MARKETRental and property marketGood rate of growth continues despite slowdownSweden is now part of a global property market and is thusaffected by the slowdown in the rate of growth that isexpected in the years to come.General market conditionsThe global economy is expected to continue to grow at a reduced rateover the next few years. Financial unrest in the USA can be expectedto continue into 2008 with the risk of a major downturn in the Americaneconomy as a result. This will have repercussions in the Swedisheconomy towards the end of 2008 and into 2009.Sweden is currently in a period of strong economic growth andincreased employment. Expansion is being fuelled by rising exportsand private consumption as well as a growing rate of investment.Improved incomes, tax reductions and changes in the social insurancesystems have together resulted in a continued strong economicclimate and increased employment. At the same time, there is a tendencytowards overheating and rising inflation and to counteract thisthe Swedish Riksbank has raised the repo rate. Growth in Sweden isexpected to weaken slightly in the immediate future. A slowdown in therate of investment will probably be the main reason for the lower rate ofgrowth in Sweden over the next few years.Regional markets in SwedenThere is a clear link between the size of a region in terms of populationand the rate of growth. A large market offers economies of scale andattracts people and capital. The creation of growth throughout thecountry requires strategies based on local conditions and the mobilisationof development potential in the various regions throughout thecountry.Growth requires regional expansion and if the region is smallgreater specialisation is needed to meet demand from other markets.Regional expansion takes place by making commuting easier. Thepotential to commute, the economy of the regions and long-termgrowth are important parameters for players on the property marketalongside identifying the segments on the property market to monitorthat have the best potential in the region chosen. The fact, for example,that small inland regions have acquired better conditions for growth isborne out in the growth table produced by the business magazineAffärsvärlden. Sweden’s most rapidly growing regions at the momentare Haparanda, Pajala and Kiruna. Malmö, Stockholm, Luleå, Blekingeand Gothenburg are also among the 20 most rapidly growingregions. However, the smaller regions do not have any major impacton overall growth in the country. It is in the larger regions that themajority of the growth is created. The three large city regions accountfor over half the national growth.The property marketToday Sweden is part of a global property market. In over half of all theproperty transactions in Sweden the purchasers were foreign investors.During 2006, Sweden was the fourth largest investor market in Europewith six per cent of the invested capital. The transparent Swedish marketis appreciated by foreign investors. Public registers offer goodaccess to information, which facilitates the purchase process.After a very high transaction volume in Europe during the first twoquarters of 2007, which was also reflected in Sweden, turnover fell.Reduced liquidity through poorer financing opportunities andincreased cost of capital, coupled with a lower propensity to take risks,are expected to ensue from the global financial unrest. The opinion is,however, that access to capital to purchase properties will continue tobe good in the long term. In Sweden, prices for prime location premisesare expected to stabilise. For other properties, a certain weakeningis expected as interest rates rise and the willingness to take risksfalls. The yield requirements have now stagnated although for certaintypes of property categories they have shown signs of rising again.The rental market in SwedenHigher employment and a continued strong belief in the future are thedriving forces behind the demand on the rental market for offices. Anincreased level of activity and a need to recruit within office-based sectorssuch as insurance companies and recruitment and employmentagencies are leading to an increase in demand for office premises. Theavailability of modern, centrally located offices is no longer sufficient tomeet the demand at all locations. Over the next year the fall in the levelof vacant space is expected to continue and at the same time rents areexpected to rise. Generally, it is the newly constructed, centrallylocated, space-efficient premises where the greatest rental growthcan be expected. Image-creating premises with the potential for customerprofiling are also in demand. Household purchasing powerincreased substantially during 2007. The increase in consumption isalso leading to a rise in rents for stores in areas that attract a largenumber of shoppers.From 2008, a slight downturn in the economy is expected with acertain weakening in Sweden. This, in combination with a number ofcommercial properties being released onto the market, could contributeto a generally slower rise in rents for the coming years.The construction marketAn increase in the shortage of labour in combination with hastily abolishedsubsidies are expected to hold back the rate of growth on theconstruction market. With rising construction prices and constructionstarts being postponed, building of residential property could fall. Theconstruction market is also continuing to experience problemsaccessing building materials. Rising prices, market dominance andcontrols are also future concerns that must be resolved in order tofacilitate construction.During the first half of 2007, the number of apartments commencedfell by 29 per cent compared with the same period in2006. Because many developers attempted to bring forward constructionstarts before the end of 2006 in order to obtain subsidiesthe commencement of residential construction in 2007 is expectedto be lower than what would otherwise have been the case. On theother hand, the number of completed housing projects increasedby 26 per cent during the same period. <strong>Akademiska</strong> <strong>Hus</strong> <strong>Annual</strong> <strong>Report</strong> 2007 | Rental and property market

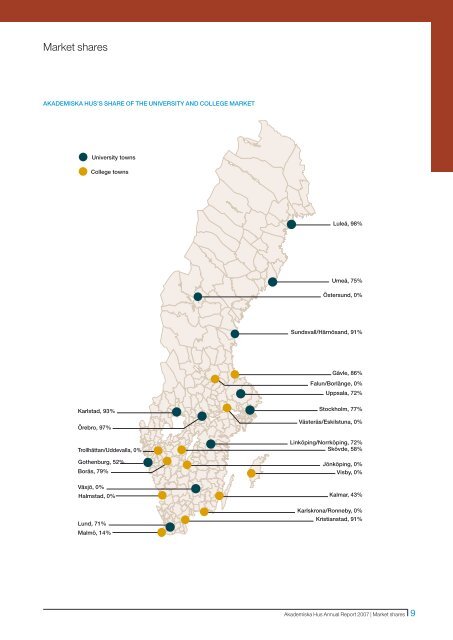

Market sharesAKADEMISKA HUS’S SHARE OF THE UNIVERSITY AND COLLEGE MARKETUniversity townsCollege townsLuleå, 98%Umeå, 75%Östersund, 0%Sundsvall/Härnösand, 91%Gävle, 86%Falun/Borlänge, 0%Uppsala, 72%Karlstad, 93%Örebro, 97%Stockholm, 77%Västerås/Eskilstuna, 0%Linköping/Norrköping, 72%Trollhättan/Uddevalla, 0% Skövde, 58%Gothenburg, 52%Borås, 79%Växjö, 0%Halmstad, 0%Lund, 71%Malmö, 14%Jönköping, 0%Visby, 0%Kalmar, 43%Karlskrona/Ronneby, 0%Kristianstad, 91%<strong>Akademiska</strong> <strong>Hus</strong> <strong>Annual</strong> <strong>Report</strong> 2007 | Market shares

- Page 6 and 7: Review of the yearAkademiska Hus 20

- Page 8 and 9: Statement by the PresidentIncreased

- Page 10 and 11: Business concept, visions and objec

- Page 14 and 15: MARKETAkademiska Hus marketHigher e

- Page 16 and 17: MARKETResearch Bill 2008In internat

- Page 18 and 19: MARKETCompetitorsLocal players the

- Page 20 and 21: MARKETProperty specification, North

- Page 23 and 24: 1613 6 24 2912171142962122932464751

- Page 25 and 26: EASTERN REGION (ÖST)Major efforts

- Page 27 and 28: ((KYRKBYNE6E20GOTHENBURGSA-FÄRJEST

- Page 29 and 30: LLUNDPLANTAGELYCKANHELGONAGÅRDEN3S

- Page 31 and 32: At the Ingvar Kamprad Design Centre

- Page 33 and 34: could benefit from proximity to the

- Page 35 and 36: of energy system and form of energy

- Page 37 and 38: difficult to influence. In the Ultu

- Page 40 and 41: OPERATIONSProperty valuationSlight

- Page 42: OPERATIONSlation of the rental paym

- Page 45 and 46: Operating costsOperating costs, a s

- Page 47 and 48: Maintenance costsStable maintenance

- Page 49 and 50: Comments on the Five-year summary1.

- Page 51 and 52: Regions and GroupKey figuresKey fig

- Page 53 and 54: Average rentable floor space, regio

- Page 55 and 56: Interest-bearing net loan debt, inc

- Page 57 and 58: Construction projectsNew constructi

- Page 59 and 60: By drawing up good documents for co

- Page 61 and 62: Akademiska Hus - a partner in the d

- Page 63 and 64:

SustainabilityAkademiska Hus’s am

- Page 65 and 66:

Akademiska Hus is working to ensure

- Page 67 and 68:

EmployeesInvestment in employee dev

- Page 69 and 70:

Group level, on the regional level

- Page 71 and 72:

Group corporate governance reportTh

- Page 73 and 74:

Remuneration and other terms and co

- Page 75 and 76:

Board and auditorsBOARDEva-Britt Gu

- Page 77 and 78:

Financial Report 73-10473Swedish Na

- Page 79 and 80:

Income StatementsGroupIFRSParent Co

- Page 81 and 82:

Balance SheetsGroupIFRSParent Compa

- Page 83 and 84:

Cash Flow StatementsGroupIFRSParent

- Page 85 and 86:

Note 3, cont’d .comprises rental

- Page 87 and 88:

Note 3, cont’d .fair value. Chang

- Page 89 and 90:

6 Categorised operating costsFuncti

- Page 91 and 92:

Note 13, cont’d .Payments to the

- Page 93 and 94:

Note 17, cont’d.17 TaxesThe follo

- Page 95 and 96:

Cost of capital and direct yield re

- Page 97 and 98:

Note 24, cont’d.The table below s

- Page 99 and 100:

Note 32, cont’d.Borrowing can be

- Page 101 and 102:

Note 33, cont’d.The retirement pe

- Page 103 and 104:

Note 37, cont’d.Due date structur

- Page 105 and 106:

39 Pledged assetsGroupIFRSParent Co

- Page 107 and 108:

Audit ReportTo the annual meeting o

- Page 109 and 110:

AddressesGROUP HEAD OFFICEAkademisk