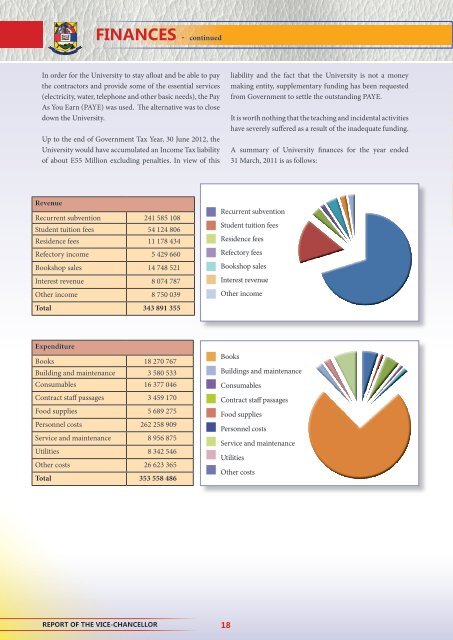

FINANCES - continuedIn order for the University to stay afloat and be able to paythe contractors and provide some of the essential services(electricity, water, telephone and other basic needs), the PayAs You Earn (PAYE) was used. The alternative was to closedown the University.Up to the end of Government Tax Year, 30 June 2012, theUniversity would have accumulated an Income Tax liabilityof about E55 Million excluding penalties. In view of thisliability and the fact that the University is not a moneymaking entity, supplementary funding has been requestedfrom Government to settle the outstanding PAYE.It is worth nothing that the teaching and incidental activitieshave severely suffered as a result of the inadequate funding.A summary of University finances for the year ended31 March, 2011 is as follows:RevenueRecurrent subvention 241 585 108Student tuition fees 54 124 806Residence fees 11 178 434Refectory income 5 429 660Bookshop sales 14 748 521Interest revenue 8 074 787Other income 8 750 039Total 343 891 355Recurrent subventionStudent tuition feesResidence feesRefectory feesBookshop salesInterest revenueOther incomeExpenditureBooks 18 270 767Building and maintenance 3 580 533Consumables 16 377 046Contract staff passages 3 459 170Food supplies 5 689 275Personnel costs 262 258 909Service and maintenance 8 956 875Utilities 8 342 546Other costs 26 623 365Total 353 558 486BooksBuildings and maintenanceConsumablesContract staff passagesFood suppliesPersonnel costsService and maintenanceUtilitiesOther costsREPORT OF THE VICE-CHANCELLOR 18

INTERNAL AUDITMr. S.H. Dlamini - Internal AuditorThe University Council, in seeking to ensureeffective corporate governance and adoption ofworld best practice, has long been committed toestablishing and maintaining effective internal control inorder to prevent fraud, waste, abuse and mismanagementin its operations.In 1999, the Audit Committee was established to provideassurance regarding the quality and reliability of boththe financial information used by Council and financialstatements issued by the University.Within the broad areas of responsibility, the activitiesperformed by the Audit Committee include;Assessing and reviewing the risk management processof the University;Reviewing reports from internal and external auditorsto ensure that, where major deficiencies or breakdownsin controls and procedures have been identified, anappropriate remedial action is taken by management;Reviewing the accounting policies and proceduresadopted by the University and any proposed changes;Oversee the internal audit function;Report to Council on its statutory mandate and otherduties; andEnsure that the combined assurance model is applied toprovide coordinated approach to all assurance activities.In the discharge of its responsibilities, the Audit Committeeestablished an Internal Audit function, first outsourcedand now conducted in-house. The Internal Audit team iscurrently comprised of four committed and dedicated staffmembers.The aim of the Internal Audit is to assist managementat all levels with information on the establishment andmaintenance of adequate internal control systems over allactivities and to ensure that these activities are carried outefficiently and effectively.Internal Audit assists the management of the Universityto meet its responsibilities effectively by evaluatingfinancial, managerial and operating information, makingrecommendations for improvement of systems andprocedures, and providing other information aimed atpromoting effective control by reducing risk at a reasonablecost.Internal Audit considers risks in general, monitors theUniversity’s activities on the terrain of risk management,and makes recommendations to management, the ViceChancellor, and the Audit Committee to reduce oreliminate the risk.The Internal Audit, however, is neither an extension nor asubstitute for good management, though it has a significantrole in advising management. It is mainly responsible forevaluating and reporting to management, Vice Chancellor,and the Audit Committee and thereby providing themwith assurance on processes of risk management, control,governance and value for money. It however remains theduty of management, not Internal Audit, to operate theseprocesses (controls and procedures), to determine whetheror not to accept audit recommendations, and to recognizeand accept risks of not taking action.19REPORT OF THE VICE-CHANCELLOR