Setting new standards - Friends Life

Setting new standards - Friends Life

Setting new standards - Friends Life

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

INTERNATIONAL LIFE & PENSIONS ASSET MANAGEMENT GROUP FINANCIAL PERFORMANCE CONCLUSIONS AND OUTLOOK<br />

Our financial performance<br />

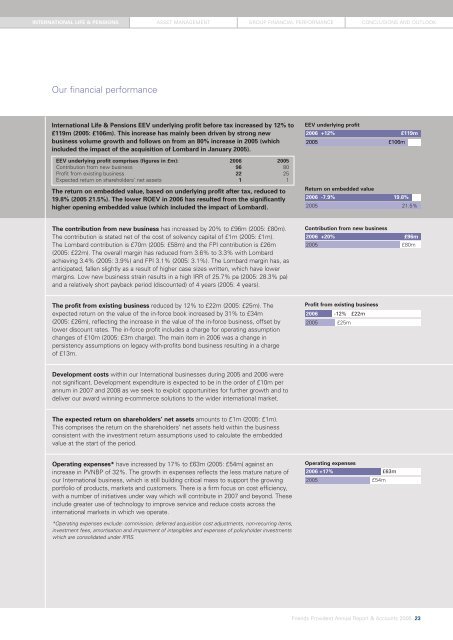

International <strong>Life</strong> & Pensions EEV underlying profit before tax increased by 12% to<br />

£119m (2005: £106m). This increase has mainly been driven by strong <strong>new</strong><br />

business volume growth and follows on from an 80% increase in 2005 (which<br />

included the impact of the acquisition of Lombard in January 2005).<br />

EEV underlying profit comprises (figures in £m): 2006 2005<br />

Contribution from <strong>new</strong> business 96 80<br />

Profit from existing business 22 25<br />

Expected return on shareholders’ net assets 1 1<br />

The return on embedded value, based on underlying profit after tax, reduced to<br />

19.8% (2005 21.5%). The lower ROEV in 2006 has resulted from the significantly<br />

higher opening embedded value (which included the impact of Lombard).<br />

EEV underlying profit<br />

2006 +12% £119m<br />

2005 £106m<br />

Return on embedded value<br />

2006 -7.9% 19.8%<br />

2005 21.5%<br />

The contribution from <strong>new</strong> business has increased by 20% to £96m (2005: £80m).<br />

The contribution is stated net of the cost of solvency capital of £1m (2005: £1m).<br />

The Lombard contribution is £70m (2005: £58m) and the FPI contribution is £26m<br />

(2005: £22m). The overall margin has reduced from 3.6% to 3.3% with Lombard<br />

achieving 3.4% (2005: 3.9%) and FPI 3.1% (2005: 3.1%). The Lombard margin has, as<br />

anticipated, fallen slightly as a result of higher case sizes written, which have lower<br />

margins. Low <strong>new</strong> business strain results in a high IRR of 25.7% pa (2005: 28.3% pa)<br />

and a relatively short payback period (discounted) of 4 years (2005: 4 years).<br />

Contribution from <strong>new</strong> business<br />

2006 +20% £96m<br />

2005 £80m<br />

The profit from existing business reduced by 12% to £22m (2005: £25m). The<br />

expected return on the value of the in-force book increased by 31% to £34m<br />

(2005: £26m), reflecting the increase in the value of the in-force business, offset by<br />

lower discount rates. The in-force profit includes a charge for operating assumption<br />

changes of £10m (2005: £3m charge). The main item in 2006 was a change in<br />

persistency assumptions on legacy with-profits bond business resulting in a charge<br />

of £13m.<br />

Profit from existing business<br />

2006 -12% £22m<br />

2005 £25m<br />

Development costs within our International businesses during 2005 and 2006 were<br />

not significant. Development expenditure is expected to be in the order of £10m per<br />

annum in 2007 and 2008 as we seek to exploit opportunities for further growth and to<br />

deliver our award winning e-commerce solutions to the wider international market.<br />

The expected return on shareholders’ net assets amounts to £1m (2005: £1m).<br />

This comprises the return on the shareholders’ net assets held within the business<br />

consistent with the investment return assumptions used to calculate the embedded<br />

value at the start of the period.<br />

Operating expenses* have increased by 17% to £63m (2005: £54m) against an<br />

increase in PVNBP of 32%. The growth in expenses reflects the less mature nature of<br />

our International business, which is still building critical mass to support the growing<br />

portfolio of products, markets and customers. There is a firm focus on cost efficiency,<br />

with a number of initiatives under way which will contribute in 2007 and beyond. These<br />

include greater use of technology to improve service and reduce costs across the<br />

international markets in which we operate.<br />

Operating expenses<br />

2006 +17% £63m<br />

2005 £54m<br />

*Operating expenses exclude: commission, deferred acquisition cost adjustments, non-recurring items,<br />

investment fees, amortisation and impairment of intangibles and expenses of policyholder investments<br />

which are consolidated under IFRS.<br />

<strong>Friends</strong> Provident Annual Report & Accounts 2006 23