You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

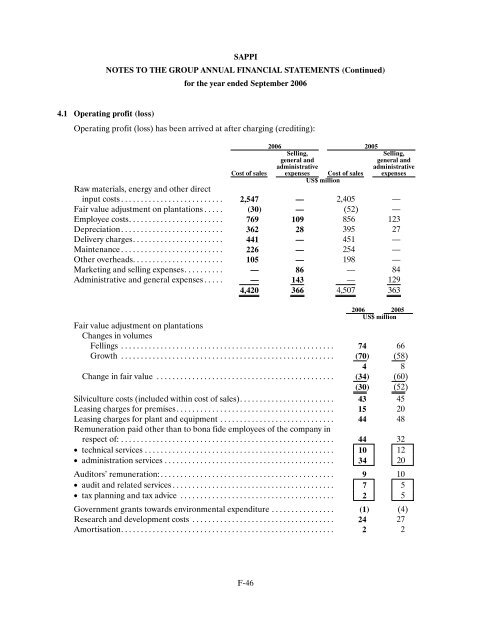

SAPPI<br />

NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS (Continued)<br />

4.1 Operating profit (loss)<br />

for the year ended September <strong><strong>20</strong>06</strong><br />

Operating profit (loss) has been arrived at after charging (crediting):<br />

<strong><strong>20</strong>06</strong> <strong>20</strong>05<br />

Selling, Selling,<br />

general and general and<br />

administrative administrative<br />

Cost of sales expenses Cost of sales expenses<br />

US$ million<br />

Raw materials, energy and other direct<br />

input costs.......................... 2,547 — 2,405 —<br />

Fair value adjustment on plantations..... (30) — (52) —<br />

Employee costs........................ 769 109 856 123<br />

Depreciation.......................... 362 28 395 27<br />

Delivery charges....................... 441 — 451 —<br />

Maintenance.......................... 226 — 254 —<br />

Other overheads....................... 105 — 198 —<br />

Marketing and selling expenses.......... — 86 — 84<br />

Administrative and general expenses..... — 143 — 129<br />

4,4<strong>20</strong> 366 4,507 363<br />

F-46<br />

<strong><strong>20</strong>06</strong> <strong>20</strong>05<br />

US$ million<br />

Fair value adjustment on plantations<br />

Changes in volumes<br />

Fellings ...................................................... 74 66<br />

Growth ...................................................... (70 ) (58 )<br />

4 8<br />

Change in fair value ............................................. (34 ) (60 )<br />

(30 ) (52 )<br />

Silviculture costs (included within cost of sales)........................ 43 45<br />

Leasing charges for premises........................................ 15 <strong>20</strong><br />

Leasing charges for plant and equipment............................. 44 48<br />

Remuneration paid other than to bona fide employees of the company in<br />

respect of:...................................................... 44 32<br />

• technical services................................................ 10 12<br />

• administration services........................................... 34 <strong>20</strong><br />

Auditors’ remuneration:............................................ 9 10<br />

• audit and related services......................................... 7 5<br />

• tax planning and tax advice ....................................... 2 5<br />

Government grants towards environmental expenditure................ (1 ) (4 )<br />

Research and development costs .................................... 24 27<br />

Amortisation...................................................... 2 2