Market Outlook - BNP PARIBAS - Investment Services India

Market Outlook - BNP PARIBAS - Investment Services India

Market Outlook - BNP PARIBAS - Investment Services India

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

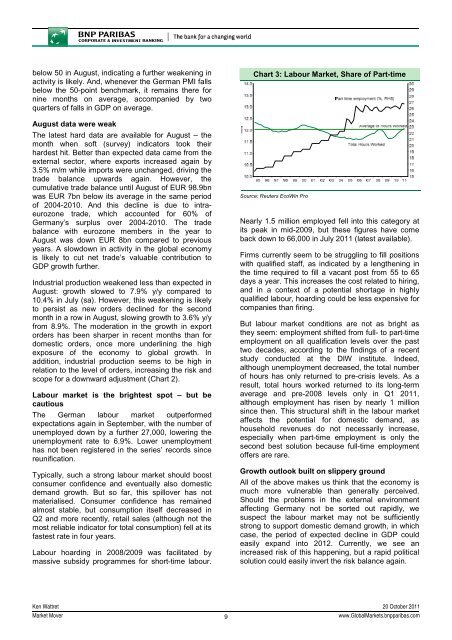

elow 50 in August, indicating a further weakening inactivity is likely. And, whenever the German PMI fallsbelow the 50-point benchmark, it remains there fornine months on average, accompanied by twoquarters of falls in GDP on average.August data were weakThe latest hard data are available for August – themonth when soft (survey) indicators took theirhardest hit. Better than expected data came from theexternal sector, where exports increased again by3.5% m/m while imports were unchanged, driving thetrade balance upwards again. However, thecumulative trade balance until August of EUR 98.9bnwas EUR 7bn below its average in the same periodof 2004-2010. And this decline is due to intraeurozonetrade, which accounted for 60% ofGermany’s surplus over 2004-2010. The tradebalance with eurozone members in the year toAugust was down EUR 8bn compared to previousyears. A slowdown in activity in the global economyis likely to cut net trade’s valuable contribution toGDP growth further.Industrial production weakened less than expected inAugust: growth slowed to 7.9% y/y compared to10.4% in July (sa). However, this weakening is likelyto persist as new orders declined for the secondmonth in a row in August, slowing growth to 3.6% y/yfrom 8.9%. The moderation in the growth in exportorders has been sharper in recent months than fordomestic orders, once more underlining the highexposure of the economy to global growth. Inaddition, industrial production seems to be high inrelation to the level of orders, increasing the risk andscope for a downward adjustment (Chart 2).Labour market is the brightest spot – but becautiousThe German labour market outperformedexpectations again in September, with the number ofunemployed down by a further 27,000, lowering theunemployment rate to 6.9%. Lower unemploymenthas not been registered in the series’ records sincereunification.Typically, such a strong labour market should boostconsumer confidence and eventually also domesticdemand growth. But so far, this spillover has notmaterialised. Consumer confidence has remainedalmost stable, but consumption itself decreased inQ2 and more recently, retail sales (although not themost reliable indicator for total consumption) fell at itsfastest rate in four years.Labour hoarding in 2008/2009 was facilitated bymassive subsidy programmes for short-time labour.Chart 3: Labour <strong>Market</strong>, Share of Part-timeSource: Reuters EcoWin ProNearly 1.5 million employed fell into this category atits peak in mid-2009, but these figures have comeback down to 66,000 in July 2011 (latest available).Firms currently seem to be struggling to fill positionswith qualified staff, as indicated by a lengthening inthe time required to fill a vacant post from 55 to 65days a year. This increases the cost related to hiring,and in a context of a potential shortage in highlyqualified labour, hoarding could be less expensive forcompanies than firing.But labour market conditions are not as bright asthey seem: employment shifted from full- to part-timeemployment on all qualification levels over the pasttwo decades, according to the findings of a recentstudy conducted at the DIW institute. Indeed,although unemployment decreased, the total numberof hours has only returned to pre-crisis levels. As aresult, total hours worked returned to its long-termaverage and pre-2008 levels only in Q1 2011,although employment has risen by nearly 1 millionsince then. This structural shift in the labour marketaffects the potential for domestic demand, ashousehold revenues do not necessarily increase,especially when part-time employment is only thesecond best solution because full-time employmentoffers are rare.Growth outlook built on slippery groundAll of the above makes us think that the economy ismuch more vulnerable than generally perceived.Should the problems in the external environmentaffecting Germany not be sorted out rapidly, wesuspect the labour market may not be sufficientlystrong to support domestic demand growth, in whichcase, the period of expected decline in GDP couldeasily expand into 2012. Currently, we see anincreased risk of this happening, but a rapid politicalsolution could easily invert the risk balance again.Ken Wattret 20 October 2011<strong>Market</strong> Mover9www.Global<strong>Market</strong>s.bnpparibas.com