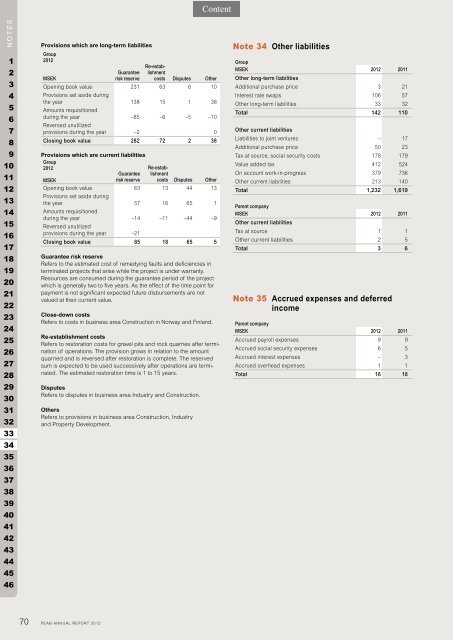

Provisions which are long-term liabilities<br />

Group<br />

<strong>2012</strong><br />

MSEK<br />

Guarantee<br />

risk reserve<br />

Re-establishment<br />

costs Disputes Other<br />

Opening book value<br />

Provisions set aside during<br />

231 63 6 10<br />

the year<br />

Amounts requisitioned<br />

138 15 1 38<br />

during the year<br />

Reversed unutilized<br />

–85 –6 –5 –10<br />

provisions during the year –2 0<br />

Closing book value 282 72 2 38<br />

Provisions which are current liabilities<br />

Group<br />

<strong>2012</strong><br />

MSEK<br />

Guarantee<br />

risk reserve<br />

Re-establishment<br />

costs Disputes Other<br />

Opening book value<br />

Provisions set aside during<br />

63 13 44 13<br />

the year<br />

Amounts requisitioned<br />

57 16 65 1<br />

during the year<br />

Reversed unutilized<br />

–14 –11 –44 –9<br />

provisions during the year –21<br />

Closing book value 85 18 65 5<br />

Guarantee risk reserve<br />

Refers to the estimated cost of remedying faults and deficiencies in<br />

terminated projects that arise while the project is under warranty.<br />

Resources are consumed during the guarantee period of the project<br />

which is generally two to five years. As the effect of the time point for<br />

payment is not significant expected future disbursements are not<br />

valued at their current value.<br />

Close-down costs<br />

Refers to costs in business area Construction in Norway and Finland.<br />

Re-establishment costs<br />

Refers to restoration costs for gravel pits and rock quarries after termination<br />

of operations. The provision grows in relation to the amount<br />

quarried and is reversed after restoration is complete. The reserved<br />

sum is expected to be used successively after operations are terminated.<br />

The estimated restoration time is 1 to 15 years.<br />

Disputes<br />

Refers to disputes in business area Industry and Construction.<br />

Others<br />

Refers to provisions in business area Construction, Industry<br />

and Property Development.<br />

70 PEAB ANNUAL REPORT <strong>2012</strong><br />

Note 34 Other liabilities<br />

Group<br />

MSEK<br />

Other long-term liabilities<br />

<strong>2012</strong> 2011<br />

Additional purchase price 3 21<br />

Interest rate swaps 106 57<br />

Other long-term liabilities 33 32<br />

Total 142 110<br />

Other current liabilities<br />

Liabilities to joint ventures – 17<br />

Additional purchase price 50 23<br />

Tax at source, social security costs 178 179<br />

Value added tax 412 524<br />

On account work-in-progress 379 736<br />

Other current liabilities 213 140<br />

Total 1,232 1,619<br />

Parent company<br />

MSEK<br />

Other current liabilities<br />

<strong>2012</strong> 2011<br />

Tax at source 1 1<br />

Other current liabilities 2 5<br />

Total 3 6<br />

Note 35 Accrued expenses and deferred<br />

income<br />

Parent company<br />

MSEK <strong>2012</strong> 2011<br />

Accrued payroll expenses 9 9<br />

Accrued social security expenses 6 5<br />

Accrued interest expenses – 3<br />

Accrued overhead expenses 1 1<br />

Total 16 18