Gasoline Price Changes - Federal Trade Commission

Gasoline Price Changes - Federal Trade Commission

Gasoline Price Changes - Federal Trade Commission

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

THE DYNAMIC OF SUPPLY, DEMAND, AND COMPETITION<br />

from either West Coast refineries through a pipeline or other terminals by truck – both at higher<br />

cost. 14<br />

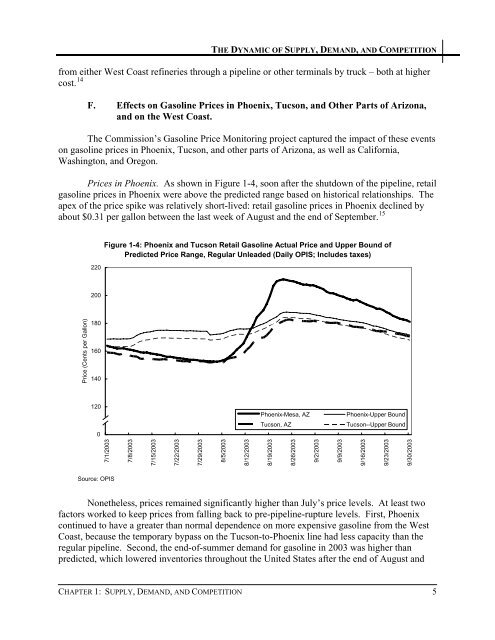

F. Effects on <strong>Gasoline</strong> <strong>Price</strong>s in Phoenix, Tucson, and Other Parts of Arizona,<br />

and on the West Coast.<br />

The <strong>Commission</strong>’s <strong>Gasoline</strong> <strong>Price</strong> Monitoring project captured the impact of these events<br />

on gasoline prices in Phoenix, Tucson, and other parts of Arizona, as well as California,<br />

Washington, and Oregon.<br />

<strong>Price</strong>s in Phoenix. As shown in Figure 1-4, soon after the shutdown of the pipeline, retail<br />

gasoline prices in Phoenix were above the predicted range based on historical relationships. The<br />

apex of the price spike was relatively short-lived: retail gasoline prices in Phoenix declined by<br />

about $0.31 per gallon between the last week of August and the end of September. 15<br />

<strong>Price</strong> (Cents per Gallon)<br />

220<br />

200<br />

180<br />

160<br />

140<br />

120<br />

100 0<br />

7/1/2003<br />

Source: OPIS<br />

Figure 1-4: Phoenix and Tucson Retail <strong>Gasoline</strong> Actual <strong>Price</strong> and Upper Bound of<br />

Predicted <strong>Price</strong> Range, Regular Unleaded (Daily OPIS; Includes taxes)<br />

7/8/2003<br />

7/15/2003<br />

7/22/2003<br />

7/29/2003<br />

8/5/2003<br />

8/12/2003<br />

Phoenix-Mesa, AZ Phoenix-Upper Bound<br />

Tucson, AZ Tucson--Upper Bound<br />

Nonetheless, prices remained significantly higher than July’s price levels. At least two<br />

factors worked to keep prices from falling back to pre-pipeline-rupture levels. First, Phoenix<br />

continued to have a greater than normal dependence on more expensive gasoline from the West<br />

Coast, because the temporary bypass on the Tucson-to-Phoenix line had less capacity than the<br />

regular pipeline. Second, the end-of-summer demand for gasoline in 2003 was higher than<br />

predicted, which lowered inventories throughout the United States after the end of August and<br />

CHAPTER 1: SUPPLY, DEMAND, AND COMPETITION 5<br />

8/19/2003<br />

8/26/2003<br />

9/2/2003<br />

9/9/2003<br />

9/16/2003<br />

9/23/2003<br />

9/30/2003