Sterlite Industries (India) Limited - Sterlite Industries India Ltd.

Sterlite Industries (India) Limited - Sterlite Industries India Ltd.

Sterlite Industries (India) Limited - Sterlite Industries India Ltd.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

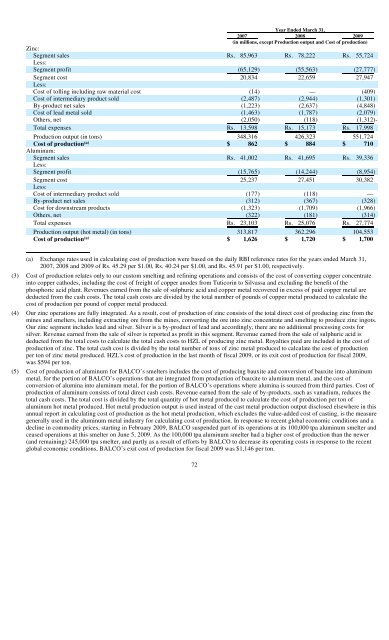

Year Ended March 31,<br />

2007 2008 2009<br />

(in millions, except Production output and Cost of production)<br />

Zinc:<br />

Segment sales Rs. 85,963 Rs. 78,222 Rs. 55,724<br />

Less:<br />

Segment profit (65,129) (55,563) (27,777)<br />

Segment cost 20,834 22,659 27,947<br />

Less:<br />

Cost of tolling including raw material cost (14) — (409)<br />

Cost of intermediary product sold (2,487) (2,944) (1,301)<br />

By-product net sales (1,223) (2,637) (4,848)<br />

Cost of lead metal sold (1,463) (1,787) (2,079)<br />

Others, net (2,050) (118) (1,312)-<br />

Total expenses Rs. 13,598 Rs. 15,173 Rs. 17,998<br />

Production output (in tons) 348,316 426,323 551,724<br />

Cost of production (a) $ 862 $ 884 $ 710<br />

Aluminum:<br />

Segment sales Rs. 41,002 Rs. 41,695 Rs. 39,336<br />

Less:<br />

Segment profit (15,765) (14,244) (8,954)<br />

Segment cost 25,237 27,451 30,382<br />

Less:<br />

Cost of intermediary product sold (177) (118) —<br />

By-product net sales (312) (367) (328)<br />

Cost for downstream products (1,323) (1,709) (1,966)<br />

Others, net (322) (181) (314)<br />

Total expenses Rs. 23,103 Rs. 25,076 Rs. 27,774<br />

Production output (hot metal) (in tons) 313,817 362,296 104,553<br />

Cost of production (a) $ 1,626 $ 1,720 $ 1,700<br />

(a) Exchange rates used in calculating cost of production were based on the daily RBI reference rates for the years ended March 31,<br />

2007, 2008 and 2009 of Rs. 45.29 per $1.00, Rs. 40.24 per $1.00, and Rs. 45.91 per $1.00, respectively.<br />

(3) Cost of production relates only to our custom smelting and refining operations and consists of the cost of converting copper concentrate<br />

into copper cathodes, including the cost of freight of copper anodes from Tuticorin to Silvassa and excluding the benefit of the<br />

phosphoric acid plant. Revenues earned from the sale of sulphuric acid and copper metal recovered in excess of paid copper metal are<br />

deducted from the cash costs. The total cash costs are divided by the total number of pounds of copper metal produced to calculate the<br />

cost of production per pound of copper metal produced.<br />

(4) Our zinc operations are fully integrated. As a result, cost of production of zinc consists of the total direct cost of producing zinc from the<br />

mines and smelters, including extracting ore from the mines, converting the ore into zinc concentrate and smelting to produce zinc ingots.<br />

Our zinc segment includes lead and silver. Silver is a by-product of lead and accordingly, there are no additional processing costs for<br />

silver. Revenue earned from the sale of silver is reported as profit in this segment. Revenue earned from the sale of sulphuric acid is<br />

deducted from the total costs to calculate the total cash costs to HZL of producing zinc metal. Royalties paid are included in the cost of<br />

production of zinc. The total cash cost is divided by the total number of tons of zinc metal produced to calculate the cost of production<br />

per ton of zinc metal produced. HZL's cost of production in the last month of fiscal 2009, or its exit cost of production for fiscal 2009,<br />

was $594 per ton.<br />

(5) Cost of production of aluminum for BALCO’s smelters includes the cost of producing bauxite and conversion of bauxite into aluminum<br />

metal, for the portion of BALCO’s operations that are integrated from production of bauxite to aluminum metal, and the cost of<br />

conversion of alumina into aluminum metal, for the portion of BALCO’s operations where alumina is sourced from third parties. Cost of<br />

production of aluminum consists of total direct cash costs. Revenue earned from the sale of by-products, such as vanadium, reduces the<br />

total cash costs. The total cost is divided by the total quantity of hot metal produced to calculate the cost of production per ton of<br />

aluminum hot metal produced. Hot metal production output is used instead of the cast metal production output disclosed elsewhere in this<br />

annual report in calculating cost of production as the hot metal production, which excludes the value-added cost of casting, is the measure<br />

generally used in the aluminum metal industry for calculating cost of production. In response to recent global economic conditions and a<br />

decline in commodity prices, starting in February 2009, BALCO suspended part of its operations at its 100,000 tpa aluminum smelter and<br />

ceased operations at this smelter on June 5, 2009. As the 100,000 tpa aluminum smelter had a higher cost of production than the newer<br />

(and remaining) 245,000 tpa smelter, and partly as a result of efforts by BALCO to decrease its operating costs in response to the recent<br />

global economic conditions, BALCO’s exit cost of production for fiscal 2009 was $1,146 per ton.<br />

72