- Page 1:

S : Sf:' ;: W^W't-^WW': ;, S 4 Si :

- Page 5:

unitedminds

- Page 9 and 10:

Economic Report of the PresidentTo

- Page 11:

the Technology Reinvestment Project

- Page 14:

formed health care system, increase

- Page 19 and 20:

CONTENTSPageCHAPTER 1. A STRATEGY F

- Page 21:

PageProviding Comprehensive Benefit

- Page 24 and 25:

LIST OF CHARTS—CONTINUEDPage3-5 L

- Page 27 and 28:

CHAPTER 1A Strategy for Growth and

- Page 29 and 30:

which have left consumers and busin

- Page 31 and 32:

that growth in both real compensati

- Page 33 and 34:

for inflation was on average roughl

- Page 35 and 36:

Box 1-2.—Saving, Investment, and

- Page 37 and 38:

investments in human capital; inves

- Page 39 and 40:

of the income distribution (Table 1

- Page 41 and 42:

Box 1-3.—Credible Deficit Reducti

- Page 43 and 44:

Chart 1-7 Correlation of Investment

- Page 45 and 46:

Box 1~4*~-A Balanced Budget Amendme

- Page 47 and 48: This educational record is not good

- Page 49 and 50: fallen markedly since the 1960s (Ch

- Page 51 and 52: The development and deployment of n

- Page 53 and 54: Earlier rounds of GATT talks had fo

- Page 55 and 56: Chart 1-10 Projected Real Growth Ra

- Page 57 and 58: are therefore on the public dole. M

- Page 59: prise communities and be granted sm

- Page 62 and 63: ingredient that should allow the ec

- Page 64 and 65: Chart 2-2 National Defense Purchase

- Page 66 and 67: Chart 2-3 Growth of U.S. Merchandis

- Page 68 and 69: Chart 2-5 Households: Credit Market

- Page 70 and 71: THE HEADWINDS ARE MOSTLY CALMINGAs

- Page 72 and 73: 1993, real consumer spending increa

- Page 74 and 75: RESIDENTIAL INVESTMENTResidential i

- Page 76 and 77: smallest annual increase in 20 year

- Page 78 and 79: ments with the Internal Revenue Ser

- Page 80 and 81: safe-harbor rules for underpayment

- Page 82 and 83: Chart 2-9 Alternative Measures of t

- Page 84 and 85: Meanwhile, the Mountain States were

- Page 86 and 87: inflation is measured by the Blue C

- Page 88 and 89: Saving, Investment, and Capital Acc

- Page 90 and 91: the future should be reflected in l

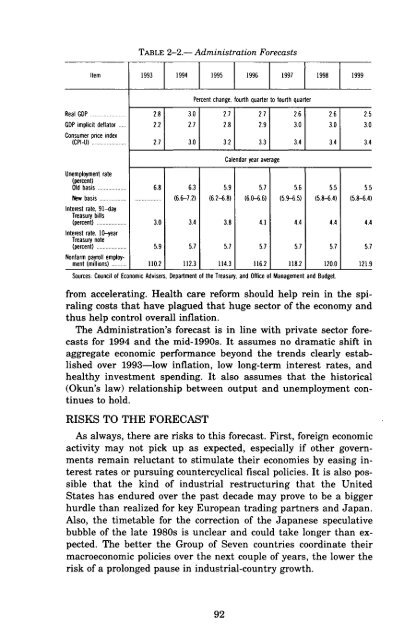

- Page 92 and 93: Chart 2-15 Dynamic Effects of Defic

- Page 94 and 95: joyed healthy average real GDP grow

- Page 96 and 97: Chart 2-16 Personal Income Taxes as

- Page 100 and 101: TABLE 2-3.— Accounting for Growth

- Page 103 and 104: CHAPTER 3Trends and Recent Developm

- Page 105 and 106: first quarter of 1991, nonfarm payr

- Page 107 and 108: cause defense cutbacks have caused

- Page 109 and 110: UNEMPLOYMENT AND NONEMPLOYMENTThe U

- Page 111 and 112: Chart 3-3 Civilian Unemployment Rat

- Page 113 and 114: Chart 3-6 Employment-to-Population

- Page 115 and 116: Chart 3-8 Ratio of White-Collar to

- Page 117 and 118: than would be expected given its hi

- Page 119 and 120: that the natural rate is falling? M

- Page 121 and 122: SLOW INCOME GROWTHIncome trends hav

- Page 123 and 124: Chart 3-10 Average Annual Growth of

- Page 125 and 126: Box 3-3.—Consequences of Producti

- Page 127 and 128: likely that immigration could expla

- Page 129 and 130: We do, however, know how many worke

- Page 131 and 132: size. No data are available on vola

- Page 133 and 134: BENEFITSOne of the concerns raised

- Page 135 and 136: edented partnership to develop a nu

- Page 137 and 138: CHAPTER 4Health Care ReformTHE UNIT

- Page 139 and 140: make cost-conscious decisions. In a

- Page 141 and 142: A third rationale for universal cov

- Page 143 and 144: Box 4-1.—Moral Hazard and Adverse

- Page 145 and 146: ies depending on one's health statu

- Page 147 and 148: than people in other countries do,

- Page 149 and 150:

sumers are ill equipped to bring st

- Page 151 and 152:

By itself, the aging of the populat

- Page 153 and 154:

TABLE 4-3.- Sources and Uses of Hea

- Page 155 and 156:

about 65 to 70 cents for a typical

- Page 157 and 158:

THE ARCHITECTURE OF THE HEALTHSECUR

- Page 159 and 160:

etary savings for the Federal Gover

- Page 161 and 162:

contribution, within limits. Outsid

- Page 163 and 164:

salary income, payments from the em

- Page 165 and 166:

TABLE 4-6.—Caps on Premiums by Fi

- Page 167 and 168:

An example will illustrate the proc

- Page 169 and 170:

TABLE 4-9.—Sources and Uses of Fe

- Page 171 and 172:

Chart 4-9 Business Spending on Heal

- Page 173:

Health care reform should set the s

- Page 176 and 177:

and private sectors, addressing env

- Page 178 and 179:

Box 5-1.—Selected National Perfor

- Page 180 and 181:

Box 5-2*—Market PowerFirms are sa

- Page 182 and 183:

ate regulation. For example, State

- Page 184 and 185:

competitiveness of U.S. industry, a

- Page 186 and 187:

Box 5-4.—ExternalitiesAn external

- Page 188 and 189:

in the habitat of the spotted owl r

- Page 190 and 191:

CLIMATE CHANGE ACTION PLANCertain g

- Page 192 and 193:

eral, lays a foundation for broader

- Page 194 and 195:

The Administration's proposal seeks

- Page 196 and 197:

vances in technical know-how have a

- Page 198 and 199:

Investments in R&D are risky. Like

- Page 200 and 201:

1950s and 1960s, and American compa

- Page 202 and 203:

ico and Lawrence Livermore in Calif

- Page 204 and 205:

of industry. MOCs will be affiliate

- Page 206 and 207:

tiveness. Again, the hoped-for resu

- Page 208 and 209:

forts to cut the massive Federal bu

- Page 210 and 211:

TECHNOLOGY POLICY, GROWTH, ANDCOMPE

- Page 212 and 213:

mitment to an open international tr

- Page 214 and 215:

ses, which take such intersectoral

- Page 216 and 217:

An important sectoral development i

- Page 218 and 219:

TABLE 6-3.—Stock of U.S. Outward

- Page 220 and 221:

technical change has been offered a

- Page 222 and 223:

ent account is a broader measure of

- Page 224 and 225:

TABLE 6-6.—Intrafirm Trade as Sha

- Page 226 and 227:

greater access to the Japanese mark

- Page 228 and 229:

the transparency of its trade regim

- Page 230 and 231:

that if the states of the former So

- Page 232 and 233:

Box 6-3.—Mexican Economic Reforms

- Page 234 and 235:

1998, while nontariff barriers on a

- Page 236 and 237:

ward convergence in environmental a

- Page 238 and 239:

Box 6-4.—The Asian "Miracle"Per c

- Page 240 and 241:

Box 6-5.—The Economic Impact of t

- Page 242 and 243:

development, and environmental clea

- Page 244 and 245:

THE TRADE POLICY AGENDABy lowering

- Page 246 and 247:

ignated monopolies. It also establi

- Page 248 and 249:

The dollar ended 1993 roughly where

- Page 250 and 251:

Box 6-7.—Exchange-Rate Volatility

- Page 252 and 253:

Chart 6-5 French Franc-Deutsche Mar

- Page 254 and 255:

Besides bringing these endeavors to

- Page 257 and 258:

LETTER OF TRANSMITTALCOUNCIL OF ECO

- Page 259 and 260:

Report to the President on the Acti

- Page 261 and 262:

duction budget package, the North A

- Page 263 and 264:

Working Group studying cost-benefit

- Page 265 and 266:

prepares the Economic Indicators an

- Page 267:

Appendix BSTATISTICAL TABLES RELATI

- Page 270 and 271:

POPULATION, EMPLOYMENT, WAGES, AND

- Page 272 and 273:

AGRICULTURE:PageB-96. Farm income,

- Page 274 and 275:

NATIONAL INCOME OR EXPENDITURETABLE

- Page 276 and 277:

TABLE B-2.—Gross domestic product

- Page 278 and 279:

TABLE B-3.—Implicit price deflato

- Page 280 and 281:

TABLE B-4.—Fixed-weighted price i

- Page 282 and 283:

TABLE B-5.—Changes in gross domes

- Page 284 and 285:

TABLE B-7.—Cross domestic product

- Page 286 and 287:

TABLE B-9.—Gross domestic product

- Page 288 and 289:

TABLE B-ll.—Gross domestic produc

- Page 290 and 291:

TABLE B-13.—Gross domestic produc

- Page 292 and 293:

TABLE B-15.—Personal consumption

- Page 294 and 295:

TABLE B-17.—Gross and net private

- Page 296 and 297:

TABLE B-19.—Inventories and final

- Page 298 and 299:

TABLE B-21.—Foreign transactions

- Page 300 and 301:

TABLE B-23.—Relation of gross dom

- Page 302 and 303:

TABLE B-25.—National income by ty

- Page 304 and 305:

TABLE B-26.—Sources of personal i

- Page 306 and 307:

TABLE B-27.—Disposition of person

- Page 308 and 309:

TABLE B-29.—Gross sating and inve

- Page 310 and 311:

TABLE B-31.—Median money income (

- Page 312 and 313:

TABLE B-33.—Population and the la

- Page 314 and 315:

TABLE B-34.—Civilian employment a

- Page 316 and 317:

TABLE B-36.—Unemployment by demog

- Page 318 and 319:

TABLE B-38.—Civilian labor force

- Page 320 and 321:

TABLE B-40.—Civilian unemployment

- Page 322 and 323:

TABLE B-42.—Unemployment by durat

- Page 324 and 325:

TABLE B-44.—Employees on nonagric

- Page 326 and 327:

TABLE B-45.—Hours and earnings in

- Page 328 and 329:

TABLE B-47.—Productivity and rela

- Page 330 and 331:

PRODUCTION AND BUSINESS ACTIVITYTAB

- Page 332 and 333:

TABLE B-51.—Industrial production

- Page 334 and 335:

TABLE B-53.—New construction acti

- Page 336 and 337:

TABLE B-54.—New housing units sta

- Page 338 and 339:

Year or monthTABLE B-56.—Manufact

- Page 340 and 341:

TABLE B-58.—Manufacturers' new an

- Page 342 and 343:

TABLE B-60.—Consumer price indexe

- Page 344 and 345:

TABLE B-61.—Consumer price indexe

- Page 346 and 347:

TABLE B-63.—Changes in consumer p

- Page 348 and 349:

TABLE B-64.—Producer price indexe

- Page 350 and 351:

TABLE B-66.—Producer price indexe

- Page 352 and 353:

TABLE B-67.—Changes in producer p

- Page 354 and 355:

TABLE B-69.—Components of money s

- Page 356 and 357:

TABLE B-70.—Aggregate reserves of

- Page 358 and 359:

TABLE B-72.—Bond yields and inter

- Page 360 and 361:

TABLE B-73.—Total funds raised in

- Page 362 and 363:

TABLE B-74.—Mortgage debt outstan

- Page 364 and 365:

TABLE B-76.—Consumer credit outst

- Page 366 and 367:

TABLE B-78.—Federal receipts, out

- Page 368 and 369:

TABLE B-79.—Federal budget receip

- Page 370 and 371:

TABLE B-81.—Federal and State and

- Page 372 and 373:

TABLE B-83.—State and local gover

- Page 374 and 375:

TABLE B-85.—Interest-bearing publ

- Page 376 and 377:

TABLE B-87.—Estimated ownership o

- Page 378 and 379:

TABLE B-89.—Corporate profits by

- Page 380 and 381:

TABLE B-91.—Sales, profits, and s

- Page 382 and 383:

TABLE B-93.—Sources and uses of f

- Page 384 and 385:

TABLE B-95.—Business formation an

- Page 386 and 387:

19481949195019511952195319541955195

- Page 388 and 389:

TABLE B-99.—Indexes of prices rec

- Page 390 and 391:

TABLE B-101.— Farm business balan

- Page 392 and 393:

TABLE B-103.—U.S. international t

- Page 394 and 395:

TABLE B-104.—U.S. merchandise exp

- Page 396 and 397:

TABLE B-106.—U.S. merchandise exp

- Page 398 and 399:

TABLE B-108.—Industrial productio

- Page 400 and 401:

TABLE B-110.—Foreign exchange rat

- Page 402 and 403:

NATIONAL WEALTHTABLE B-l 12.—Nati

- Page 404:

SUPPLEMENTARY TABLETABLE B-114.—S