NIPS Annual Report and Accounts 2012-13 - Department of Justice

NIPS Annual Report and Accounts 2012-13 - Department of Justice

NIPS Annual Report and Accounts 2012-13 - Department of Justice

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>2012</strong>-20<strong>13</strong><br />

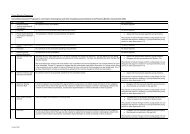

Component Definition<br />

Building Substructure, Frame, Upper Floors,<br />

Structure Ro<strong>of</strong>, Stairs, External Walls,<br />

Windows & external doors, Internal<br />

walls & partitions, Internal doors,<br />

Floors/wall/ceiling finishes<br />

Engineering Sanitary appliances, services<br />

Systems equipment, disposal installation,<br />

water installation, heat source,<br />

space heating, & air treatment,<br />

ventilation systems, electrical, gas,<br />

lift <strong>and</strong> protective installations.<br />

Equipment & CCTV, access control, alarm<br />

Security systems, control rooms including all<br />

Installations associated ICT hardware &<br />

s<strong>of</strong>tware; Fixed furniture, fittings,<br />

equipment & appliances.<br />

External Roads, footpaths, drainage, fences,<br />

Works gates, boundary walls, street<br />

furniture, l<strong>and</strong>scaping <strong>and</strong><br />

external lighting.<br />

Property, Plant <strong>and</strong> Equipment, other than L<strong>and</strong> <strong>and</strong><br />

Buildings are carried at current cost using indices<br />

compiled by the Office for National Statistics. The<br />

st<strong>and</strong>ard threshold for capitalisation is £1,000.<br />

Lower thresholds apply to certain types <strong>of</strong> IT<br />

equipment.<br />

Expenditure on <strong>of</strong>fice furniture <strong>and</strong> equipment is<br />

classified as capital expenditure if the purchase cost<br />

<strong>of</strong> an individual item is over the st<strong>and</strong>ard threshold<br />

<strong>of</strong> £1,000. An exception to this is if, as the result<br />

<strong>of</strong> a refurbishment or the establishment <strong>of</strong> a new<br />

<strong>of</strong>fice or project, a pool <strong>of</strong> new <strong>of</strong>fice furniture<br />

or equipment is purchased with individual items<br />

costing less than £1,000 but the total purchase<br />

costs are more than £1,000.<br />

Properties regarded by the Northern Irel<strong>and</strong> Prison<br />

Service as operational are valued on the basis <strong>of</strong><br />

existing use, or where this could not be assessed<br />

because there is no market value for the property, its<br />

depreciated replacement cost. Properties regarded<br />

by the Northern Irel<strong>and</strong> Prison Service as nonoperational<br />

are valued on the basis <strong>of</strong> open market<br />

value.<br />

1.4 Intangible Assets<br />

Purchased computer s<strong>of</strong>tware licences are<br />

capitalised as intangible assets where expenditure<br />

<strong>of</strong> £1,000 or more is incurred. Intangible assets are<br />

stated at their market value. Intangible assets are<br />

amortised on a straight-line basis over the expected<br />

useful lives <strong>of</strong> the assets concerned.<br />

1.5 Financial Instruments<br />

Under IAS 39 <strong>and</strong> IFRS 7, the Northern Irel<strong>and</strong><br />

Prison Service is required to recognise, measure <strong>and</strong><br />

disclose the elements <strong>of</strong> its 0% interest Housing<br />

Loan Scheme at fair value. These elements have<br />

been identified within both Non-current <strong>and</strong><br />

Current Financial Assets. The carrying value has been<br />

discounted at a rate <strong>of</strong> 3.5% in line with Treasury<br />

guidelines. The Northern Irel<strong>and</strong> Prison Service does<br />

not hold any other financial instruments.<br />

1.6 Depreciation <strong>and</strong> Amortisation<br />

Freehold l<strong>and</strong> is not depreciated. <strong>NIPS</strong> has<br />

depreciated separately identified components <strong>of</strong><br />

its buildings assets according to the useful life<br />

<strong>of</strong> that component, with individual lives applied<br />

to each component. Provision for depreciation<br />

<strong>and</strong> amortisation is made to write-<strong>of</strong>f the cost<br />

<strong>of</strong> property, plant <strong>and</strong> equipment <strong>and</strong> intangible<br />

assets on a straight-line basis over the expected<br />

useful lives <strong>of</strong> the assets concerned. L<strong>and</strong>, assets<br />

under construction or assets awaiting disposal are<br />

not depreciated. The overall expected useful lives <strong>of</strong><br />

assets are as follows:<br />

75