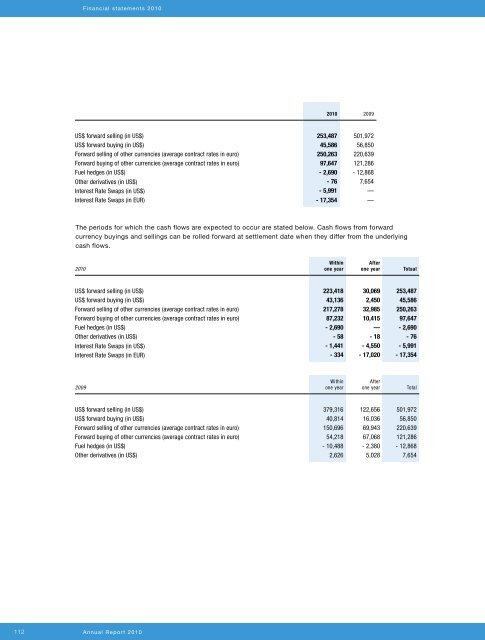

Financial statements 20102010 2009US$ forward selling (in US$) 253,487 501,972US$ forward buying (in US$) 45,586 56,850Forward selling of other currencies (average contract rates in euro) 250,263 220,639Forward buying of other currencies (average contract rates in euro) 97,647 121,286Fuel hedges (in US$) - 2,690 - 12,868Other derivatives (in US$) - 76 7,654Interest Rate Swaps (in US$) - 5,991 —Interest Rate Swaps (in EUR) - 17,354 —The periods for which the cash flows are expected to occur are stated below. Cash flows from forwardcurrency buyings and sellings can be rolled forward at settlement date when they differ from the underlyingcash flows.2010Withinone yearAfterone yearTotaalUS$ forward selling (in US$) 223,418 30,069 253,487US$ forward buying (in US$) 43,136 2,450 45,586Forward selling of other currencies (average contract rates in euro) 217,278 32,985 250,263Forward buying of other currencies (average contract rates in euro) 87,232 10,415 97,647Fuel hedges (in US$) - 2,690 — - 2,690Other derivatives (in US$) - 58 - 18 - 76Interest Rate Swaps (in US$) - 1,441 - 4,550 - 5,991Interest Rate Swaps (in EUR) - 334 - 17,020 - 17,3542009Withinone yearAfterone yearTotalUS$ forward selling (in US$) 379,316 122,656 501,972US$ forward buying (in US$) 40,814 16,036 56,850Forward selling of other currencies (average contract rates in euro) 150,696 69,943 220,639Forward buying of other currencies (average contract rates in euro) 54,218 67,068 121,286Fuel hedges (in US$) - 10,488 - 2,380 - 12,868Other derivatives (in US$) 2,626 5,028 7,654112 <strong>Annual</strong> Report 2010

Financial statements 2010The results on effective cash flow hedges are recognized in group equity as stated below:2010 2009Opening balance Hedging reserve as at January 1 8,262 5,735Movement in fair value of effective cash flow hedges recognized in group equity - 4,380 5,398Transferred to the income statement - 7,174 - 3,925Total directly recognized in group equity - 11,554 1,473Taxation 938 1,054Directly charged to the Hedging reserve (net of taxes) - 10,616 2,527Balance Hedging reserve as at December 31 - 2,354 8,262The results on non-effective cash flow hedges are presented within the operational costs and amount to € 6.2million negative over 2010 (2009: € 14.5 million positive).26.3 Capital managementThe Board of Management’s policy is to maintain a strong capital base so as to maintain customer, investor,creditor and market confidence and to support future development of the business. The Board of Managementmonitors the return on equity, which the Group defines as net operating income divided by total shareholders’equity, excluding minority interests. The Board of Management also monitors the level of dividend to be paid toholders of ordinary shares. The dividend policy is to maintain a pay-out ratio of 40% to 50%.The Board of Management seeks to maintain a balance between the higher returns that might be possible withhigher levels of borrowings and the benefits of a sound capital position. The Group’s target is to achieve along-term return on equity of at least 12%; in 2010 the return was 21.7% (2009: 21.1%).Royal <strong>Boskalis</strong> Westminster N.V. does not have a defined share buy-back plan.There were no changes in the Group’s approach to capital management during the year.Neither Royal <strong>Boskalis</strong> Westminster N.V. nor any of its Group companies are subject to externally imposedcapital requirements.26.4 Other financial instrumentsPursuant to the decision of the General Meeting of Shareholders held on May 9, 2001, the StichtingContinuïteit KBW has acquired the right to take cumulative protective preference shares in Royal <strong>Boskalis</strong>Westminster N.V. for a nominal amount which shall be equal to the nominal amount of ordinary sharesoutstanding at the time of the issue. This right qualifies as a derivative financial liability, with the followingimportant conditions. The cumulative protective preference shares are to be issued at par against a 25% cashcontribution, the remainder after call-up by the Stichting in consultation with Royal <strong>Boskalis</strong> Westminster N.V.After the issue, Royal <strong>Boskalis</strong> Westminster N.V. has the obligation to buy or cancel the shares upon theStichting’s request. The preferential dividend right amounts to Euribor increased by 4% at most. The interestand credit risk is limited. The fair value of the option right is nil.Royal <strong>Boskalis</strong> Westminster nv113