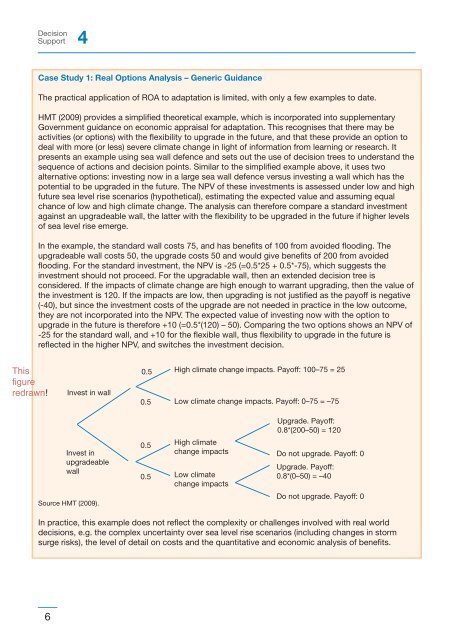

DecisionSupport 4Case Study 1: Real Options Analysis – Generic GuidanceThe practical application of ROA to adaptation is limited, with only a few examples to date.HMT (2009) provides a simplified theoretical example, which is <strong>in</strong>corporated <strong>in</strong>to supplementaryGovernment guidance on economic appraisal for adaptation. This recognises that there may beactivities (or options) with the flexibility to upgrade <strong>in</strong> the future, and that these provide an option todeal with more (or less) severe climate change <strong>in</strong> light of <strong>in</strong>formation from learn<strong>in</strong>g or research. Itpresents an example us<strong>in</strong>g sea w<strong>all</strong> defence and sets out the use of decision trees to understand thesequence of actions and decision po<strong>in</strong>ts. Similar to the simplified example above, it uses twoalternative options: <strong>in</strong>vest<strong>in</strong>g now <strong>in</strong> a large sea w<strong>all</strong> defence versus <strong>in</strong>vest<strong>in</strong>g a w<strong>all</strong> which has thepotential to be upgraded <strong>in</strong> the future. The NPV of these <strong>in</strong>vestments is assessed under low and highfuture sea level rise scenarios (hypothetical), estimat<strong>in</strong>g the expected value and assum<strong>in</strong>g equalchance of low and high climate change. The analysis can therefore compare a standard <strong>in</strong>vestmentaga<strong>in</strong>st an upgradeable w<strong>all</strong>, the latter with the flexibility to be upgraded <strong>in</strong> the future if higher levelsof sea level rise emerge.In the example, the standard w<strong>all</strong> costs 75, and has benefits of 100 from avoided flood<strong>in</strong>g. Theupgradeable w<strong>all</strong> costs 50, the upgrade costs 50 and would give benefits of 200 from avoidedflood<strong>in</strong>g. For the standard <strong>in</strong>vestment, the NPV is -25 (=0.5*25 + 0.5*-75), which suggests the<strong>in</strong>vestment should not proceed. For the upgradable w<strong>all</strong>, then an extended decision tree isconsidered. If the impacts of climate change are high enough to warrant upgrad<strong>in</strong>g, then the value ofthe <strong>in</strong>vestment is 120. If the impacts are low, then upgrad<strong>in</strong>g is not justified as the payoff is negative(-40), but s<strong>in</strong>ce the <strong>in</strong>vestment costs of the upgrade are not needed <strong>in</strong> practice <strong>in</strong> the low outcome,they are not <strong>in</strong>corporated <strong>in</strong>to the NPV. The expected value of <strong>in</strong>vest<strong>in</strong>g now with the option toupgrade <strong>in</strong> the future is therefore +10 (=0.5*(120) – 50). Compar<strong>in</strong>g the two options shows an NPV of-25 for the standard w<strong>all</strong>, and +10 for the flexible w<strong>all</strong>, thus flexibility to upgrade <strong>in</strong> the future isreflected <strong>in</strong> the higher NPV, and switches the <strong>in</strong>vestment decision.Thisfigureredrawn!Invest <strong>in</strong> w<strong>all</strong>0.50.5High climate change impacts. Payoff: 100–75 = 25Low climate change impacts. Payoff: 0–75 = –75Upgrade. Payoff:0.8*(200–50) = 120Invest <strong>in</strong>upgradeablew<strong>all</strong>0.50.5High climatechange impactsLow climatechange impactsDo not upgrade. Payoff: 0Upgrade. Payoff:0.8*(0–50) = –40Source HMT (2009).Do not upgrade. Payoff: 0In practice, this example does not reflect the complexity or ch<strong>all</strong>enges <strong>in</strong>volved with real worlddecisions, e.g. the complex uncerta<strong>in</strong>ty over sea level rise scenarios (<strong>in</strong>clud<strong>in</strong>g changes <strong>in</strong> stormsurge risks), the level of detail on costs and the quantitative and economic analysis of benefits.6

Real Options AnalysisCase Study 2: Real Options Guidance – Mov<strong>in</strong>g to PracticeThe previous example is relatively straightforward to solve because: only four <strong>in</strong>vestment options areconsidered, either <strong>in</strong>vest <strong>in</strong> a standard/upgradeable w<strong>all</strong>, with one sequential decision to upgrade;there are only two decision po<strong>in</strong>ts, i.e.: at t0, and at the upgrad<strong>in</strong>g moment; only two possibleuncerta<strong>in</strong> future states of the world can be realised, either ‘high’, or ‘low’ climate change impacts;the tim<strong>in</strong>g of learn<strong>in</strong>g is known; and at this time, uncerta<strong>in</strong>ty is fully resolved. A more realistic casestudy look<strong>in</strong>g at the optimal dike height under uncerta<strong>in</strong>ty with learn<strong>in</strong>g about climate changeimpacts is therefore presented below.Dike heighten<strong>in</strong>g is expensive, and economic<strong>all</strong>y efficient <strong>in</strong>vestment is therefore important. VanDantzig (1956) described that dike <strong>in</strong>vestment is a cost m<strong>in</strong>imisation problem, after a large flood<strong>in</strong>g <strong>in</strong>the Netherlands <strong>in</strong> 1953. In essence, higher dikes reduce expected damage costs, but <strong>in</strong>vestmentcosts <strong>in</strong>crease exponenti<strong>all</strong>y with dike height. A balance has to be found between expecteddamages and costs of dike construction over time, not<strong>in</strong>g decisions on dike height are recurrent for anumber of reasons (e.g. economic growth, climate change impacts on water levels, or soilsubsidence). On the one hand, it is not optimal to build a dike once and for <strong>all</strong> because that wouldresult <strong>in</strong> excessive <strong>in</strong>vestment costs with only little benefits. On the other hand, dike heighten<strong>in</strong>g, likemost large <strong>in</strong>vestment, has fixed costs, and therefore, yearly <strong>in</strong>vestment is not optimal but rather asolution where a dike is revised at longer time <strong>in</strong>tervals, for example, half a century.Crucial to determ<strong>in</strong>e optimal dike height over time are water level observations. With theseobservations return periods of different water levels can be estimated. Water defences protect<strong>in</strong>gland from large-scale flood<strong>in</strong>g events typic<strong>all</strong>y offer protection aga<strong>in</strong>st events with long returnperiods (e.g. 10000 years or even more), but these events are extremely rare, though they willbecome less rare <strong>in</strong> the future due to climate change.With climate change, sea levels are expected to rise, and peak river discharges are expected to<strong>in</strong>crease. These future scenarios have been projected, but are <strong>in</strong>sufficient to be valuable for a costbenefitapproach, as they require <strong>in</strong>formation on possible future states of the world and alsoprobabilities of these states. In the Bayesian literature these probabilities are c<strong>all</strong>ed <strong>in</strong>formed priors,or subjective probabilities. So far, subjective probability distributions are lack<strong>in</strong>g for the rate of sealevel rise or the <strong>in</strong>crease <strong>in</strong> peak discharges although that it is clear to some scenarios are much lesslikely than others. A second problem is that we poorly understand how / what / when we will learnabout climate change impacts. Some sources of uncerta<strong>in</strong>ty are likely to be reduced: water levelobservations will grow, reduc<strong>in</strong>g statistical uncerta<strong>in</strong>ty, and model structure uncerta<strong>in</strong>ty is likely to bereduced over time with research. If we know that better <strong>in</strong>formation will be available <strong>in</strong> the future, thismay have implications for current dike heighten<strong>in</strong>g decisions. As expla<strong>in</strong>ed previously, <strong>in</strong>formationhas expected value: once we know better dike heighten<strong>in</strong>g strategy can be adapted to reduce totalexpected costs.Nonetheless, with some prior distribution about the rate of the structural water level <strong>in</strong>crease, that isthe speed with which the relative water level is structur<strong>all</strong>y <strong>in</strong>creas<strong>in</strong>g, and assumptions about thelearn<strong>in</strong>g process, it is possible to <strong>in</strong>vestigate the problem of optimal dike height, and how valuable itis to obta<strong>in</strong> better knowledge on climate change impacts for the dike heighten<strong>in</strong>g problem: that is theexpected costs sav<strong>in</strong>gs that can be obta<strong>in</strong>ed by anticipat<strong>in</strong>g new <strong>in</strong>formation, and by chang<strong>in</strong>g thedike heighten<strong>in</strong>g strategy once <strong>in</strong>formation has been received. Furthermore, early <strong>in</strong>formation is morevaluable than late <strong>in</strong>formation because future costs are discounted. For this case study, we <strong>in</strong>troducea special case of learn<strong>in</strong>g: perfect learn<strong>in</strong>g, which we assume to be a probabilistic event follow<strong>in</strong>g asurvival model. The decision variable is the dike <strong>in</strong>crement , u t , the amount with which the dike isheightened, at any time t. The problem is discretised <strong>in</strong> sm<strong>all</strong> time steps , t k , and the decision spaceis discretised as well, u tk , E{0, ∆u, 2∆ u ,.., umax}. The left panel of Fig.1 shows a decision tree with7