Michelin couv courteGB

Michelin couv courteGB

Michelin couv courteGB

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

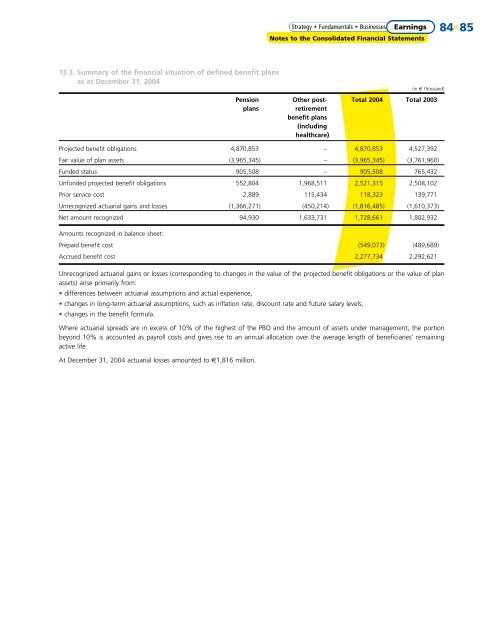

13.3. Summary of the financial situation of defined benefit plans<br />

as at December 31, 2004<br />

Strategy • Fundamentals • Businesses • Résultats Earnings<br />

Notes to the Consolidated Financial Statements<br />

(in € thousand)<br />

Pension Other post- Total 2004 Total 2003<br />

plans retirement<br />

benefit plans<br />

(including<br />

healthcare)<br />

Projected benefit obligations 4,870,853 – 4,870,853 4,527,392<br />

Fair value of plan assets (3,965,345) – (3,965,345) (3,761,960)<br />

Funded status 905,508 – 905,508 765,432<br />

Unfunded projected benefit obligations 552,804 1,968,511 2,521,315 2,508,102<br />

Prior service cost 2,889 115,434 118,323 139,771<br />

Unrecognized actuarial gains and losses (1,366,271) (450,214) (1,816,485) (1,610,373)<br />

Net amount recognized 94,930 1,633,731 1,728,661 1,802,932<br />

Amounts recognized in balance sheet:<br />

Prepaid benefit cost (549,073) (489,689)<br />

Accrued benefit cost 2,277,734 2,292,621<br />

Unrecognized actuarial gains or losses (corresponding to changes in the value of the projected benefit obligations or the value of plan<br />

assets) arise primarily from:<br />

• differences between actuarial assumptions and actual experience,<br />

• changes in long-term actuarial assumptions, such as inflation rate, discount rate and future salary levels,<br />

• changes in the benefit formula.<br />

Where actuarial spreads are in excess of 10% of the highest of the PBO and the amount of assets under management, the portion<br />

beyond 10% is accounted as payroll costs and gives rise to an annual allocation over the average length of beneficiaries’ remaining<br />

active life.<br />

At December 31, 2004 actuarial losses amounted to €1,816 million.<br />

84•85