Monthly Bulletin April 2008 - European Central Bank - Europa

Monthly Bulletin April 2008 - European Central Bank - Europa

Monthly Bulletin April 2008 - European Central Bank - Europa

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

February, after having increased by an average<br />

monthly rate of 1.4% over the period from<br />

May 2007 to January <strong>2008</strong>. Despite this<br />

moderation in short-term movements, past<br />

developments still imply significant accumulated<br />

pipeline pressures which have not yet reached<br />

the consumer level. In particular, these pressures<br />

could have a further impact on the consumer<br />

prices charged by food-related service providers.<br />

By contrast, the annual rate of change in producer<br />

prices for consumer goods excluding tobacco and<br />

food prices continued in February to move around<br />

the moderate level observed since the beginning<br />

of last year. Thus there is so far no evidence of an<br />

increase in pipeline pressures on consumer prices<br />

for non-energy industrial goods.<br />

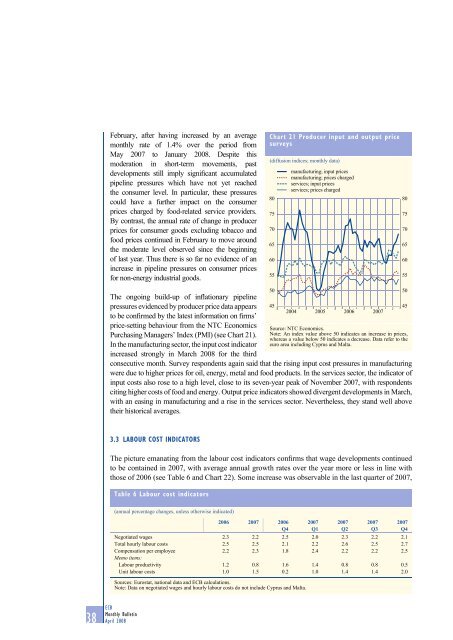

Chart 21 Producer input and output price<br />

surveys<br />

(diffusion indices; monthly data)<br />

80<br />

75<br />

70<br />

65<br />

60<br />

55<br />

manufacturing; input prices<br />

manufacturing; prices charged<br />

services; input prices<br />

services; prices charged<br />

80<br />

75<br />

70<br />

65<br />

60<br />

55<br />

The ongoing build-up of inflationary pipeline<br />

pressures evidenced by producer price data appears<br />

to be confirmed by the latest information on firms’<br />

price-setting behaviour from the NTC Economics<br />

Purchasing Managers’ Index (PMI) (see Chart 21).<br />

In the manufacturing sector, the input cost indicator<br />

increased strongly in March <strong>2008</strong> for the third<br />

consecutive month. Survey respondents again said that the rising input cost pressures in manufacturing<br />

were due to higher prices for oil, energy, metal and food products. In the services sector, the indicator of<br />

input costs also rose to a high level, close to its seven-year peak of November 2007, with respondents<br />

citing higher costs of food and energy. Output price indicators showed divergent developments in March,<br />

with an easing in manufacturing and a rise in the services sector. Nevertheless, they stand well above<br />

their historical averages.<br />

50<br />

45<br />

2004 2005 2006 2007<br />

Source: NTC Economics.<br />

Note: An index value above 50 indicates an increase in prices,<br />

whereas a value below 50 indicates a decrease. Data refer to the<br />

euro area including Cyprus and Malta.<br />

50<br />

45<br />

3.3 LABOUR COST INDICATORS<br />

The picture emanating from the labour cost indicators confirms that wage developments continued<br />

to be contained in 2007, with average annual growth rates over the year more or less in line with<br />

those of 2006 (see Table 6 and Chart 22). Some increase was observable in the last quarter of 2007,<br />

Table 6 Labour cost indicators<br />

(annual percentage changes, unless otherwise indicated)<br />

2006 2007 2006<br />

Q4<br />

Negotiated wages 2.3 2.2 2.5 2.0 2.3 2.2 2.1<br />

Total hourly labour costs 2.5 2.5 2.1 2.2 2.6 2.5 2.7<br />

Compensation per employee 2.2 2.3 1.8 2.4 2.2 2.2 2.5<br />

Memo items:<br />

Labour productivity 1.2 0.8 1.6 1.4 0.8 0.8 0.5<br />

Unit labour costs 1.0 1.5 0.2 1.0 1.4 1.4 2.0<br />

Sources: Eurostat, national data and ECB calculations.<br />

Note: Data on negotiated wages and hourly labour costs do not include Cyprus and Malta.<br />

2007<br />

Q1<br />

2007<br />

Q2<br />

2007<br />

Q3<br />

2007<br />

Q4<br />

38 ECB<br />

<strong>Monthly</strong> <strong>Bulletin</strong><br />

<strong>April</strong> <strong>2008</strong>