Annual Report 1997/1998 - Munich Re

Annual Report 1997/1998 - Munich Re

Annual Report 1997/1998 - Munich Re

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Munich</strong> <strong>Re</strong> <strong><strong>Re</strong>port</strong> of the Board of Management<br />

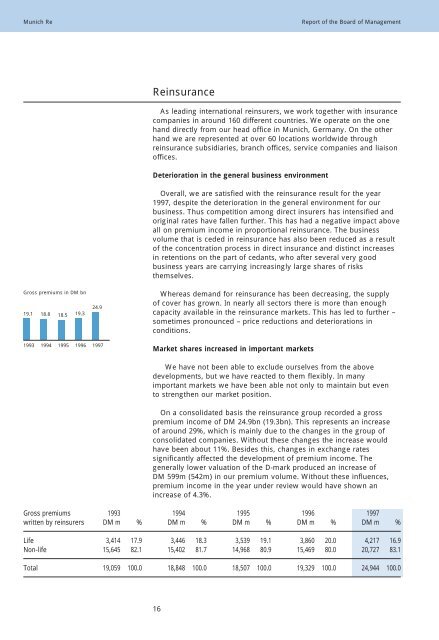

Gross premiums in DM bn<br />

19.1 18.8 18.5 19.3<br />

24.9<br />

1993 1994 1995 1996 <strong>1997</strong><br />

<strong>Re</strong>insurance<br />

As leading international reinsurers, we work together with insurance<br />

companies in around 160 different countries. We operate on the one<br />

hand directly from our head office in <strong>Munich</strong>, Germany. On the other<br />

hand we are represented at over 60 locations worldwide through<br />

reinsurance subsidiaries, branch offices, service companies and liaison<br />

offices.<br />

Deterioration in the general business environment<br />

Overall, we are satisfied with the reinsurance result for the year<br />

<strong>1997</strong>, despite the deterioration in the general environment for our<br />

business. Thus competition among direct insurers has intensified and<br />

original rates have fallen further. This has had a negative impact above<br />

all on premium income in proportional reinsurance. The business<br />

volume that is ceded in reinsurance has also been reduced as a result<br />

of the concentration process in direct insurance and distinct increases<br />

in retentions on the part of cedants, who after several very good<br />

business years are carrying increasingly large shares of risks<br />

themselves.<br />

Whereas demand for reinsurance has been decreasing, the supply<br />

of cover has grown. In nearly all sectors there is more than enough<br />

capacity available in the reinsurance markets. This has led to further –<br />

sometimes pronounced – price reductions and deteriorations in<br />

conditions.<br />

Market shares increased in important markets<br />

We have not been able to exclude ourselves from the above<br />

developments, but we have reacted to them flexibly. In many<br />

important markets we have been able not only to maintain but even<br />

to strengthen our market position.<br />

On a consolidated basis the reinsurance group recorded a gross<br />

premium income of DM 24.9bn (19.3bn). This represents an increase<br />

of around 29%, which is mainly due to the changes in the group of<br />

consolidated companies. Without these changes the increase would<br />

have been about 11%. Besides this, changes in exchange rates<br />

significantly affected the development of premium income. The<br />

generally lower valuation of the D-mark produced an increase of<br />

DM 599m (542m) in our premium volume. Without these influences,<br />

premium income in the year under review would have shown an<br />

increase of 4.3%.<br />

Gross premiums 1993 1994 1995 1996 <strong>1997</strong><br />

written by reinsurers DM m % DM m % DM m % DM m % DM m %<br />

Life 3,414 17.9 3,446 18.3 3,539 19.1 3,860 20.0 4,217 16.9<br />

Non-life 15,645 82.1 15,402 81.7 14,968 80.9 15,469 80.0 20,727 83.1<br />

Total 19,059 100.0 18,848 100.0 18,507 100.0 19,329 100.0 24,944 100.0<br />

16