non-resident individual income tax - Lembaga Hasil Dalam Negeri

non-resident individual income tax - Lembaga Hasil Dalam Negeri

non-resident individual income tax - Lembaga Hasil Dalam Negeri

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

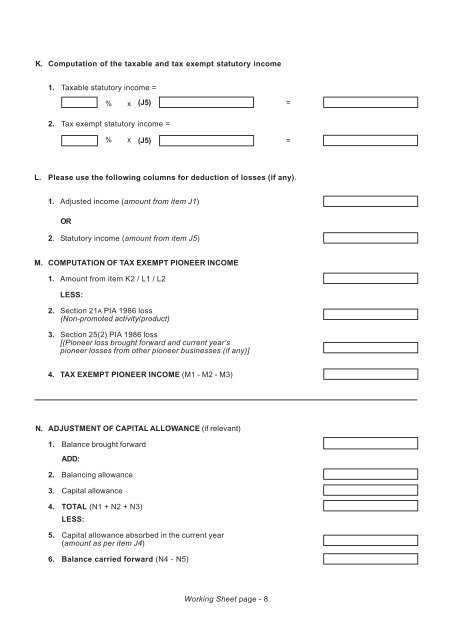

K. Computation of the <strong>tax</strong>able and <strong>tax</strong> exempt statutory <strong>income</strong><br />

1. Taxable statutory <strong>income</strong> =<br />

% x<br />

(J5)<br />

=<br />

2. Tax exempt statutory <strong>income</strong> =<br />

% x<br />

(J5)<br />

=<br />

L. Please use the following columns for deduction of losses (if any).<br />

1. Adjusted <strong>income</strong> (amount from item J1)<br />

OR<br />

2. Statutory <strong>income</strong> (amount from item J5)<br />

M. COMPUTATION OF TAX EXEMPT PIONEER INCOME<br />

1. Amount from item K2 / L1 / L2<br />

LESS:<br />

2. Section 21A PIA 1986 loss<br />

(Non-promoted activity/product)<br />

3. Section 25(2) PIA 1986 loss<br />

[(Pioneer loss brought forward and current year’s<br />

pioneer losses from other pioneer businesses (if any)]<br />

4. TAX EXEMPT PIONEER INCOME (M1 - M2 - M3)<br />

N. ADJUSTMENT OF CAPITAL ALLOWANCE (if relevant)<br />

1. Balance brought forward<br />

ADD:<br />

2. Balancing allowance<br />

3. Capital allowance<br />

4. TOTAL (N1 + N2 + N3)<br />

LESS:<br />

5. Capital allowance absorbed in the current year<br />

(amount as per item J4)<br />

6. Balance carried forward (N4 - N5)<br />

Working Sheet page - 8