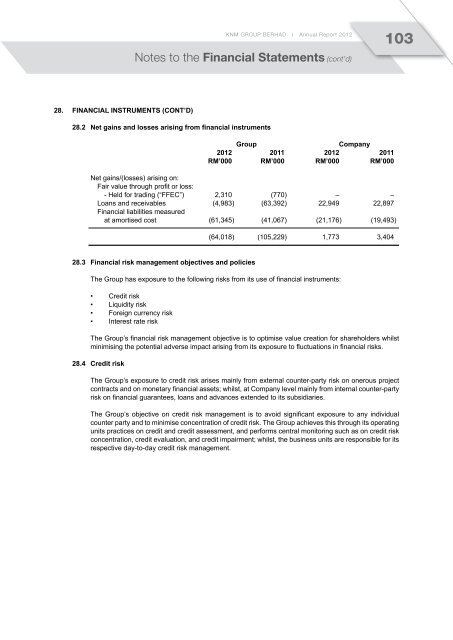

<strong>KNM</strong> GROUP BERHAD I Annual Report 2012103Notes to the Financial Statements (cont’d)28. Financial instruments (Cont’d)28.2 Net gains and losses arising from financial instrumentsGroupCompany2012 2011 2012 2011RM’000 RM’000 RM’000 RM’000Net gains/(losses) arising on:Fair value through profit or loss:- Held for trading (“FFEC”) 2,310 (770) – –Loans and receivables (4,983) (63,392) 22,949 22,897Financial liabilities measuredat amortised cost (61,345) (41,067) (21,176) (19,493)(64,018) (105,229) 1,773 3,40428.3 Financial risk management objectives and policiesThe Group has exposure to the following risks from its use of financial instruments:• Credit risk• Liquidity risk• Foreign currency risk• Interest rate riskThe Group’s financial risk management objective is to optimise value creation for shareholders whilstminimising the potential adverse impact arising from its exposure to fluctuations in financial risks.28.4 Credit riskThe Group’s exposure to credit risk arises mainly from external counter-party risk on onerous projectcontracts and on monetary financial assets; whilst, at Company level mainly from internal counter-partyrisk on financial guarantees, loans and advances extended to its subsidiaries.The Group’s objective on credit risk management is to avoid significant exposure to any individualcounter party and to minimise concentration of credit risk. The Group achieves this through its operatingunits practices on credit and credit assessment, and performs central monitoring such as on credit riskconcentration, credit evaluation, and credit impairment; whilst, the business units are responsible for itsrespective day-to-day credit risk management.

104<strong>KNM</strong> GROUP BERHAD I Annual Report 2012Notes to the Financial Statements (cont’d)28. Financial instruments (Cont’d)28.4 Credit risk (cont’d)Policies and ProcessesPolicies and processes in managing credit risk varies with the classes of counter-parties as outlinedbelow:Contract CustomersProcess & Specialised Equipment & Turnkey ContractsMost orders are treated as onerous construction contracts, where billings are based on the progressmilestones which typically are split into four or more stages of a project’s life cycle. Large order suchas EPC, billings are negotiated to closely mirror the cash flow requirements in contract execution.An advance from the customers would normally be required before the commencement of work, andsimilarly the customer would demand a Bank or Corporate Guarantee on its advancement made and/oras a form of guaranteeing performance. Customers’ orders are usually components of a larger projectwhich has secured financing. As such, credit risk exposure is typically low at the early and mid-stagesof a project life cycle, but increase towards the last milestone payment arising from possible variationor contractual disputes. This tail-end risk is managed or mitigated with one or more of the following:• Professional lien on goods and materials• Transactional credit documents (i.e. Letter of Credit) on export delivery• Contract customers are assessed on credit and sovereign nation risks where applicable on bothquantitative and qualitative elements.• Credit exposure is monitored on the aging of receivables, and the projects’ progression andvariations.Financial institutionsThe Group places its funds in Banks in over 19 countries in which it has business presence. The Groupalso enters into FOREX forward contracts with licensed financial institutions for hedging purposes.Credit risk is generally low as the counter parties are all reputable licensed institutions. Where financialderivatives are involved, mandatory ISDA agreements are incepted where necessary.Financial Guarantees and Advances for SubsidiariesThe Company through 2 (two) fully owned subsidiaries serves as central treasury to certain subsidiarieswithout external credit facilities by extending them loan, advances and banking trade facilities. Forthose subsidiaries with their own credit facilities, the Company is often required to provide corporateguarantee to the said banks extending such credit facilities. On the former, the Company enters intoformal agreement on pricing and repayment schedule, and continuously monitors the subsidiaries’performances, cash-flows and repayment. On the later, the Company continuously monitors thesubsidiaries’ performance and ability to service their credit obligations.The Group receives financial guarantees given by banks in managing exposure to credit risks. At theend of the reporting period, financial guarantees received by the Group amounted to RM28,863,000 (31December 2011: RM18,134,000; 1 January 2011: RM61,000) in respect of RM375,687,000 (31 December2011: RM334,700,000; 1 January 2011: RM254,689,000) trade receivables. The remaining balance oftrade receivables are not secured by any collateral or supported by any other credit enhancements.