Annual Report 2010 - Verein der Kohlenimporteure eV

Annual Report 2010 - Verein der Kohlenimporteure eV

Annual Report 2010 - Verein der Kohlenimporteure eV

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

78<br />

To a lesser extent, plans are being made to expand<br />

production capacities in the coking coal sector. At<br />

the Makhado coking coal project in the Limpopo<br />

<br />

of resources, of which 230 million tonnes have been<br />

proven, will be opened. According to plans, coking coal<br />

production will begin in 2013 and then increase to a full<br />

capacity of 5 million tonnes per annum.<br />

The Rietkuil project in the Mpumalanga region was<br />

granted production rights. The aim is to produce about<br />

3 Mt of coal annually for 30 years.<br />

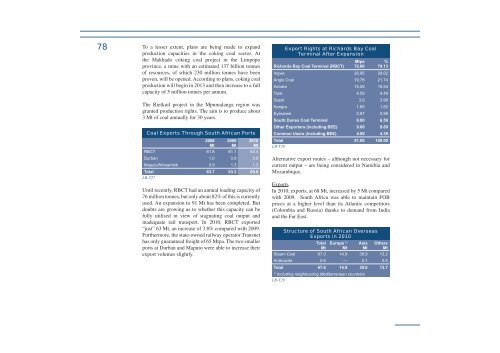

Coal Exports Through South African Ports<br />

2008<br />

Mt<br />

2009<br />

Mt<br />

<strong>2010</strong><br />

Mt<br />

RBCT 61.8 61.1 63.4<br />

Durban 1.0 0.9 0.9<br />

Maputo/Mosambik 0.9 1.3 1.3<br />

Total<br />

LB-T27<br />

63.7 63.3 65.6<br />

Until recently, RBCT had an annual loading capacity of<br />

<br />

used. An expansion to 91 Mt has been completed. But<br />

doubts are growing as to whether this capacity can be<br />

fully utilised in view of stagnating coal output and<br />

inadequate rail transport. In <strong>2010</strong>, RBCT exported<br />

“just” 63 Mt, an increase of 3.8% compared with 2009.<br />

<br />

has only guaranteed freight of 65 Mtpa. The two smaller<br />

ports at Durban and Maputo were able to increase their<br />

export volumes slightly.<br />

Export Rights at Richards Bay Coal<br />

Terminal After Expansion<br />

Mtpa %<br />

Richards Bay Coal Terminal (RBCT) 72.00 79.13<br />

Ingwe 26.95 29.62<br />

Anglo Coal 19.78 21.74<br />

Xstrata 15.06 16.54<br />

Total 4.09 4.49<br />

Sasol 3.6 3.96<br />

Kangra 1.65 1.82<br />

Eyesizwe 0.87 0.96<br />

South Dunes Coal Terminal 6.00 6.59<br />

Other Exporters (including BEE) 9.00 9.89<br />

Common Users (including BEE) 4.00 4.39<br />

Total<br />

LB-T28<br />

91.00 100.00<br />

Alternative export routes – although not necessary for<br />

current output – are being consi<strong>der</strong>ed in Namibia and<br />

Mozambique.<br />

Exports<br />

In <strong>2010</strong>, exports, at 68 Mt, increased by 5 Mt compared<br />

<br />

prices at a higher level than its Atlantic competitors<br />

(Colombia and Russia) thanks to demand from India<br />

<br />

Structure of South African Overseas<br />

Exports in <strong>2010</strong><br />

Total<br />

Mt<br />

Europe 1)<br />

Mt<br />

Asia<br />

Mt<br />

Others<br />

Mt<br />

Steam Coal 67.0 14.9 38.9 13.2<br />

Anthracite 0.6 --- 0.1 0.5<br />

Total 67.6 14.9 39.0 13.7<br />

1) <br />

LB-T29