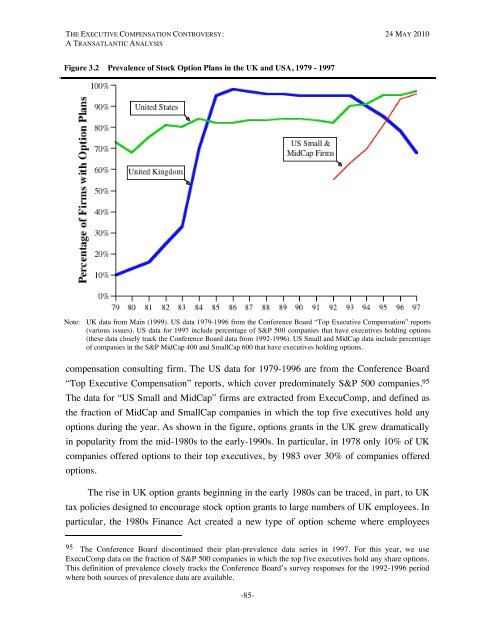

THE EXECUTIVE COMPENSATION CONTROVERSY: 24 MAY 2010A TRANSATLANTIC ANALYSISFigure 3.2 Prevalence of Stock Option Plans in the UK and USA, 1979 - 1997Note: UK data from Main (1999). US data 1979-1996 from the Conference Board “Top <strong>Executive</strong> <strong>Compensation</strong>” reports(various issues). US data for 1997 include percentage of S&P 500 companies that have executives holding options(these data closely track the Conference Board data from 1992-1996). US Small and MidCap data include percentageof companies in the S&P MidCap 400 and SmallCap 600 that have executives holding options.compensation consulting firm. <strong>The</strong> US data for 1979-1996 are from the Conference Board“Top <strong>Executive</strong> <strong>Compensation</strong>” reports, which cover predominately S&P 500 companies. 95<strong>The</strong> data for “US Small and MidCap” firms are extracted from ExecuComp, and defined asthe fraction of MidCap and SmallCap companies in which the top five executives hold anyoptions during the year. As shown in the figure, options grants in the UK grew dramaticallyin popularity from the mid-1980s to the early-1990s. In particular, in 1978 only 10% of UKcompanies offered options to their top executives, by 1983 over 30% of companies offeredoptions.<strong>The</strong> rise in UK option grants beginning in the early 1980s can be traced, in part, to UKtax policies designed to encourage stock option grants to large numbers of UK employees. Inparticular, the 1980s Finance Act created a new type of option scheme where employees95 <strong>The</strong> Conference Board discontinued their plan-prevalence data series in 1997. For this year, we useExecuComp data on the fraction of S&P 500 companies in which the top five executives hold any share options.This definition of prevalence closely tracks the Conference Board’s survey responses for the 1992-1996 periodwhere both sources of prevalence data are available.-85-

THE EXECUTIVE COMPENSATION CONTROVERSY: 24 MAY 2010A TRANSATLANTIC ANALYSISinvesting their savings in company stock options could escape all taxes upon exercise,provided that they held the option for a sufficient period of time. 96 <strong>The</strong> new options had aterm of either five or seven years, and would be granted at a fixed exercise price no less than90% of the grant-date market price. In 1983, the government created a second type of taxfavoredoption plan, called the “Save As You Earn (SAYE) Share Option Issue Series B.” 97In 1984, the government doubled the monthly limit on savings under the plan (from £50 to£100). In April 1984, in a move reminiscent of the US policies in 1950, the UK governmentextended benefits to top executives receiving options, by designating gains upon exercisingoptions as “capital gains” taxable only when the shares were ultimately sold rather than asordinary income taxable upon exercise. 98In 1979, only three UK firms offered options to all employees. By 1982 more than 200companies were offering such plans, and by 1984 nearly 700 companies offered broad-basedgovernment-approved (and encouraged) option plans. 99 As shown in Figure 3.2, by 1986 –following the new tax treatment for options granted to top executives – nearly all UKcompanies offered option plans to its executives (and often to all employees). Indeed, asshown in the figure, from 1985 to 1993 the prevalence of options in the UK surpassed theprevalence in the USA.As discussed in Section 3.1, stock options became controversial in the UK in the early1990s after executives in water, gas, and electric utilities began reporting gains on optionsgranted when the utilities were privatized in 1990. <strong>The</strong> exercise prices had been set at thegovernment’s assumption of a market price, which turned out to be much lower than theactual price the shares would sell for on the open market. As a result, the executives realizedlarge option gains even as their companies underperformed their industry. <strong>The</strong> outrage overthese option schemes led to the influential report by the Greenbury (1995) committee, whichcalled for a comprehensive review (with potential retroactive changes) of all option plans atexisting privatized utilities, and a moratorium on granting options at newly privatized utilitiesuntil six months after the shares are traded on open exchanges. More broadly, the Greenbury96 See Anthony, “Changes to encourage share-holding,” Guardian (May 17, 1980), p. 20; Moullin, “Betterschemes now for profit-sharing,” Guardian (August 16, 1980), p. 18; Davis, “Cheap Shares,” Observer(October 24, 1982), p. 23.97 Dibben, “Opening up the options,” Guardian (November 19, 1983), p. 23.98 “Share Options: Employees shares fillip,” Guardian (March 14, 1984), p. 3.99 Davis, “Cheap Shares,” Observer (October 24, 1982), p. 23; “Share Options: Employees shares fillip,”Guardian (March 14, 1984), p. 3.-86-