(WIP) ACC 350 Exam 1 Study Material

Work in Process

Work in Process

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

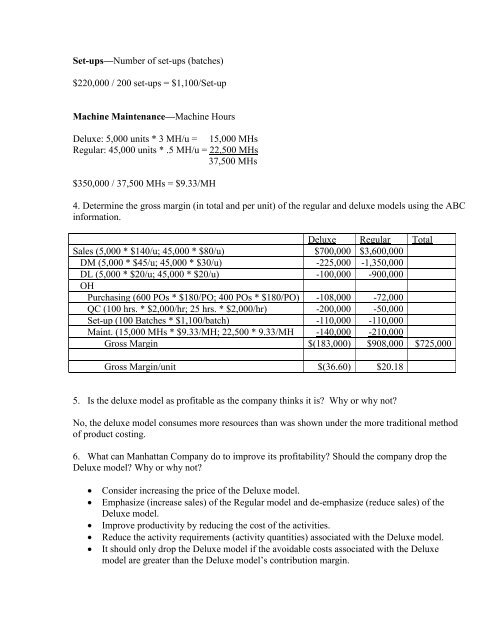

Set-ups—Number of set-ups (batches)<br />

$220,000 / 200 set-ups = $1,100/Set-up<br />

Machine Maintenance—Machine Hours<br />

Deluxe: 5,000 units * 3 MH/u = 15,000 MHs<br />

Regular: 45,000 units * .5 MH/u = 22,500 MHs<br />

37,500 MHs<br />

$<strong>350</strong>,000 / 37,500 MHs = $9.33/MH<br />

4. Determine the gross margin (in total and per unit) of the regular and deluxe models using the ABC<br />

information.<br />

Deluxe Regular Total<br />

Sales (5,000 * $140/u; 45,000 * $80/u) $700,000 $3,600,000<br />

DM (5,000 * $45/u; 45,000 * $30/u) -225,000 -1,<strong>350</strong>,000<br />

DL (5,000 * $20/u; 45,000 * $20/u) -100,000 -900,000<br />

OH<br />

Purchasing (600 POs * $180/PO; 400 POs * $180/PO) -108,000 -72,000<br />

QC (100 hrs. * $2,000/hr; 25 hrs. * $2,000/hr) -200,000 -50,000<br />

Set-up (100 Batches * $1,100/batch) -110,000 -110,000<br />

Maint. (15,000 MHs * $9.33/MH; 22,500 * 9.33/MH -140,000 -210,000<br />

Gross Margin $(183,000) $908,000 $725,000<br />

Gross Margin/unit $(36.60) $20.18<br />

5. Is the deluxe model as profitable as the company thinks it is? Why or why not?<br />

No, the deluxe model consumes more resources than was shown under the more traditional method<br />

of product costing.<br />

6. What can Manhattan Company do to improve its profitability? Should the company drop the<br />

Deluxe model? Why or why not?<br />

• Consider increasing the price of the Deluxe model.<br />

• Emphasize (increase sales) of the Regular model and de-emphasize (reduce sales) of the<br />

Deluxe model.<br />

• Improve productivity by reducing the cost of the activities.<br />

• Reduce the activity requirements (activity quantities) associated with the Deluxe model.<br />

• It should only drop the Deluxe model if the avoidable costs associated with the Deluxe<br />

model are greater than the Deluxe model’s contribution margin.