Review of OperationsSales up by 13 per centSector Outlook10123The continued sluggish demand in local markets and stiff competition from substitute materials, have impacted the VFY business adversely.Against this backdrop, through aggressive marketing efforts and improved share of exports, the Division has put in a satisfactory performance.Notwithstanding the fall in demand in the domestic market, sales volumes at 15,326 tonnes have grown by 13 per cent YoY, primarilyon the back of improved exports. Exports soared from 1,105 tonnes to 2,037 tonnes, reflecting a growth of 84 per cent YoY. A successfulentry into new markets and deeper penetration into existing markets have been the key drivers. The razor-sharp focus on product quality,backed by superior customer service has enabled it to reposition its products amongst quality conscious customers. This, together with thecompetitive pricing strategy led to achieving superior valume growths. Domestic volumes grew by 7 per cent YoY from 12,402 tonnes in FY2000 to 13,289 tonnes in FY 2001. Besides aggressive marketing and promotional efforts, improved quality of yarns and a strengtheneddistribution network have contributed to this encouraging result. The Division’s market share has also gone up from 27 per cent to 28 percent during the year.Asset utilization at record high levels, margins maintainedReflecting improved domestic volumes and recovery in exports, production volumes have risen significantly. The VFY Sector’s volumesat 15,496 tonnes are 23 per cent higher over that of the earlier year. These reflect a cpacity utilisation of 103 per cent which is the highestever utilisation achieved so far.Divisional margins maintainedThe sluggish demand in the domestic market, increased supplies and intense price competition put realisations under pressure. VFYprices continued to weaken throughout the first half of the current financial year. After having touched a low of Rs. 143/Kg in June 2000,VFY prices recovered gradually on the back of a gradual recovery in demand and diversion of supplies towards exports. During the secondhalf of the current financial year VFY prices have been rising and hit Rs.153/kg levels by March 2001. Realisation for the full year thusaveraged around Rs.148/Kg, which is still lower than the average realisation for FY 2000.Such a fall in realisation on a year-on-year basis against rising costs naturally impacted VFY margins adversely. These declined from17 per cent in FY 2000 to 13 per cent in FY 2001. The sharp rise in costs of wood pulp, water and power could not be fully offset byimproved efficiencies. At Veraval, the impending water crisis, due to the drought could be avoided through the commissioning of thedesalination plant, but because of the cost involved, it had a negative impact.Despite this erosion in VFY margins, divisional margins could be maintained at 23 per cent, largely due to the improved realisationfor caustic and chloric products as well as better operations at the captive power plant. A favourable change in the demand-supply forcaustic/chlorine products led to a quantum jump in prices of caustic soda, chlorine and hydrochloric acid. The reduced energy costs (betterefficiency, higher PLF and increased use of lignite at the captive power plant) also enabled the Division fully offset the impact of fall in VFYmargins. The margins could have been even better, but for planned shutdown of one-third of caustic soda capacities for membranereplacement (for about 20 days) during the fourth quarter of the current financial year.The outlook for the VFY business remains challenging. Changing fashion trends, competition from Polyester Filament Yarn (PFY), bothin the domestic and export markets are affecting its growth potential. The prevailing gap in prices of VFY and PFY is substantial and is furthercompounding the issue, inducing as it does customers to shift from VFY to PFY. As a result, the recovery in domestic demand is slow.In the interim period, volume growth will be driven by the Division’s ability to heighten export presence. The export markets offerprofitable opportunities for growth. Realignment of VFY capacities taking place abroad and several capacities in the West being closeddown for cost reasons, offer enormous growth opportunities for quality conscious producers like Indian Rayon.

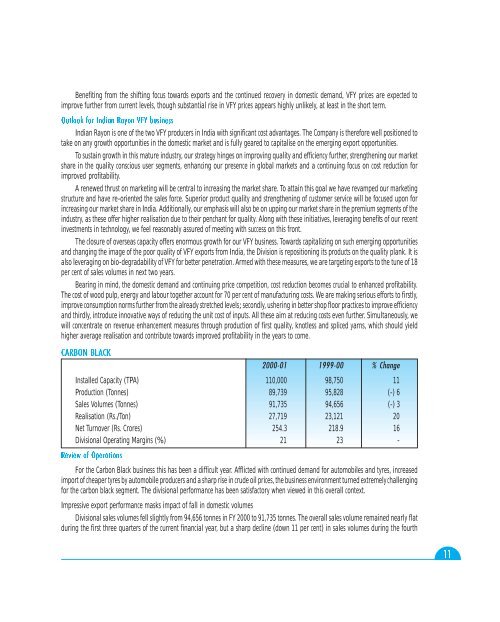

Benefiting from the shifting focus towards exports and the continued recovery in domestic demand, VFY prices are expected toimprove further from current levels, though substantial rise in VFY prices appears highly unlikely, at least in the short term.Outlook for Indian Rayon VFY businessIndian Rayon is one of the two VFY producers in India with significant cost advantages. The Company is therefore well positioned totake on any growth opportunities in the domestic market and is fully geared to capitalise on the emerging export opportunities.To sustain growth in this mature industry, our strategy hinges on improving quality and efficiency further, strengthening our marketshare in the quality conscious user segments, enhancing our presence in global markets and a continuing focus on cost reduction forimproved profitability.A renewed thrust on marketing will be central to increasing the market share. To attain this goal we have revamped our marketingstructure and have re-oriented the sales force. Superior product quality and strengthening of customer service will be focused upon forincreasing our market share in India. Additionally, our emphasis will also be on upping our market share in the premium segments of theindustry, as these offer higher realisation due to their penchant for quality. Along with these initiatives, leveraging benefits of our recentinvestments in technology, we feel reasonably assured of meeting with success on this front.The closure of overseas capacity offers enormous growth for our VFY business. Towards capitalizing on such emerging opportunitiesand changing the image of the poor quality of VFY exports from India, the Division is repositioning its products on the quality plank. It isalso leveraging on bio-degradability of VFY for better penetration. Armed with these measures, we are targeting exports to the tune of 18per cent of sales volumes in next two years.Bearing in mind, the domestic demand and continuing price competition, cost reduction becomes crucial to enhanced profitability.The cost of wood pulp, energy and labour together account for 70 per cent of manufacturing costs. We are making serious efforts to firstly,improve consumption norms further from the already stretched levels; secondly, ushering in better shop floor practices to improve efficiencyand thirdly, introduce innovative ways of reducing the unit cost of inputs. All these aim at reducing costs even further. Simultaneously, wewill concentrate on revenue enhancement measures through production of first quality, knotless and spliced yarns, which should yieldhigher average realisation and contribute towards improved profitability in the years to come.CARBON BLACK2000-01 1999-00 % ChangeInstalled Capacity (TPA) 110,000 98,750 11Production (Tonnes) 89,739 95,828 (-) 6Sales Volumes (Tonnes) 91,735 94,656 (-) 3Realisation (Rs./Ton) 27,719 23,121 20Net Turnover (Rs. Crores) 254.3 218.9 16Divisional Operating Margins (%) 21 23 -Review of OperationsFor the Carbon Black business this has been a difficult year. Afflicted with continued demand for automobiles and tyres, increasedimport of cheaper tyres by automobile producers and a sharp rise in crude oil prices, the business environment turned extremely challengingfor the carbon black segment. The divisional performance has been satisfactory when viewed in this overall context.Impressive export performance masks impact of fall in domestic volumesDivisional sales volumes fell slightly from 94,656 tonnes in FY 2000 to 91,735 tonnes. The overall sales volume remained nearly flatduring the first three quarters of the current financial year, but a sharp decline (down 11 per cent) in sales volumes during the fourth11