The Westin Denver International Airport<strong>Hotel</strong> <strong>Market</strong> <strong>Analysis</strong>The ADR for the competitive airport lodging market decreased at a CAGR of 4.1percent over the past five years with ADR ranging from a low of $106.34 in 2010 toa high of $131.93 in 2008. During the height of the Great Recession (2009), theidentified competitive market experienced a significant decline in ADR of 18.4percent. This decrease resulted in an ADR of $107.71, an approximately $24decline. The market ADR further declined 1.3 percent in 2010 to $106.34, the fiveyearlow ADR level achieved by the competitive airport lodging market. Throughyear-end 2011, ADR increased a modest 1.6 percent over prior year levels,resulting in an ADR of $108. Through YTD June 2012, ADR increased from$106.79 to $108.76 or 1.8 percent.As a result of fluctuations in occupancy <strong>and</strong> ADR, RevPAR declined at a CAGR of3.6 percent between 2007 <strong>and</strong> 2011. In 2009, the competitive market experienceda decline in RevPAR of 19.0 percent, primarily as a result of an 18.4 percentdecrease in ADR. Comparatively, the U.S. overall lodging market experienced adecline in RevPAR of only 16.7 percent during this time. Through YTD June 2012,RevPAR increased 2.1 percent over prior year levels, resulting in RevPAR of$83.17, which is below 2007 levels.A majority of dem<strong>and</strong> at the hotels comprising the competitive airport lodgingmarket is from the transient market segment (approximately 55 percent) with groupdem<strong>and</strong> representing the second largest market segment (approximately 30percent). Based on conversations with management of the competitive hotels, weunderst<strong>and</strong> that the airport lodging market attracts group business that prefers theconvenience of being near the airport. The remainder of dem<strong>and</strong> in the competitiveairport lodging market is comprised of contract/crew dem<strong>and</strong>. The competitiveairport lodging market also benefits from distressed passenger dem<strong>and</strong>, which iscreated due to flight cancellations which are primarily attributable to inclementweather <strong>and</strong> airplane mechanical malfunctions. <strong>Dem<strong>and</strong></strong> for the full-service hotelscomprising the competitive airport lodging market is typically highest between themonths of May <strong>and</strong> September.2. Competitive Downtown Lodging <strong>Market</strong>As previously stated, given the fact that the proposed Subject will represent thehighest quality hotel in the airport submarket, we have also identified a sample ofcompetitive full-service hotels in downtown Denver. While these hotels are locatedapproximately 25 miles from the proposed Subject, it is likely that the proposedSubject will compete with these hotels for group dem<strong>and</strong> associated mainly withcorporate groups <strong>and</strong> national associations that involve attendees that must travelto Denver by air. The Subject will also compete with these hotels for transientdem<strong>and</strong> that would prefer the convenience of an airport location but that have totravel downtown due to the current lack of quality, upper upscale accommodations<strong>and</strong>/or lack of Starwood affiliated, full-service hotels in the airport market. As aresult, a review of the performance of these hotels, both in aggregate <strong>and</strong> on anIV-15

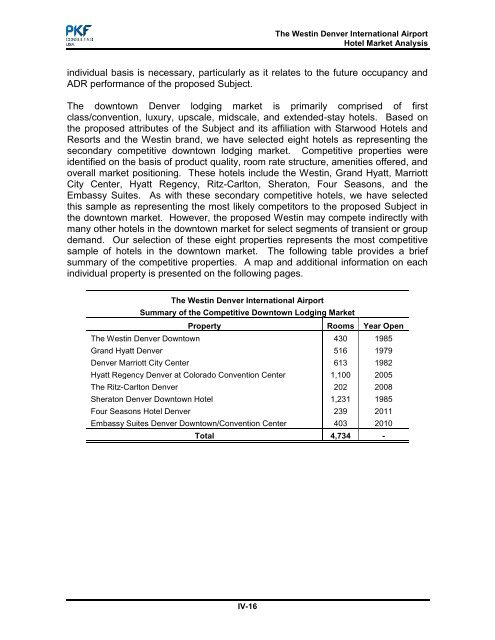

The Westin Denver International Airport<strong>Hotel</strong> <strong>Market</strong> <strong>Analysis</strong>individual basis is necessary, particularly as it relates to the future occupancy <strong>and</strong>ADR performance of the proposed Subject.The downtown Denver lodging market is primarily comprised of firstclass/convention, luxury, upscale, midscale, <strong>and</strong> extended-stay hotels. Based onthe proposed attributes of the Subject <strong>and</strong> its affiliation with Starwood <strong>Hotel</strong>s <strong>and</strong>Resorts <strong>and</strong> the Westin br<strong>and</strong>, we have selected eight hotels as representing thesecondary competitive downtown lodging market. Competitive properties wereidentified on the basis of product quality, room rate structure, amenities offered, <strong>and</strong>overall market positioning. These hotels include the Westin, Gr<strong>and</strong> Hyatt, MarriottCity Center, Hyatt Regency, Ritz-Carlton, Sheraton, Four Seasons, <strong>and</strong> theEmbassy Suites. As with these secondary competitive hotels, we have selectedthis sample as representing the most likely competitors to the proposed Subject inthe downtown market. However, the proposed Westin may compete indirectly withmany other hotels in the downtown market for select segments of transient or groupdem<strong>and</strong>. Our selection of these eight properties represents the most competitivesample of hotels in the downtown market. The following table provides a briefsummary of the competitive properties. A map <strong>and</strong> additional information on eachindividual property is presented on the following pages.The Westin Denver International AirportSummary of the Competitive Downtown Lodging <strong>Market</strong>Property Rooms Year OpenThe Westin Denver Downtown 430 1985Gr<strong>and</strong> Hyatt Denver 516 1979Denver Marriott City Center 613 1982Hyatt Regency Denver at Colorado Convention Center 1,100 2005The Ritz-Carlton Denver 202 2008Sheraton Denver Downtown <strong>Hotel</strong> 1,231 1985Four Seasons <strong>Hotel</strong> Denver 239 2011Embassy Suites Denver Downtown/Convention Center 403 2010Total 4,734 -IV-16