Download PDF (2.5MB) - Anchor Environmental

Download PDF (2.5MB) - Anchor Environmental

Download PDF (2.5MB) - Anchor Environmental

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

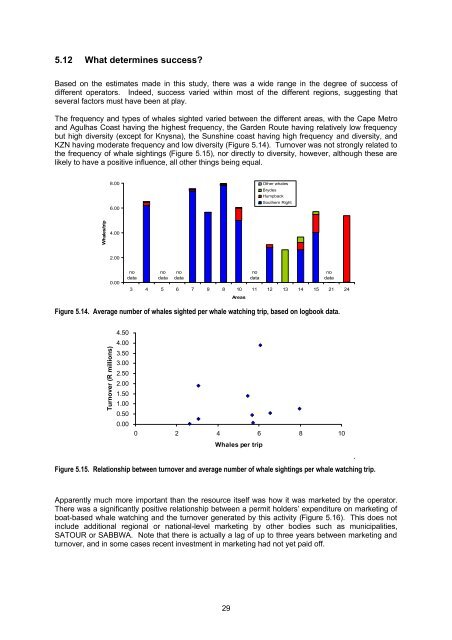

5.12 What determines success<br />

Based on the estimates made in this study, there was a wide range in the degree of success of<br />

different operators. Indeed, success varied within most of the different regions, suggesting that<br />

several factors must have been at play.<br />

The frequency and types of whales sighted varied between the different areas, with the Cape Metro<br />

and Agulhas Coast having the highest frequency, the Garden Route having relatively low frequency<br />

but high diversity (except for Knysna), the Sunshine coast having high frequency and diversity, and<br />

KZN having moderate frequency and low diversity (Figure 5.14). Turnover was not strongly related to<br />

the frequency of whale sightings (Figure 5.15), nor directly to diversity, however, although these are<br />

likely to have a positive influence, all other things being equal.<br />

8.00<br />

6.00<br />

Other whales<br />

Brydes<br />

Humpback<br />

Southern Right<br />

Whales/trip<br />

4.00<br />

2.00<br />

0.00<br />

no<br />

data<br />

no<br />

data<br />

no<br />

data<br />

3 4 5 6 7 9 8 10 11 12 13 14 15 21 24<br />

Areas<br />

no<br />

data<br />

no<br />

data<br />

Figure 5.14. Average number of whales sighted per whale watching trip, based on logbook data.<br />

Turnover (R millions)<br />

4.50<br />

4.00<br />

3.50<br />

3.00<br />

2.50<br />

2.00<br />

1.50<br />

1.00<br />

0.50<br />

0.00<br />

0 2 4 6 8 10<br />

Whales per trip<br />

.<br />

Figure 5.15. Relationship between turnover and average number of whale sightings per whale watching trip.<br />

Apparently much more important than the resource itself was how it was marketed by the operator.<br />

There was a significantly positive relationship between a permit holders’ expenditure on marketing of<br />

boat-based whale watching and the turnover generated by this activity (Figure 5.16). This does not<br />

include additional regional or national-level marketing by other bodies such as municipalities,<br />

SATOUR or SABBWA. Note that there is actually a lag of up to three years between marketing and<br />

turnover, and in some cases recent investment in marketing had not yet paid off.<br />

29