(WIP) ACC 350 Exam 1 Study Material

Work in Process

Work in Process

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

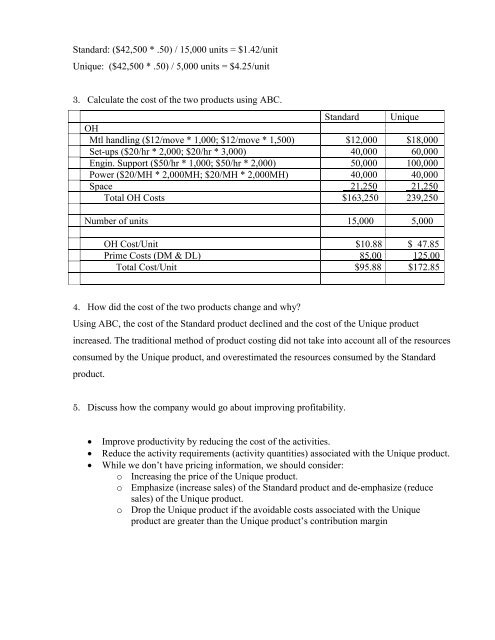

Standard: ($42,500 * .50) / 15,000 units = $1.42/unit<br />

Unique: ($42,500 * .50) / 5,000 units = $4.25/unit<br />

3. Calculate the cost of the two products using ABC.<br />

Standard Unique<br />

OH<br />

Mtl handling ($12/move * 1,000; $12/move * 1,500) $12,000 $18,000<br />

Set-ups ($20/hr * 2,000; $20/hr * 3,000) 40,000 60,000<br />

Engin. Support ($50/hr * 1,000; $50/hr * 2,000) 50,000 100,000<br />

Power ($20/MH * 2,000MH; $20/MH * 2,000MH) 40,000 40,000<br />

Space 21,250 21,250<br />

Total OH Costs $163,250 239,250<br />

Number of units 15,000 5,000<br />

OH Cost/Unit $10.88 $ 47.85<br />

Prime Costs (DM & DL) 85.00 125.00<br />

Total Cost/Unit $95.88 $172.85<br />

4. How did the cost of the two products change and why?<br />

Using ABC, the cost of the Standard product declined and the cost of the Unique product<br />

increased. The traditional method of product costing did not take into account all of the resources<br />

consumed by the Unique product, and overestimated the resources consumed by the Standard<br />

product.<br />

5. Discuss how the company would go about improving profitability.<br />

• Improve productivity by reducing the cost of the activities.<br />

• Reduce the activity requirements (activity quantities) associated with the Unique product.<br />

• While we don’t have pricing information, we should consider:<br />

o Increasing the price of the Unique product.<br />

o Emphasize (increase sales) of the Standard product and de-emphasize (reduce<br />

sales) of the Unique product.<br />

o Drop the Unique product if the avoidable costs associated with the Unique<br />

product are greater than the Unique product’s contribution margin