- Page 1 and 2:

A Report to the Minister for Health

- Page 3 and 4:

CONTENTS TABLE OF FIGURES _________

- Page 5 and 6:

CONSUMER ATTITUDES TO SWITCHING ___

- Page 7 and 8:

EXECUTIVE SUMMARY AND RECOMMENDATIO

- Page 9 and 10:

As a result it does not have to sat

- Page 11 and 12:

Recommendation 7 The Minister for H

- Page 13 and 14:

indicates that consumers of PHI hav

- Page 15 and 16:

Recommendation 13 The Minister for

- Page 17 and 18:

is quite unclear, so far as the Aut

- Page 19 and 20:

1.4 For the next number of months t

- Page 21 and 22:

other insurers were to enter the ma

- Page 23 and 24:

2.6 Private health insurance (PHI)

- Page 25 and 26:

2.17 Open enrolment and lifetime co

- Page 27 and 28:

• 2001: The Health Insurance Auth

- Page 29 and 30:

Figure 2: Annual Change in PHI memb

- Page 31 and 32:

of medical inflation and the higher

- Page 33 and 34:

VIVAS Health is rising steadily. In

- Page 35 and 36:

• Table 1 below shows the annual

- Page 37 and 38:

Figure 6: PHI Products BUPA Ireland

- Page 39 and 40:

• Work-based group schemes where

- Page 41 and 42:

from year to year and also during t

- Page 43 and 44:

3. DEFINING THE PRIVATE HEALTH INSU

- Page 45 and 46:

Figure 7: Key features of Related H

- Page 47 and 48:

price increase unprofitable by a hy

- Page 49 and 50:

4.6 Aspects of the exemption from i

- Page 51 and 52:

and quarterly management accounts t

- Page 53 and 54:

Table 4: Regulation of PHI Firms 48

- Page 55 and 56:

4.31 This is a positive step. Just

- Page 57 and 58:

obliges Vhi Healthcare to seek appr

- Page 59 and 60:

4.41 In the regulatory approval pro

- Page 61 and 62:

4.50 However, the Authority is clea

- Page 63 and 64:

Unfunded Lifetime Community Rating

- Page 65 and 66:

President of the Society of Actuari

- Page 67 and 68:

− The main other deterrent at pre

- Page 69 and 70:

o The former members of the Advisor

- Page 71 and 72:

materially affected by any seasonal

- Page 73 and 74:

It may also be noted that the propo

- Page 75 and 76:

4.94 There are 37 health insurers i

- Page 77 and 78:

Interviews with Possible New Entran

- Page 79 and 80:

have shown that new sales and switc

- Page 81 and 82:

not binding on incumbents and no in

- Page 83 and 84:

5.33 In this context Vhi Healthcare

- Page 85 and 86:

5.44 As the former incumbent monopo

- Page 87 and 88:

5.52 Vhi Healthcare’s first mover

- Page 89 and 90:

• Psychological costs 6.5 Transac

- Page 91 and 92:

18-24 9% 13% 25-34 34% 19% 35-44 31

- Page 93 and 94:

6.24 The provision of renewal notic

- Page 95 and 96:

The HIA publishes on its website a

- Page 97 and 98:

Recommendation 10 Following consult

- Page 99 and 100:

Recommendation 11 The insurance com

- Page 101 and 102: Regulations were established to aff

- Page 103 and 104: transferred and the amounts require

- Page 105 and 106: Buyer Power and Concentrated Market

- Page 107 and 108: The Supply of Private Medical Facil

- Page 109 and 110: VIVAS Health claims that Vhi Health

- Page 111 and 112: approval on coverage of facilities

- Page 113 and 114: Supplier-Induced Demand 7.36 The Vh

- Page 115 and 116: Questions Relevant evidence Irish P

- Page 117 and 118: to restrict individual choice of pr

- Page 119 and 120: 8. CONCENTRATION AND MARKET POWER I

- Page 121 and 122: gives us some indication of the com

- Page 123 and 124: wishes to retain the flexibility to

- Page 125 and 126: largest price increase that is prof

- Page 127 and 128: scheme. Employees may be under the

- Page 129 and 130: elevant regulatory requirements, ex

- Page 131 and 132: Table 7 Vhi Healthcare Financial Re

- Page 133 and 134: • There is limited buyer power fr

- Page 135 and 136: Breaking up Vhi Healthcare would di

- Page 137 and 138: expertise and other staff resources

- Page 139 and 140: APPENDIX 1 Other forms of health re

- Page 141 and 142: APPENDIX 2 Report of UK Government

- Page 143 and 144: Australia Ireland Public hospital U

- Page 145 and 146: Australia Ireland Risk equalisation

- Page 147 and 148: 1.22 The Irish data is not split at

- Page 149 and 150: Conclusion of normal claim payments

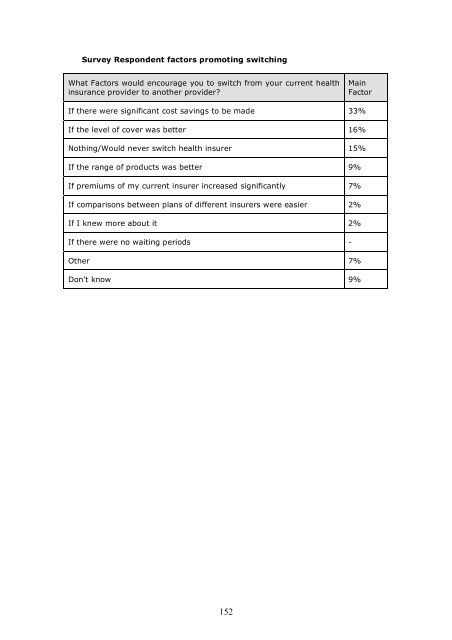

- Page 151: APPENDIX 3 Consumer Attitudes to Sw

- Page 155 and 156: APPENDIX 5 OECD Review of PHI The O

- Page 157 and 158: not-for-profit insurers has posed c

- Page 159 and 160: 114. Private insurers have not impl

- Page 161 and 162: APPENDIX 6 List of Submissions The

- Page 163 and 164: Understanding and Comparing Private

- Page 165 and 166: Benefits Outpatient Cover Cover for

- Page 167 and 168: Dobson, P., M. Waterson and A. Chu,

- Page 169: Vhi Healthcare (2005), Annual Repor