UN World Investment Report 2010 - Office of Trade Negotiations

UN World Investment Report 2010 - Office of Trade Negotiations

UN World Investment Report 2010 - Office of Trade Negotiations

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

108<br />

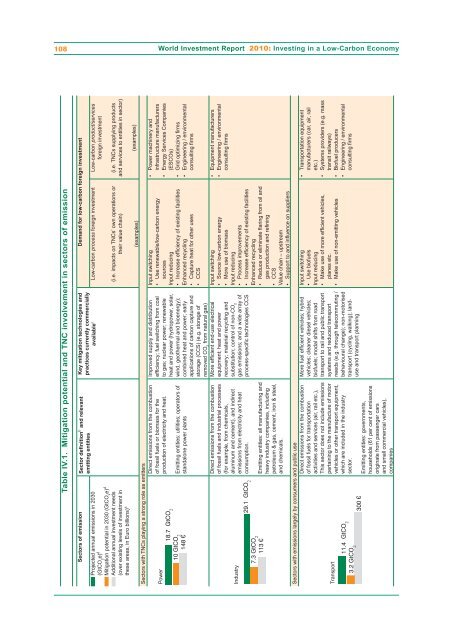

Table IV.1. Mitigation potential and TNC involvement in sectors <strong>of</strong> emission<br />

Demand for low-carbon foreign investment<br />

Low-carbon product/services<br />

foreign investment<br />

Low-carbon process foreign investment<br />

Key mitigation technologies and<br />

practices currently commercially<br />

available c<br />

(i.e. TNCs supplying products<br />

and services to entities in sector)<br />

(i.e. impacts on TNCs’ own operations or<br />

their value chain)<br />

Sectors <strong>of</strong> emission Sector definition b and relevant<br />

emitting entities<br />

Projected annual emissions in 2030<br />

(GtCO e) 2 d<br />

Mitigation potential in 2030 (GtCO e) 2 d<br />

Additional annual investment needs<br />

(over existing levels <strong>of</strong> investment in<br />

these areas, in Euro billions) a<br />

(examples)<br />

(examples)<br />

<strong>World</strong> <strong>Investment</strong> <strong>Report</strong> <strong>2010</strong>: Investing in a Low-Carbon Economy<br />

Power machinery and<br />

infrastructure manufacturers<br />

Energy Services Companies<br />

(ESCOs)<br />

Grid optimizing firms<br />

Engineering / environmental<br />

consulting firms<br />

•<br />

•<br />

•<br />

•<br />

Input switching<br />

• Use renewable/low-carbon energy<br />

sources<br />

Input reducing<br />

• Increase efficiency <strong>of</strong> existing facilities<br />

Enhanced recycling<br />

• Capture heat for other uses<br />

• CCS<br />

Improved supply and distribution<br />

efficiency; fuel switching from coal<br />

to gas; nuclear power; renewable<br />

heat and power (hydropower, solar,<br />

wind, geothermal and bioenergy);<br />

combined heat and power; early<br />

applications <strong>of</strong> carbon capture and<br />

storage (CCS) (e.g. storage <strong>of</strong><br />

removed CO from natural gas)<br />

2<br />

More efficient end-use electrical<br />

equipment; heat and power<br />

recovery; material recycling and<br />

substitution; control <strong>of</strong> non-CO2 gas emissions; and a wide array <strong>of</strong><br />

process-specific technologies CCS<br />

Sectors with TNCs playing a strong role as emitters<br />

Direct emissions from the combustion<br />

<strong>of</strong> fossil fuels or biomass for the<br />

Power<br />

production <strong>of</strong> electricity and heat.<br />

18.7 GtCO<br />

2<br />

10 GtCO<br />

2<br />

Emitting entities: utilities; operators <strong>of</strong><br />

148 €<br />

standalone power plants<br />

Equipment manufacturers<br />

Engineering / environmental<br />

consulting firms<br />

•<br />

•<br />

Input switching<br />

• Source low-carbon energy<br />

• More use <strong>of</strong> biomass<br />

Input reducing<br />

• Process improvements<br />

• Increase efficiency <strong>of</strong> existing facilities<br />

Enhanced recycling<br />

• Reduce or eliminate flaring from oil and<br />

gas production and refining<br />

• CCS<br />

Value chain – upstream<br />

• Support to and influence on suppliers<br />

Direct emissions from the combustion<br />

<strong>of</strong> fossil fuels and industrial processes<br />

(for example, from chemicals,<br />

aluminum and cement), and indirect<br />

emissions from electricity and heat<br />

consumption.<br />

Industry<br />

29.1 GtCO 2<br />

Emitting entities: all manufacturing and<br />

heavy industry companies, including<br />

petroleum & gas, cement, iron & steel,<br />

and chemicals.<br />

7.3 GtCO<br />

2<br />

113 €<br />

Transportation equipment<br />

manufacturers (car, air, rail<br />

etc.)<br />

Systems providers (e.g. mass<br />

transit railways)<br />

Bi<strong>of</strong>uel producers<br />

Engineering / environmental<br />

consulting firms<br />

•<br />

•<br />

•<br />

•<br />

Input switching<br />

• Use bi<strong>of</strong>uels<br />

Input reducing<br />

• Make use <strong>of</strong> more efficient vehicles,<br />

planes etc.<br />

• Make use <strong>of</strong> non-emitting vehicles<br />

More fuel efficient vehicles; hybrid<br />

vehicles; cleaner diesel vehicles;<br />

bi<strong>of</strong>uels; modal shifts from road<br />

transport to rail and public transport<br />

systems and reduced transport<br />

needs (e.g. through telecommuting /<br />

behavioural change); non-motorised<br />

transport (cycling, walking); landuse<br />

and transport planning<br />

Sectors with emissions largely by consumers and public use<br />

Direct emissions from the combustion<br />

<strong>of</strong> fossil fuels for transportation<br />

activities and services (air, rail etc.),<br />

This sector does not include emissions<br />

pertaining to the manufacture <strong>of</strong> motor<br />

Transport<br />

vehicles or other transport equipment,<br />

11.4 GtCO which are included in the industry<br />

2<br />

3.2 GtCO sector.<br />

2<br />

300 €<br />

Emitting entities: governments,<br />

households (61 per cent <strong>of</strong> emissions<br />

originate from passenger cars<br />

and small commercial vehicles),<br />

companies