Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

SAPPI<br />

NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS (Continued)<br />

for the year ended September <strong><strong>20</strong>06</strong><br />

21. INTEREST-BEARING BORROWINGS (Continued)<br />

Borrowing facilities secured by trade receivables<br />

<strong>Sappi</strong> Fine Paper North America<br />

<strong>Sappi</strong> sells the majority of its US$ receivables to Galleon Capital LLC on a non-recourse basis. Credit<br />

enhancement is calculated by adding up the maximum exposure of 3 % of the top four obligors, ie. 12 %<br />

(plus dilution reserve plus interest cost reserve). In addition, excess concentrations are covered with a<br />

letter of credit in favour of Galleon Capital LLC. <strong>Sappi</strong> is responsible for the collection of all amounts that<br />

are due from the customer. The rate of discounting that is charged on the receivables is LIBOR (London<br />

Inter Bank Offer Rate) plus 34 basis points.<br />

<strong>Sappi</strong> Fine Paper Europe<br />

<strong>Sappi</strong> sells the majority of its EUR denominated receivables to a SPE that is managed by State Street<br />

Bank. State Street then on sells these receivables to Galleon Capital LLC on a non-recourse basis. A letter<br />

of credit has been issued by <strong>Sappi</strong> to Galleon Capital LLC which guarantees in the event of default by a<br />

customer. The discounting fee payable to State Street is 14%. <strong>Sappi</strong> is responsible for the collection of all<br />

amounts that are due from the customer. The rate of discounting that is charged on the receivables is<br />

EURIBOR (European Inter Bank Offer Rate) plus 36 basis points.<br />

<strong>Sappi</strong> Trading<br />

<strong>Sappi</strong> sells the majority of its US$ denominated receivables to a SPE that is managed by State Street<br />

Bank. State Street then on sells these receivables to Galleon Capital LLC on a non-recourse basis. A letter<br />

of credit has been issued by <strong>Sappi</strong> to Galleon Capital LLC which guarantees in the event of default by a<br />

customer. The discounting fee payable to State Street is 14%. <strong>Sappi</strong> is responsible for the collection of all<br />

amounts that are due from the customer. The rate of discounting that is charged on the receivables is<br />

LIBOR (London Inter Bank Offer Rate) plus 42 basis points.<br />

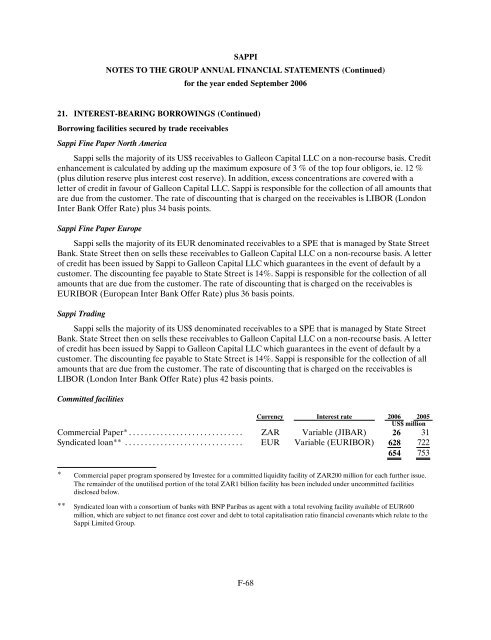

Committed facilities<br />

Currency Interest rate <strong><strong>20</strong>06</strong> <strong>20</strong>05<br />

US$ million<br />

Commercial Paper*............................. ZAR Variable (JIBAR) 26 31<br />

Syndicated loan** .............................. EUR Variable (EURIBOR) 628 722<br />

654 753<br />

* Commercial paper program sponsered by Investec for a committed liquidity facility of ZAR<strong>20</strong>0 million for each further issue.<br />

The remainder of the unutilised portion of the total ZAR1 billion facility has been included under uncommitted facilities<br />

disclosed below.<br />

** Syndicated loan with a consortium of banks with BNP Paribas as agent with a total revolving facility available of EUR600<br />

million, which are subject to net finance cost cover and debt to total capitalisation ratio financial covenants which relate to the<br />

<strong>Sappi</strong> Limited Group.<br />

F-68