Promoting Financial Inclusion - United Nations Development ...

Promoting Financial Inclusion - United Nations Development ...

Promoting Financial Inclusion - United Nations Development ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

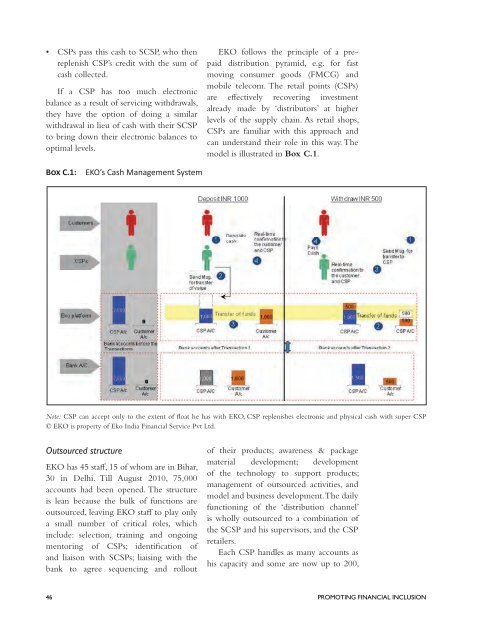

• CSPs pass this cash to SCSP, who then<br />

replenish CSP’s credit with the sum of<br />

cash collected.<br />

If a CSP has too much electronic<br />

balance as a result of servicing withdrawals,<br />

they have the option of doing a similar<br />

withdrawal in lieu of cash with their SCSP<br />

to bring down their electronic balances to<br />

optimal levels.<br />

EKO follows the principle of a prepaid<br />

distribution pyramid, e.g. for fast<br />

moving consumer goods (FMCG) and<br />

mobile telecom. The retail points (CSPs)<br />

are effectively recovering investment<br />

already made by ‘distributors’ at higher<br />

levels of the supply chain. As retail shops,<br />

CSPs are familiar with this approach and<br />

can understand their role in this way. The<br />

model is illustrated in Box C.1.<br />

BOX C.1:<br />

EKO’s Cash Management System<br />

Note: CSP can accept only to the extent of float he has with EKO, CSP replenishes electronic and physical cash with super CSP<br />

© EKO is property of Eko India <strong>Financial</strong> Service Pvt Ltd.<br />

Outsourced structure<br />

EKO has 45 staff, 15 of whom are in Bihar,<br />

30 in Delhi. Till August 2010, 75,000<br />

accounts had been opened. The structure<br />

is lean because the bulk of functions are<br />

outsourced, leaving EKO staff to play only<br />

a small number of critical roles, which<br />

include: selection, training and ongoing<br />

mentoring of CSPs; identification of<br />

and liaison with SCSPs; liaising with the<br />

bank to agree sequencing and rollout<br />

of their products; awareness & package<br />

material development; development<br />

of the technology to support products;<br />

management of outsourced activities, and<br />

model and business development. The daily<br />

functioning of the ‘distribution channel’<br />

is wholly outsourced to a combination of<br />

the SCSP and his supervisors, and the CSP<br />

retailers.<br />

Each CSP handles as many accounts as<br />

his capacity and some are now up to 200,<br />

46 PROMOTING FINANCIAL INCLUSION