English version - Hexagon Composites ASA

English version - Hexagon Composites ASA

English version - Hexagon Composites ASA

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

COMROD COMMUNICATION <strong>ASA</strong> – LISTING ON THE OSLO STOCK EXCHANGE<br />

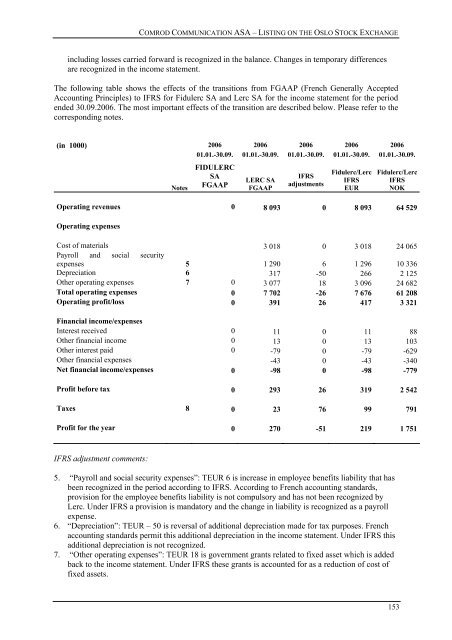

including losses carried forward is recognized in the balance. Changes in temporary differences<br />

are recognized in the income statement.<br />

The following table shows the effects of the transitions from FGAAP (French Generally Accepted<br />

Accounting Principles) to IFRS for Fidulerc SA and Lerc SA for the income statement for the period<br />

ended 30.09.2006. The most important effects of the transition are described below. Please refer to the<br />

corresponding notes.<br />

(in 1000)<br />

2006 2006 2006 2006 2006<br />

01.01.-30.09. 01.01.-30.09. 01.01.-30.09. 01.01.-30.09. 01.01.-30.09.<br />

Notes<br />

FIDULERC<br />

SA<br />

FGAAP<br />

LERC SA<br />

FGAAP<br />

IFRS<br />

adjustments<br />

Fidulerc/Lerc<br />

IFRS<br />

EUR<br />

Fidulerc/Lerc<br />

IFRS<br />

NOK<br />

Operating revenues 0 8 093 0 8 093 64 529<br />

Operating expenses<br />

Cost of materials 3 018 0 3 018 24 065<br />

Payroll and social security<br />

expenses 5 1 290 6 1 296 10 336<br />

Depreciation 6 317 -50 266 2 125<br />

Other operating expenses 7 0 3 077 18 3 096 24 682<br />

Total operating expenses 0 7 702 -26 7 676 61 208<br />

Operating profit/loss 0 391 26 417 3 321<br />

Financial income/expenses<br />

Interest received 0 11 0 11 88<br />

Other financial income 0 13 0 13 103<br />

Other interest paid 0 -79 0 -79 -629<br />

Other financial expenses -43 0 -43 -340<br />

Net financial income/expenses 0 -98 0 -98 -779<br />

Profit before tax 0 293 26 319 2 542<br />

Taxes 8 0 23 76 99 791<br />

Profit for the year 0 270 -51 219 1 751<br />

IFRS adjustment comments:<br />

5. “Payroll and social security expenses”: TEUR 6 is increase in employee benefits liability that has<br />

been recognized in the period according to IFRS. According to French accounting standards,<br />

provision for the employee benefits liability is not compulsory and has not been recognized by<br />

Lerc. Under IFRS a provision is mandatory and the change in liability is recognized as a payroll<br />

expense.<br />

6. “Depreciation”: TEUR – 50 is reversal of additional depreciation made for tax purposes. French<br />

accounting standards permit this additional depreciation in the income statement. Under IFRS this<br />

additional depreciation is not recognized.<br />

7. “Other operating expenses”: TEUR 18 is government grants related to fixed asset which is added<br />

back to the income statement. Under IFRS these grants is accounted for as a reduction of cost of<br />

fixed assets.<br />

153