Gasoline Price Changes - Federal Trade Commission

Gasoline Price Changes - Federal Trade Commission

Gasoline Price Changes - Federal Trade Commission

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Price</strong> (Cents per Gallon)<br />

220<br />

200<br />

180<br />

160<br />

140<br />

120<br />

100 0<br />

7/1/2003<br />

7/8/2003<br />

7/15/2003<br />

7/22/2003<br />

7/29/2003<br />

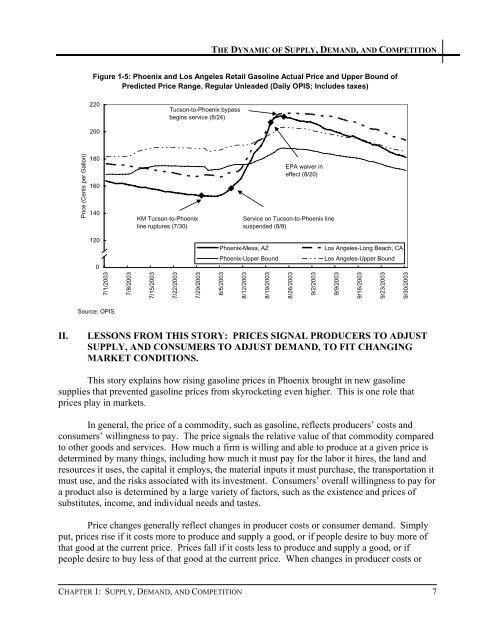

THE DYNAMIC OF SUPPLY, DEMAND, AND COMPETITION<br />

Figure 1-5: Phoenix and Los Angeles Retail <strong>Gasoline</strong> Actual <strong>Price</strong> and Upper Bound of<br />

Predicted <strong>Price</strong> Range, Regular Unleaded (Daily OPIS; Includes taxes)<br />

Source: OPIS<br />

KM Tucson-to-Phoenix<br />

line ruptures (7/30)<br />

Tucson-to-Phoenix bypass<br />

begins service (8/24)<br />

8/5/2003<br />

8/12/2003<br />

8/19/2003<br />

EPA waiver in<br />

effect (8/20)<br />

Service on Tucson-to-Phoenix line<br />

suspended (8/8)<br />

Phoenix-Mesa, AZ Los Angeles-Long Beach, CA<br />

Phoenix-Upper Bound Los Angeles-Upper Bound<br />

II. LESSONS FROM THIS STORY: PRICES SIGNAL PRODUCERS TO ADJUST<br />

SUPPLY, AND CONSUMERS TO ADJUST DEMAND, TO FIT CHANGING<br />

MARKET CONDITIONS.<br />

This story explains how rising gasoline prices in Phoenix brought in new gasoline<br />

supplies that prevented gasoline prices from skyrocketing even higher. This is one role that<br />

prices play in markets.<br />

In general, the price of a commodity, such as gasoline, reflects producers’ costs and<br />

consumers’ willingness to pay. The price signals the relative value of that commodity compared<br />

to other goods and services. How much a firm is willing and able to produce at a given price is<br />

determined by many things, including how much it must pay for the labor it hires, the land and<br />

resources it uses, the capital it employs, the material inputs it must purchase, the transportation it<br />

must use, and the risks associated with its investment. Consumers’ overall willingness to pay for<br />

a product also is determined by a large variety of factors, such as the existence and prices of<br />

substitutes, income, and individual needs and tastes.<br />

<strong>Price</strong> changes generally reflect changes in producer costs or consumer demand. Simply<br />

put, prices rise if it costs more to produce and supply a good, or if people desire to buy more of<br />

that good at the current price. <strong>Price</strong>s fall if it costs less to produce and supply a good, or if<br />

people desire to buy less of that good at the current price. When changes in producer costs or<br />

CHAPTER 1: SUPPLY, DEMAND, AND COMPETITION 7<br />

8/26/2003<br />

9/2/2003<br />

9/9/2003<br />

9/16/2003<br />

9/23/2003<br />

9/30/2003