In Fonderia 2 2024

Secondo numero del 2024 di In Fonderia

Secondo numero del 2024 di In Fonderia

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

STEEL AND ALUMINIUM: ONE GOES UP, THE<br />

OTHER GOES DOWN<br />

Twenty-five years ago, the packaging chain, as<br />

contained in the report, was one of the first to<br />

be regulated at a European level with an apsuperiori<br />

al 70% del totale.<br />

Gli obiettivi sfidanti di decarbonizzazione fissati dall’Ue, del resto, stanno facendo emergere con sempre<br />

maggiore evidenza il ruolo chiave del riciclo del rottame ferroso quale risorsa strategica per la transizione e la<br />

conseguente necessità di misure che consentano di aumentarne la disponibilità e la qualità per l’industria<br />

siderurgica e fusoria europea. La capacità di produzione di acciaio da forno elettrico tenderà necessariamente<br />

ad aumentare, portandosi dietro una crescente domanda globale di rottame e in particolare IN PRIMO di rottame PIANOcon<br />

elevate caratteristiche qualitative per supportare produzioni siderurgiche e fusioni a più alto valore aggiunto.<br />

A causa della forte dipendenza dell’industria manufatturiera italiana dall’importazione dei metalli, il<br />

miglioramento della raccolta di questa frazione diverrà quindi sempre più strategico per la nostra economia.<br />

glio, forse il più difficile da superare, riguarda<br />

l’approccio normativo europeo. Bruxelles ha<br />

sempre dato più valore alle pratiche di riuso,<br />

invece che al riciclo, riducendo così in maniera<br />

significativa l’accessibilità alle materie prime<br />

secondarie. L’accordo raggiunto di recente per<br />

il nuovo Packaging & Packaging Waste Regulation<br />

(Ppwr) sembra essere un compromesso<br />

valido. Tuttavia, il problema resta. Riuso versus<br />

riciclo non è sinonimo di sana concorrenza,<br />

bensì uno scontro interno all’Ue, che non fa<br />

bene a nessuno.<br />

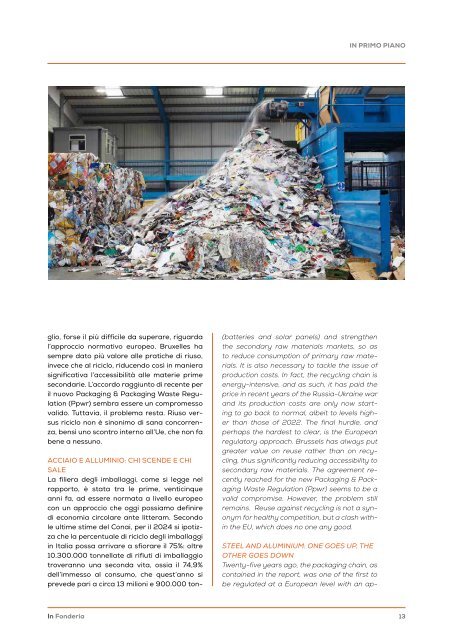

ACCIAIO E ALLUMINIO: CHI SCENDE E CHI<br />

SALE<br />

La filiera degli imballaggi, come si legge nel<br />

rapporto, è stata tra le prime, venticinque<br />

anni fa, ad essere normata a livello europeo<br />

con un approccio che oggi possiamo definire<br />

di economia circolare ante litteram. Secondo<br />

le ultime stime del Conai, per il <strong>2024</strong> si ipotizza<br />

che la percentuale di riciclo degli imballaggi<br />

in Italia possa arrivare a sfiorare il 75%: oltre<br />

10.300.000 tonnellate di rifiuti di imballaggio<br />

troveranno una seconda vita, ossia il 74,9%<br />

dell’immesso al consumo, che quest’anno si<br />

prevede pari a circa 13 milioni e 900.000 ton-<br />

(batteries and solar panels) and strengthen<br />

the secondary raw materials markets, so as<br />

to reduce consumption of primary raw materials.<br />

It is also necessary to tackle the issue of<br />

production costs. <strong>In</strong> fact, the recycling chain is<br />

energy-intensive, and as such, it has paid the<br />

price in recent years of the Russia-Ukraine war<br />

and its production costs are only now starting<br />

to go back to normal, albeit to levels higher<br />

than those of 2022. The final hurdle, and<br />

perhaps the hardest to clear, is the European<br />

regulatory approach. Brussels has always put<br />

greater value on reuse rather than on recycling,<br />

thus significantly reducing accessibility to<br />

secondary raw materials. The agreement recently<br />

reached for the new Packaging & Packaging<br />

Waste Regulation (Ppwr) seems to be a<br />

valid compromise. However, the problem still<br />

remains. Reuse against recycling is not a synonym<br />

for healthy competition, but a clash within<br />

the EU, which does no one any good.<br />

<strong>In</strong> <strong>Fonderia</strong><br />

13