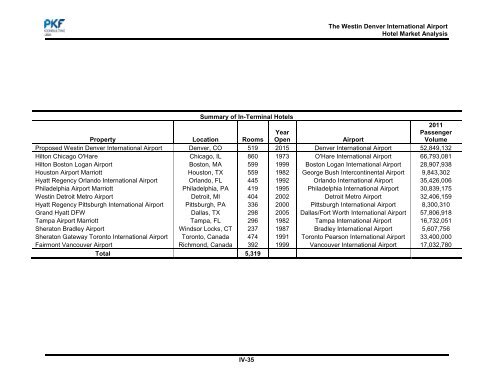

The Westin Denver International Airport<strong>Hotel</strong> <strong>Market</strong> <strong>Analysis</strong>Summary of In-Terminal <strong>Hotel</strong>s2011Property Location RoomsYearOpenAirportPassengerVolumeProposed Westin Denver International Airport Denver, CO 519 2015 Denver International Airport 52,849,132Hilton Chicago O'Hare Chicago, IL 860 1973 O'Hare International Airport 66,793,081Hilton Boston Logan Airport Boston, MA 599 1999 Boston Logan International Airport 28,907,938Houston Airport Marriott Houston, TX 559 1982 George Bush Intercontinental Airport 9,843,302Hyatt Regency Orl<strong>and</strong>o International Airport Orl<strong>and</strong>o, FL 445 1992 Orl<strong>and</strong>o International Airport 35,426,006Philadelphia Airport Marriott Philadelphia, PA 419 1995 Philadelphia International Airport 30,839,175Westin Detroit Metro Airport Detroit, MI 404 2002 Detroit Metro Airport 32,406,159Hyatt Regency Pittsburgh International Airport Pittsburgh, PA 336 2000 Pittsburgh International Airport 8,300,310Gr<strong>and</strong> Hyatt DFW Dallas, TX 298 2005 Dallas/Fort Worth International Airport 57,806,918Tampa Airport Marriott Tampa, FL 296 1982 Tampa International Airport 16,732,051Sheraton Bradley Airport Windsor Locks, CT 237 1987 Bradley International Airport 5,607,756Sheraton Gateway Toronto International Airport Toronto, Canada 474 1991 Toronto Pearson International Airport 33,400,000Fairmont Vancouver Airport Richmond, Canada 392 1999 Vancouver International Airport 17,032,780Total 5,319IV-35

The Westin Denver International Airport<strong>Hotel</strong> <strong>Market</strong> <strong>Analysis</strong>1. Historical Performance of the In-Terminal <strong>Hotel</strong>sPresented in the following table is the historical performance of the in-terminallodging market from 2007 through 2011, as well as YTD June 2011 <strong>and</strong> 2012.The Westin Denver International AirportHistorical Performance of the Competitive <strong>Market</strong>Annual Percent Occupied Percent <strong>Market</strong> Percent PercentYear Supply Change Rooms Change Occupancy ADR Change RevPAR Change2007 1,941,435 - 1,556,749 - 80.2% $164.46 - $131.87 -2008 1,941,435 0.0% 1,476,369 -5.2% 76.0% $160.58 -2.4% $122.11 -7.4%2009 1,941,435 0.0% 1,401,656 -5.1% 72.2% $140.74 -12.4% $101.61 -16.8%2010 1,941,435 0.0% 1,517,808 8.3% 78.2% $140.08 -0.5% $109.51 7.8%2011 1,941,435 0.0% 1,542,975 1.7% 79.5% $146.67 4.7% $116.57 6.4%CAGR 0.0% - -0.2% - - -2.8% - -3.0% -YTD Jun '11 970,718 - 784,654 - 80.8% $148.43 - $119.98 -YTD Jun '12 970,718 0.0% 791,873 0.9% 81.6% $150.62 1.5% $122.87 2.4%Source: <strong>PKF</strong> Consulting USA<strong>Dem<strong>and</strong></strong> at the in-terminal hotels decreased at a CAGR of 0.2 percent over the pastfive years with occupancy ranging from a low of 72.2 percent in 2009 to a high of80.2 percent in 2007. Similar to the performance of most lodging markets acrossthe U.S., dem<strong>and</strong> declined in 2008 <strong>and</strong> 2009 as a result of the economic downturn.The in-terminal hotels experienced a decline of 5.2 <strong>and</strong> 5.1 percent in 2008 <strong>and</strong>2009, respectively. As the economy began to improve <strong>and</strong> air travel returned toprior year levels, dem<strong>and</strong> at the in-terminal hotels increased 8.3 percent in 2010,resulting in an occupancy level of 78.2 percent. <strong>Dem<strong>and</strong></strong> further increased 1.7percent in 2011, resulting in an occupancy level of nearly 80 percent. Occupancyfor the in-terminal hotels remained flat over prior year levels at approximately 81percent through YTD June 2012. It is worth noting that an overall occupancy ofapproximately 80 percent represents the maximum level of performance for thissample of hotels given market segmentation <strong>and</strong> dem<strong>and</strong> seasonality <strong>and</strong> explainsthe flat five-year CAGR in dem<strong>and</strong> <strong>and</strong> minimal YTD dem<strong>and</strong> growth.It is also worth noting that over the five year historical period, the occupancy for thein-terminal hotels has averaged 77.2 percent <strong>and</strong> that the average size of the 12hotels is 443 rooms. When reviewing the local <strong>DIA</strong> competitive airport hotels, thefive year occupancy average was lower at 74 percent <strong>and</strong> yet the average hotel sizewas much smaller at 198 rooms. This indicates that there is a clear competitiveadvantage, which translates into an occupancy performance premium, for interminalhotels when compared to their respective competitors that are notphysically attached to the airport.ADR for the in-terminal hotels decreased at a CAGR of 2.8 percent between 2007<strong>and</strong> 2011. While the aggregate ADR was in the low to mid-$160 range in 2007 <strong>and</strong>IV-36