Economic crime report 2004 - Ekobrottsmyndigheten

Economic crime report 2004 - Ekobrottsmyndigheten

Economic crime report 2004 - Ekobrottsmyndigheten

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

tion, normally at the retail level, does taxation come into play. Approved<br />

warehousers and registered consignees have the exclusive right to handle<br />

products under suspension.<br />

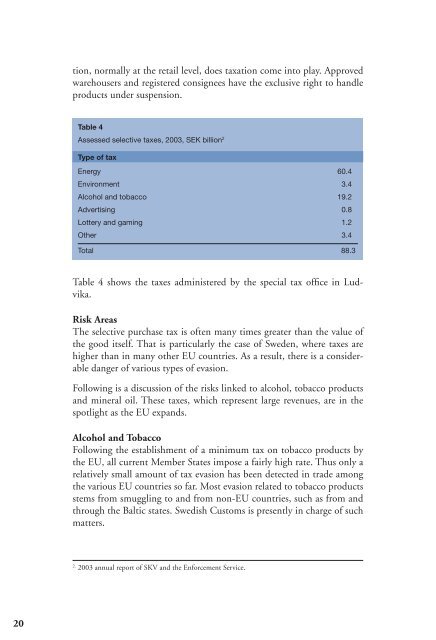

Table 4<br />

Assessed selective taxes, 2003, SEK billion 2<br />

Type of tax<br />

Energy 60.4<br />

Environment 3.4<br />

Alcohol and tobacco 19.2<br />

Advertising 0.8<br />

Lottery and gaming 1.2<br />

Other 3.4<br />

Total 88.3<br />

Table 4 shows the taxes administered by the special tax office in Ludvika.<br />

Risk Areas<br />

The selective purchase tax is often many times greater than the value of<br />

the good itself. That is particularly the case of Sweden, where taxes are<br />

higher than in many other EU countries. As a result, there is a considerable<br />

danger of various types of evasion.<br />

Following is a discussion of the risks linked to alcohol, tobacco products<br />

and mineral oil. These taxes, which represent large revenues, are in the<br />

spotlight as the EU expands.<br />

Alcohol and Tobacco<br />

Following the establishment of a minimum tax on tobacco products by<br />

the EU, all current Member States impose a fairly high rate. Thus only a<br />

relatively small amount of tax evasion has been detected in trade among<br />

the various EU countries so far. Most evasion related to tobacco products<br />

stems from smuggling to and from non-EU countries, such as from and<br />

through the Baltic states. Swedish Customs is presently in charge of such<br />

matters.<br />

2.<br />

2003 annual <strong>report</strong> of SKV and the Enforcement Service.<br />

20