Untitled - the ultimate blog

Untitled - the ultimate blog

Untitled - the ultimate blog

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

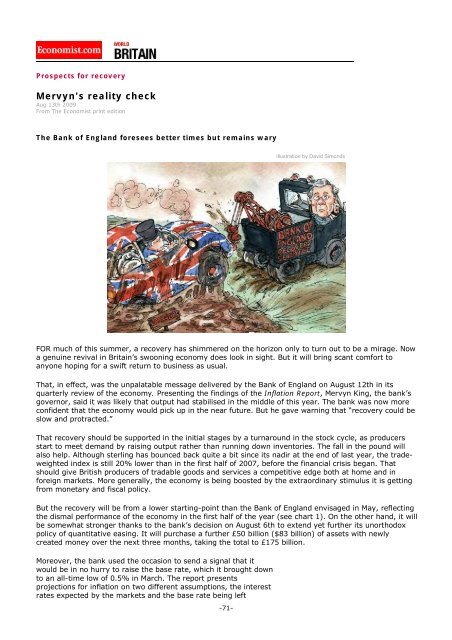

Prospects for recovery<br />

Mervyn's reality check<br />

Aug 13th 2009<br />

From The Economist print edition<br />

The Bank of England foresees better times but remains wary<br />

Illustration by David Simonds<br />

FOR much of this summer, a recovery has shimmered on <strong>the</strong> horizon only to turn out to be a mirage. Now<br />

a genuine revival in Britain’s swooning economy does look in sight. But it will bring scant comfort to<br />

anyone hoping for a swift return to business as usual.<br />

That, in effect, was <strong>the</strong> unpalatable message delivered by <strong>the</strong> Bank of England on August 12th in its<br />

quarterly review of <strong>the</strong> economy. Presenting <strong>the</strong> findings of <strong>the</strong> Inflation Report, Mervyn King, <strong>the</strong> bank’s<br />

governor, said it was likely that output had stabilised in <strong>the</strong> middle of this year. The bank was now more<br />

confident that <strong>the</strong> economy would pick up in <strong>the</strong> near future. But he gave warning that “recovery could be<br />

slow and protracted.”<br />

That recovery should be supported in <strong>the</strong> initial stages by a turnaround in <strong>the</strong> stock cycle, as producers<br />

start to meet demand by raising output ra<strong>the</strong>r than running down inventories. The fall in <strong>the</strong> pound will<br />

also help. Although sterling has bounced back quite a bit since its nadir at <strong>the</strong> end of last year, <strong>the</strong> tradeweighted<br />

index is still 20% lower than in <strong>the</strong> first half of 2007, before <strong>the</strong> financial crisis began. That<br />

should give British producers of tradable goods and services a competitive edge both at home and in<br />

foreign markets. More generally, <strong>the</strong> economy is being boosted by <strong>the</strong> extraordinary stimulus it is getting<br />

from monetary and fiscal policy.<br />

But <strong>the</strong> recovery will be from a lower starting-point than <strong>the</strong> Bank of England envisaged in May, reflecting<br />

<strong>the</strong> dismal performance of <strong>the</strong> economy in <strong>the</strong> first half of <strong>the</strong> year (see chart 1). On <strong>the</strong> o<strong>the</strong>r hand, it will<br />

be somewhat stronger thanks to <strong>the</strong> bank’s decision on August 6th to extend yet fur<strong>the</strong>r its unorthodox<br />

policy of quantitative easing. It will purchase a fur<strong>the</strong>r £50 billion ($83 billion) of assets with newly<br />

created money over <strong>the</strong> next three months, taking <strong>the</strong> total to £175 billion.<br />

Moreover, <strong>the</strong> bank used <strong>the</strong> occasion to send a signal that it<br />

would be in no hurry to raise <strong>the</strong> base rate, which it brought down<br />

to an all-time low of 0.5% in March. The report presents<br />

projections for inflation on two different assumptions, <strong>the</strong> interest<br />

rates expected by <strong>the</strong> markets and <strong>the</strong> base rate being left<br />

-71-

![[ccebbook.cn]The Economist August 1st 2009 - the ultimate blog](https://img.yumpu.com/28183607/1/190x252/ccebbookcnthe-economist-august-1st-2009-the-ultimate-blog.jpg?quality=85)

![[ccebook.cn]The World in 2010](https://img.yumpu.com/12057568/1/190x249/ccebookcnthe-world-in-2010.jpg?quality=85)

![[ccemagz.com]The Economist October 24th 2009 - the ultimate blog](https://img.yumpu.com/5191885/1/190x252/ccemagzcomthe-economist-october-24th-2009-the-ultimate-blog.jpg?quality=85)