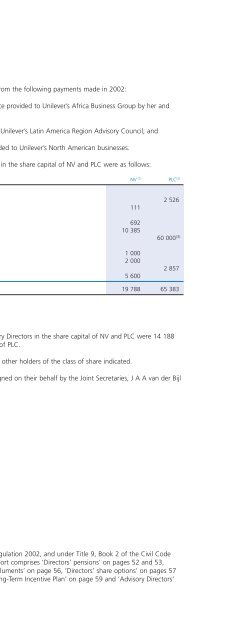

Report & accounts 2002 in full - Unilever

Report & accounts 2002 in full - Unilever

Report & accounts 2002 in full - Unilever

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

122 Additional <strong>in</strong>formation for US <strong>in</strong>vestors<br />

<strong>Unilever</strong> Group<br />

Classification differences between UK and US GAAP<br />

Revenue recognition<br />

Under US GAAP, certa<strong>in</strong> sales <strong>in</strong>centive expenses which have been <strong>in</strong>cluded <strong>in</strong> operat<strong>in</strong>g costs under <strong>Unilever</strong>’s account<strong>in</strong>g would be<br />

deducted from turnover. The decrease <strong>in</strong> turnover for the years to 31 December <strong>2002</strong>, 2001 and 2000 is €1 337 million, €1 279 million<br />

and €1 237 million respectively. There is no impact on <strong>Unilever</strong>’s net profit.<br />

Cash flow statement<br />

Under US GAAP, various items would be reclassified with<strong>in</strong> the consolidated cash flow statement. In particular, <strong>in</strong>terest received, <strong>in</strong>terest<br />

paid and taxation would be part of net cash flow from operat<strong>in</strong>g activities, and dividends paid would be <strong>in</strong>cluded with<strong>in</strong> net cash flow from<br />

f<strong>in</strong>anc<strong>in</strong>g. In addition, under US GAAP, cash and cash equivalents comprise cash balances and current <strong>in</strong>vestments with an orig<strong>in</strong>al maturity<br />

at the date of <strong>in</strong>vestment of less than three months. Under <strong>Unilever</strong>’s presentation, cash <strong>in</strong>cludes only cash <strong>in</strong> hand or available on demand<br />

less bank overdrafts. Movements <strong>in</strong> those current <strong>in</strong>vestments which are <strong>in</strong>cluded under the head<strong>in</strong>g of cash and cash equivalents under<br />

US GAAP form part of the movement entitled ‘Management of liquid resources’ <strong>in</strong> the cash flow statements. At 31 December <strong>2002</strong>, the<br />

balance of such <strong>in</strong>vestments was €45 million (2001: €9 million; 2000: €58 million).<br />

Recently issued account<strong>in</strong>g pronouncements<br />

In August 2001, FASB issued SFAS 143, ‘Account<strong>in</strong>g for Asset Retirement Obligations’. This statement is effective from January 2003 and<br />

requires obligations associated with the retirement of a tangible long-lived asset to be recorded as a liability upon acquisition of the asset.<br />

SFAS 143 would not have a material impact on <strong>Unilever</strong>’s f<strong>in</strong>ancial position or results of operations.<br />

In July <strong>2002</strong>, the FASB issued SFAS 146, ‘Account<strong>in</strong>g for Costs Associated with Exit or Disposal Activities’. This standard will require <strong>Unilever</strong><br />

to recognise certa<strong>in</strong> costs associated with disposal activities when they are <strong>in</strong>curred, rather than at the date of a commitment to a disposal<br />

plan. SFAS 146 is effective for disposal activities <strong>in</strong>itiated after 31 December <strong>2002</strong>. Given the nature of disposal plans, it is not possible to<br />

determ<strong>in</strong>e <strong>in</strong> advance the impact it might have on <strong>Unilever</strong>’s f<strong>in</strong>ancial position at a particular date or <strong>Unilever</strong>’s results of operations for a<br />

particular period <strong>in</strong> the future. For <strong>2002</strong>, the impact is shown aga<strong>in</strong>st restructur<strong>in</strong>g costs <strong>in</strong> the US GAAP reconciliation statements on pages<br />

118 and 119.<br />

In December <strong>2002</strong>, the FASB issued SFAS 148, ’Account<strong>in</strong>g for Stock-Based Compensation - Transition and Disclosure - an Amendment<br />

of SFAS No. 123’. This standard provides two additional transition methods for companies elect<strong>in</strong>g to adopt the fair value account<strong>in</strong>g<br />

provisions of SFAS 123, ’Account<strong>in</strong>g for Stock-Based Compensation’, but does not change the fair value measurement pr<strong>in</strong>ciples of<br />

SFAS 123. When <strong>Unilever</strong> adopts the fair value method for account<strong>in</strong>g for stock options, we expect to use <strong>full</strong> retrospective restatement.<br />

The impact of this is shown <strong>in</strong> the table on page 104.<br />

In November <strong>2002</strong>, the FASB issued F<strong>in</strong>ancial Interpretation No. 45 (FIN 45), ’Guarantor’s and Disclosure Requirements for Guarantees,<br />

Includ<strong>in</strong>g Direct Guarantees’. Under this <strong>in</strong>terpretation, a guarantor must recognise the fair value of the obligation undertaken <strong>in</strong> issu<strong>in</strong>g<br />

a guarantee. The <strong>in</strong>itial recognition and <strong>in</strong>itial measurement provisions of this <strong>in</strong>terpretation are applicable on a prospective basis to<br />

guarantees issued or modified after 31 December <strong>2002</strong>. FIN 45 is not expected to have a material impact on <strong>Unilever</strong>’s f<strong>in</strong>ancial position<br />

or results of operations.<br />

In January 2003, the FASB issued F<strong>in</strong>ancial Interpretation No. 46 (FIN 46), ’Consolidation of Variable Interest Entities’. Under this<br />

<strong>in</strong>terpretation, certa<strong>in</strong> entities known as variable <strong>in</strong>terest entities must be consolidated by the primary beneficiary of the entity.<br />

The measurement pr<strong>in</strong>ciples of this <strong>in</strong>terpretation will be effective for <strong>Unilever</strong>’s 2003 f<strong>in</strong>ancial statements. FIN 46 is not expected<br />

to have any impact on <strong>Unilever</strong>’s f<strong>in</strong>ancial position or results of operations.<br />

Documents on display <strong>in</strong> the United States<br />

<strong>Unilever</strong> files and furnishes reports and <strong>in</strong>formation with the United States Securities and Exchange Commission (SEC), and such reports<br />

and <strong>in</strong>formation can be <strong>in</strong>spected and copied at the SEC’s public reference facilities <strong>in</strong> Wash<strong>in</strong>gton DC, Chicago and New York. Certa<strong>in</strong><br />

of our reports and other <strong>in</strong>formation that we file or furnish to the SEC are also available to the public over the <strong>in</strong>ternet on the SEC’s<br />

website at www.sec.gov.<br />

<strong>Unilever</strong> Annual <strong>Report</strong> & Accounts and Form 20-F <strong>2002</strong>