Price Determination in the Australian Food Industry A Report

Price Determination in the Australian Food Industry A Report

Price Determination in the Australian Food Industry A Report

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

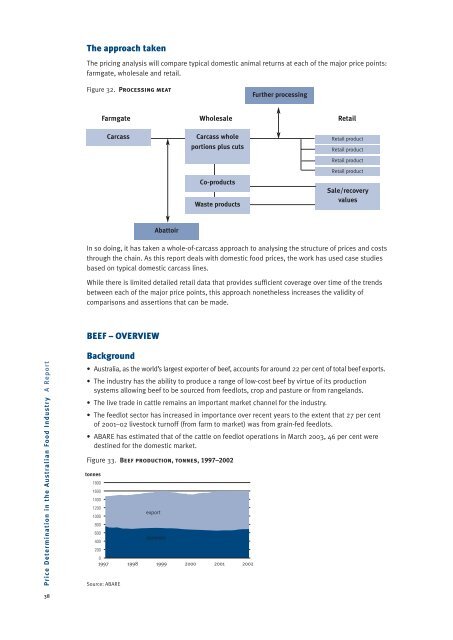

The approach taken<br />

The pric<strong>in</strong>g analysis will compare typical domestic animal returns at each of <strong>the</strong> major price po<strong>in</strong>ts:<br />

farmgate, wholesale and retail.<br />

Figure 32. Process<strong>in</strong>g meat<br />

Fur<strong>the</strong>r process<strong>in</strong>g<br />

Farmgate Wholesale Retail<br />

Carcass<br />

Carcass whole<br />

portions plus cuts<br />

Co-products<br />

Waste products<br />

Retail product<br />

Retail product<br />

Retail product<br />

Retail product<br />

Sale/recovery<br />

values<br />

Abattoir<br />

In so do<strong>in</strong>g, it has taken a whole-of-carcass approach to analys<strong>in</strong>g <strong>the</strong> structure of prices and costs<br />

through <strong>the</strong> cha<strong>in</strong>. As this report deals with domestic food prices, <strong>the</strong> work has used case studies<br />

based on typical domestic carcass l<strong>in</strong>es.<br />

While <strong>the</strong>re is limited detailed retail data that provides sufficient coverage over time of <strong>the</strong> trends<br />

between each of <strong>the</strong> major price po<strong>in</strong>ts, this approach none<strong>the</strong>less <strong>in</strong>creases <strong>the</strong> validity of<br />

comparisons and assertions that can be made.<br />

BEEF – OVERVIEW<br />

Background<br />

<strong>Price</strong> <strong>Determ<strong>in</strong>ation</strong> <strong>in</strong> <strong>the</strong> <strong>Australian</strong> <strong>Food</strong> <strong>Industry</strong> A <strong>Report</strong><br />

• Australia, as <strong>the</strong> world’s largest exporter of beef, accounts for around 22 per cent of total beef exports.<br />

• The <strong>in</strong>dustry has <strong>the</strong> ability to produce a range of low-cost beef by virtue of its production<br />

systems allow<strong>in</strong>g beef to be sourced from feedlots, crop and pasture or from rangelands.<br />

• The live trade <strong>in</strong> cattle rema<strong>in</strong>s an important market channel for <strong>the</strong> <strong>in</strong>dustry.<br />

• The feedlot sector has <strong>in</strong>creased <strong>in</strong> importance over recent years to <strong>the</strong> extent that 27 per cent<br />

of 2001–02 livestock turnoff (from farm to market) was from gra<strong>in</strong>-fed feedlots.<br />

• ABARE has estimated that of <strong>the</strong> cattle on feedlot operations <strong>in</strong> March 2003, 46 per cent were<br />

dest<strong>in</strong>ed for <strong>the</strong> domestic market.<br />

Figure 33. Beef production, tonnes, 1997–2002<br />

tonnes<br />

1800<br />

1600<br />

1400<br />

1200<br />

export<br />

1000<br />

800<br />

600<br />

domestic<br />

400<br />

200<br />

0<br />

1997 1998 1999 2000 2001 2002<br />

Source: ABARE<br />

38