Global Steel Trade; Structural Problems and Future Solutions

Global Steel Trade; Structural Problems and Future Solutions

Global Steel Trade; Structural Problems and Future Solutions

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Production Links. A second cause of the fall in domestic dem<strong>and</strong> was the dislocation <strong>and</strong> breakdown in<br />

existing production links. Under the planned economy, large-scale companies specialized in particular<br />

aspects of production <strong>and</strong> were linked to specific upstream suppliers <strong>and</strong> downstream customers. For<br />

instance, iron ore from Ukraine was shipped to Russia to make sheet, which was then shipped back to<br />

Ukraine to make pipe. 7 After the breakup of the Soviet Union, the old suppliers <strong>and</strong> customers were<br />

sometimes no longer in the same country, <strong>and</strong> customs duties <strong>and</strong> trade barriers were erected where none<br />

had previously existed.<br />

At the same time, the other countries of the former Soviet Union, which had been major consumers of<br />

Russian steel, were also going through economic transition <strong>and</strong> a decline in steel consumption of their<br />

own, <strong>and</strong> unlike other export markets, often could not pay cash. 8 In 1990, non-Russian republics of<br />

the Soviet Union accounted for 70 percent of Russia’s sales; by 1995, this figure had dropped to 6<br />

percent. 9<br />

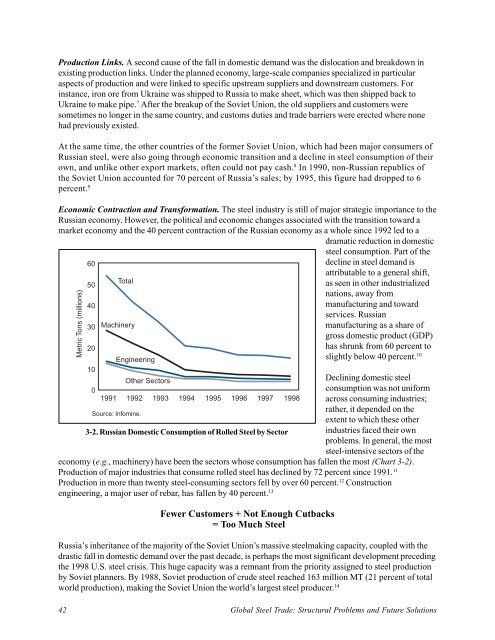

Economic Contraction <strong>and</strong> Transformation. The steel industry is still of major strategic importance to the<br />

Russian economy. However, the political <strong>and</strong> economic changes associated with the transition toward a<br />

market economy <strong>and</strong> the 40 percent contraction of the Russian economy as a whole since 1992 led to a<br />

dramatic reduction in domestic<br />

steel consumption. Part of the<br />

60<br />

decline in steel dem<strong>and</strong> is<br />

attributable to a general shift,<br />

50<br />

40<br />

Total<br />

as seen in other industrialized<br />

nations, away from<br />

manufacturing <strong>and</strong> toward<br />

30<br />

20<br />

Machinery<br />

services. Russian<br />

manufacturing as a share of<br />

gross domestic product (GDP)<br />

has shrunk from 60 percent to<br />

slightly below 40 percent. 10<br />

Metric Tons (millions)<br />

10<br />

Engineering<br />

Other Sectors<br />

Declining domestic steel<br />

0<br />

consumption was not uniform<br />

1991 1992 1993 1994 1995 1996 1997 1998 across consuming industries;<br />

rather, it depended on the<br />

Source: Infomine.<br />

extent to which these other<br />

3-2. Russian Domestic Consumption of Rolled <strong>Steel</strong> by Sector industries faced their own<br />

problems. In general, the most<br />

steel-intensive sectors of the<br />

economy (e.g., machinery) have been the sectors whose consumption has fallen the most (Chart 3-2).<br />

Production of major industries that consume rolled steel has declined by 72 percent since 1991. 11<br />

Production in more than twenty steel-consuming sectors fell by over 60 percent. 12 Construction<br />

engineering, a major user of rebar, has fallen by 40 percent. 13<br />

Fewer Customers + Not Enough Cutbacks<br />

= Too Much <strong>Steel</strong><br />

Russia’s inheritance of the majority of the Soviet Union’s massive steelmaking capacity, coupled with the<br />

drastic fall in domestic dem<strong>and</strong> over the past decade, is perhaps the most significant development preceding<br />

the 1998 U.S. steel crisis. This huge capacity was a remnant from the priority assigned to steel production<br />

by Soviet planners. By 1988, Soviet production of crude steel reached 163 million MT (21 percent of total<br />

world production), making the Soviet Union the world’s largest steel producer. 14<br />

42 <strong>Global</strong> <strong>Steel</strong> <strong>Trade</strong>: <strong>Structural</strong> <strong>Problems</strong> <strong>and</strong> <strong>Future</strong> <strong>Solutions</strong>