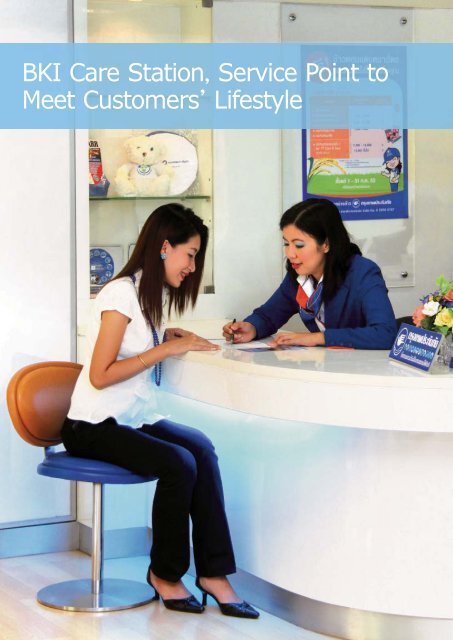

BKI Care Station, Service Po<strong>in</strong>t <strong>to</strong> Meet Cus<strong>to</strong>mersû Lifestyle

<strong>We</strong> <strong>aim</strong> <strong>to</strong> <strong>be</strong> <strong>the</strong> <strong>most</strong> <strong>preferred</strong> <strong>non</strong>-<strong>life</strong> <strong><strong>in</strong>surer</strong> <strong>in</strong> <strong>Thailand</strong> <strong>We</strong> provide our cus<strong>to</strong>mers with an added service channel through our BKI Care Station <strong>in</strong> shopp<strong>in</strong>g malls <strong>in</strong> order <strong>to</strong> respond <strong>to</strong> <strong>the</strong>ir demand for greater convenience, as well as <strong>to</strong> extend <strong>the</strong> companyûs reach <strong>to</strong> every s<strong>in</strong>gle cus<strong>to</strong>mer. THE THAI NON-LIFE INSURANCE INDUSTRY IN 2009 AND OUTLOOK FOR 2010 Market<strong>in</strong>g and Competition <strong>in</strong> 2009 In 2009, <strong>the</strong> overall Thai economy experienced a 2.3 percent negative growth rate, which directly impacted <strong>non</strong>-<strong>life</strong> <strong>in</strong>surance <strong>in</strong>dustry growth. A <strong>to</strong>tal direct written premium for <strong>the</strong> entire <strong>in</strong>dustry witnessed only a 3.4 percent growth rate, <strong>the</strong> lowest over <strong>the</strong> past ten years. Mo<strong>to</strong>r <strong>in</strong>surance, hav<strong>in</strong>g a high market share of 60.0 percent, was <strong>the</strong> <strong>most</strong> affected, hav<strong>in</strong>g a growth rate of only 2.0 percent, compared <strong>to</strong> 5.6 percent <strong>in</strong> 2008. Voluntary mo<strong>to</strong>r <strong>in</strong>surance, <strong>in</strong> particular, grew by 2.1 percent and 1.8 percent of Compulsory mo<strong>to</strong>r <strong>in</strong>surance, due <strong>to</strong> constant negative growth for <strong>to</strong>tal mo<strong>to</strong>r sales for <strong>the</strong> fourth consecutive year, with 10.8 percent negative growth <strong>in</strong> 2009. Mo<strong>to</strong>r markets for commercial vehicles had 17.9 percent negative growth (<strong>the</strong> highest over <strong>the</strong> past four years), while those for personal cars experienced only 1.4 percent growth, compared <strong>to</strong> 33.3 percent <strong>in</strong> 2008 (source: The Mo<strong>to</strong>r Industry Association). This was coupled with <strong>the</strong> fact that cus<strong>to</strong>mers had <strong>be</strong>come <strong>in</strong>creas<strong>in</strong>gly <strong>in</strong>terested <strong>in</strong> buy<strong>in</strong>g <strong>the</strong>ir mo<strong>to</strong>r <strong>in</strong>surance policies at an economical price, such as <strong>the</strong> “3 Plus” and “2 Plus” policies. In 2009, <strong>the</strong> loss ratio <strong>in</strong>curred by mo<strong>to</strong>r <strong>in</strong>surance slightly <strong>in</strong>creased <strong>to</strong> 57.0 percent, compared <strong>to</strong> 56.3 percent <strong>in</strong> 2008 although many <strong>non</strong>-<strong>life</strong> <strong>in</strong>surance companies gradually raised <strong>the</strong>ir Comprehensive mo<strong>to</strong>r <strong>in</strong>surance premium rate for cars of no more than 2,000 c.c. so that it was <strong>in</strong> accordance with ris<strong>in</strong>g bus<strong>in</strong>ess costs, both for those of spare parts and labour. In addition, a num<strong>be</strong>r of companies had issued new products <strong>to</strong> <strong>the</strong> market for personal accident <strong>in</strong>surance and health <strong>in</strong>surance <strong>in</strong> order <strong>to</strong> stimulate <strong>the</strong>ir sales due <strong>to</strong> a high market demand and higher frequency of accidents and malignant diseases. Meanwhile, <strong>the</strong>re was a slowdown <strong>in</strong> new <strong>in</strong>vestment projects. Dur<strong>in</strong>g 2009, miscellaneous <strong>in</strong>surance that experienced over 20.0 percent growth <strong>in</strong>cluded all risks <strong>in</strong>surance, eng<strong>in</strong>eer<strong>in</strong>g <strong>in</strong>surance, personal accident <strong>in</strong>surance and health <strong>in</strong>surance. In 2009, Bangkok Insurance Public Company Limited was no different from o<strong>the</strong>r <strong>non</strong>-<strong>life</strong> <strong>in</strong>surance companies affected by <strong>the</strong> economic crisis. Never<strong>the</strong>less, it had consistently adopted proactive strategies for personal l<strong>in</strong>e bus<strong>in</strong>ess over <strong>the</strong> past several years, coupled with cont<strong>in</strong>uously mak<strong>in</strong>g advertisements and public relations campaigns via a myriad of media over <strong>the</strong> past 3-4 years, enabl<strong>in</strong>g consumers <strong>to</strong> know and remem<strong>be</strong>r more about <strong>the</strong> Company’s name. Besides, <strong>the</strong> Company issued such new products as “ Comprehensive Value Package” a Comprehensive mo<strong>to</strong>r <strong>in</strong>surance policy and “The Value Packages” <strong>in</strong>surance policy called, “4 - Classic Diseases” package, and “Salary Man” package, both of which satisfac<strong>to</strong>rily attracted new cus<strong>to</strong>mers. Due <strong>to</strong> <strong>the</strong> Company’s proactive strategies and new policies, <strong>the</strong> Company could, <strong>in</strong> 2009, expand over 30.0 percent of its personal cus<strong>to</strong>mer market, with an <strong>in</strong>crease of over 40.0 percent of new cus<strong>to</strong>mers, ma<strong>in</strong>ly via <strong>the</strong> Telemarket<strong>in</strong>g and Bancassurance channels. For its services, <strong>the</strong> Company has speeded up its development of and <strong>in</strong>crease <strong>in</strong> <strong>the</strong> num<strong>be</strong>r of garages participat<strong>in</strong>g <strong>in</strong> <strong>the</strong> “Bangkok Insurance Recommended Garage” project and those fix<strong>in</strong>g cars on contracts, both <strong>in</strong> Bangkok and upcountry, <strong>in</strong> order <strong>to</strong> provide convenience <strong>to</strong> its cus<strong>to</strong>mers. Fur<strong>the</strong>rmore, <strong>the</strong> Company lends support <strong>to</strong> its bus<strong>in</strong>ess partners’ performance so that <strong>the</strong>y are able <strong>to</strong> use <strong>the</strong> Company’s work system <strong>to</strong> carry out <strong>the</strong>ir underwrit<strong>in</strong>g work and issue policies with convenience and swiftness. Through <strong>the</strong> Company’s aforementioned operational strategies, its direct written premium <strong>in</strong> 2009 experienced higher growth than <strong>the</strong> def<strong>in</strong>ed target of 14.2 percent. The four ma<strong>in</strong> classes of <strong>in</strong>surance achiev<strong>in</strong>g a high growth rate <strong>in</strong>cluded fire <strong>in</strong>surance, mar<strong>in</strong>e <strong>in</strong>surance, mo<strong>to</strong>r <strong>in</strong>surance and miscellaneous <strong>in</strong>surance, result<strong>in</strong>g <strong>in</strong> <strong>the</strong> Company’s rise <strong>in</strong> <strong>the</strong> overall market share from 6.5 percent <strong>in</strong> 2008 <strong>to</strong> 7.1 percent <strong>in</strong> 2009. 11