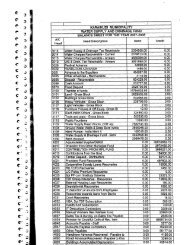

Gudiyattam Gudiyattam Town - Municipal

Gudiyattam Gudiyattam Town - Municipal

Gudiyattam Gudiyattam Town - Municipal

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Chapter ñ14 Final Report: <strong>Gudiyattam</strong> <strong>Municipal</strong>ity<br />

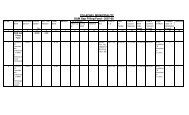

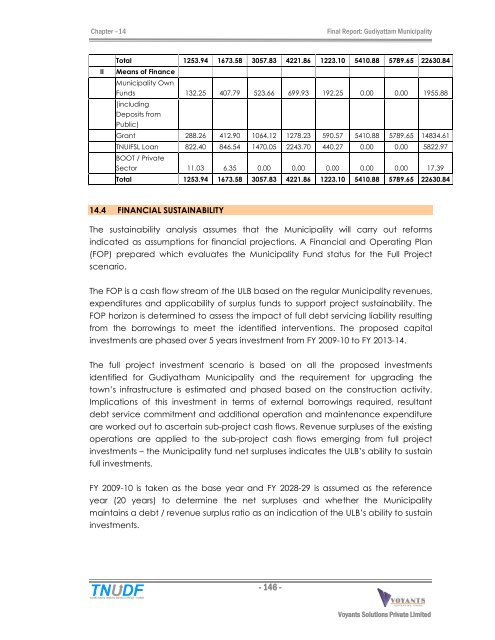

Total 1253.94 1673.58 3057.83 4221.86 1223.10 5410.88 5789.65 22630.84<br />

II Means of Finance<br />

<strong>Municipal</strong>ity Own<br />

Funds 132.25 407.79 523.66 699.93 192.25 0.00 0.00 1955.88<br />

(including<br />

Deposits from<br />

Public)<br />

Grant 288.26 412.90 1064.12 1278.23 590.57 5410.88 5789.65 14834.61<br />

TNUIFSL Loan 822.40 846.54 1470.05 2243.70 440.27 0.00 0.00 5822.97<br />

BOOT / Private<br />

Sector 11.03 6.35 0.00 0.00 0.00 0.00 0.00 17.39<br />

Total 1253.94 1673.58 3057.83 4221.86 1223.10 5410.88 5789.65 22630.84<br />

14.4 FINANCIAL SUSTAINABILITY<br />

The sustainability analysis assumes that the <strong>Municipal</strong>ity will carry out reforms<br />

indicated as assumptions for financial projections. A Financial and Operating Plan<br />

(FOP) prepared which evaluates the <strong>Municipal</strong>ity Fund status for the Full Project<br />

scenario.<br />

The FOP is a cash flow stream of the ULB based on the regular <strong>Municipal</strong>ity revenues,<br />

expenditures and applicability of surplus funds to support project sustainability. The<br />

FOP horizon is determined to assess the impact of full debt servicing liability resulting<br />

from the borrowings to meet the identified interventions. The proposed capital<br />

investments are phased over 5 years investment from FY 2009-10 to FY 2013-14.<br />

The full project investment scenario is based on all the proposed investments<br />

identified for Gudiyatham <strong>Municipal</strong>ity and the requirement for upgrading the<br />

townís infrastructure is estimated and phased based on the construction activity.<br />

Implications of this investment in terms of external borrowings required, resultant<br />

debt service commitment and additional operation and maintenance expenditure<br />

are worked out to ascertain sub-project cash flows. Revenue surpluses of the existing<br />

operations are applied to the sub-project cash flows emerging from full project<br />

investments ñ the <strong>Municipal</strong>ity fund net surpluses indicates the ULBís ability to sustain<br />

full investments.<br />

FY 2009-10 is taken as the base year and FY 2028-29 is assumed as the reference<br />

year (20 years) to determine the net surpluses and whether the <strong>Municipal</strong>ity<br />

maintains a debt / revenue surplus ratio as an indication of the ULBís ability to sustain<br />

investments.<br />

- 146 -<br />

Voyants Solutions Private Limited