quarter dragged overall volumes down marginally. Continued poor demand for tyres in the local market, which in turn is attributed tolower production of automobiles during this year was the main cause. While the automobile industry registered a negative growth of 18per cent, the heavy commercial vehicle segment, its biggest user industry, registered a fall of 18 per cent in production volumes during theyear. On top of this, demand for carbon black in the replacement tyre market also declined as a result of the lacklustre economic activityand the resultant slowdown in goods movement across the country. Hence, domestic sales volumes at 76,019 tonnes were lower by almost12 per cent vis-a-vis 85,887 tonnes attained in the previous year.A phenomenal rise in exports at 15,716 tonnes, which is up by 79 per cent from 8,769 tonnes in FY 2000 offset the impact. Throughaggressive marketing efforts and a successful reach into the new export markets of Asia and Europe, the Division could achieve suchpathbreaking results. Towards this end leveraging the locational advantage of the Company’s Chennai plant has been a major contributor.In keeping with market needs, overall production shrunk by 6 per cent from 95,828 tonnes in FY 2000 to 89,739 tonnes in FY 2001.Rise in Global CBFS prices put further pressureA sharp rise in input costs compounded the Division’s handicap. Carbon Black Feed Stock (CBFS) prices shot up form a level ofUS$125 per tonne in March 2000 to a high of US$181 per tonne in September 2000. These started declining from the 4QFY 2001onwards. CBFS prices which averaged around US$163 per tonne for the year, reflect an increase of 30 per cent YoY. CBFS pricesaccount for 83 per cent of the production costs. The sharp rise in global CBFS prices and the depreciation of the Indian Rupee againstthe US$, affected costs severely.Realisation up 20 per centAlthough the increase in cost was passed on to the customers, the markets could absorb only a part of it as demand in the localmarkets was unfavourable along with competition in export markets. However even reflecting the partial passing of the cost increases, theaverage realisation was up 20 per cent YoY, from Rs.23,121 per tonne to Rs.27,719 per tonne.Margins under pressure, per ton profits maintainedGiven the pass through nature of these price increases as well as the partial absorption of cost increases by the Company, divisionaloperating margins declined from 23.2 per cent in FY 2000 to 20.6 per cent in FY 2001. The fall would have been steeper, but for higherrealisation (passing of costs) and the significant improvement in operational efficiency at both of its plants in Chennai and Renukoot. Thesourcing of CBFS from the domestic markets as well as the introduction of bulk packaging system which reduced packing costs, havecontributed towards arresting the margin fall. Despite lower operating margins, per tonne profits have been improved at Rs. 5,700 pertonne in comparison to Rs.5,364 per tonne during the last year.CBFS prices have softened now and are hovering around US$ 155 per tonne. This development, if sustained, will have a positivebearing on the divisional margins in future.Sector OutlookThe long-term outlook for the Carbon Black industry is positive, though it may have bumpy rides in the short term. The automobilesector continues to reel under the pressures of economic recession. The reduced demand of the goods movement through heavy vehicles,coupled with improved railway efficiency is affecting the need for tyres in the replacement markets. Cheaper import of tyres by automobilemanufacturers will stunt the demand for carbon black in India. In such an environment, the only viable alternative to remain profitableis to concentrate on exports. The softening of global CBFS prices, which has started falling with the tempering of global crude oil prices,should bring succour to carbon black manufacturers in terms of reduced pressure on costs and margins in future.Outlook for Indian Rayon’s Carbon Black BusinessGoing forward, Indian Rayon’s strategy will be to focus on volume growth through increased share of exports, development of nontyreapplications, improved realisations and tighten cost structure for enhanced profitability.123 12

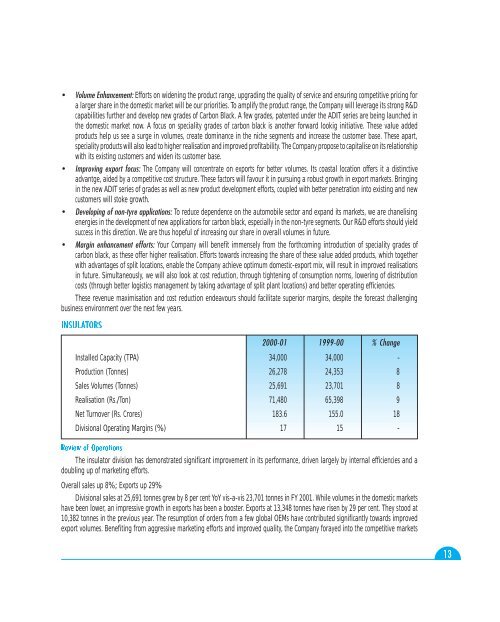

• Volume Enhancement: Efforts on widening the product range, upgrading the quality of service and ensuring competitive pricing fora larger share in the domestic market will be our priorities. To amplify the product range, the Company will leverage its strong R&Dcapabilities further and develop new grades of Carbon Black. A few grades, patented under the ADIT series are being launched inthe domestic market now. A focus on speciality grades of carbon black is another forward lookig initiative. These value addedproducts help us see a surge in volumes, create dominance in the niche segments and increase the customer base. These apart,speciality products will also lead to higher realisation and improved profitability. The Company propose to capitalise on its relationshipwith its existing customers and widen its customer base.• Improving export focus: The Company will concentrate on exports for better volumes. Its coastal location offers it a distinctiveadvantge, aided by a competitive cost structure. These factors will favour it in pursuing a robust growth in export markets. Bringingin the new ADIT series of grades as well as new product development efforts, coupled with better penetration into existing and newcustomers will stoke growth.• Developing of non-tyre applications: To reduce dependence on the automobile sector and expand its markets, we are chanelisingenergies in the development of new applications for carbon black, especially in the non-tyre segments. Our R&D efforts should yieldsuccess in this direction. We are thus hopeful of increasing our share in overall volumes in future.• Margin enhancement efforts: Your Company will benefit immensely from the forthcoming introduction of speciality grades ofcarbon black, as these offer higher realisation. Efforts towards increasing the share of these value added products, which togetherwith advantages of split locations, enable the Company achieve optimum domestic-export mix, will result in improved realisationsin future. Simultaneously, we will also look at cost reduction, through tightening of consumption norms, lowering of distributioncosts (through better logistics management by taking advantage of split plant locations) and better operating efficiencies.These revenue maximisation and cost reduction endeavours should facilitate superior margins, despite the forecast challengingbusiness environment over the next few years.INSULATORS2000-01 1999-00 % ChangeInstalled Capacity (TPA) 34,000 34,000 -Production (Tonnes) 26,278 24,353 8Sales Volumes (Tonnes) 25,691 23,701 8Realisation (Rs./Ton) 71,480 65,398 9Net Turnover (Rs. Crores) 183.6 155.0 18Divisional Operating Margins (%) 17 15 -Review of OperationsThe insulator division has demonstrated significant improvement in its performance, driven largely by internal efficiencies and adoubling up of marketing efforts.Overall sales up 8%; Exports up 29%Divisional sales at 25,691 tonnes grew by 8 per cent YoY vis-a-vis 23,701 tonnes in FY 2001. While volumes in the domestic marketshave been lower, an impressive growth in exports has been a booster. Exports at 13,348 tonnes have risen by 29 per cent. They stood at10,382 tonnes in the previous year. The resumption of orders from a few global OEMs have contributed significantly towards improvedexport volumes. Benefiting from aggressive marketing efforts and improved quality, the Company forayed into the competitive markets13