Global Steel Trade; Structural Problems and Future Solutions

Global Steel Trade; Structural Problems and Future Solutions

Global Steel Trade; Structural Problems and Future Solutions

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

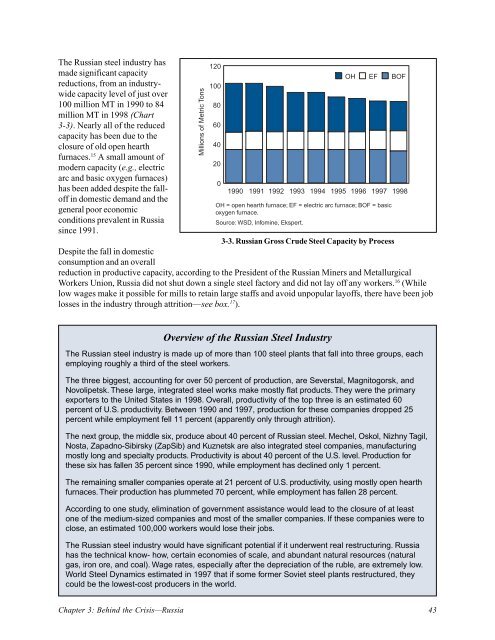

The Russian steel industry has<br />

made significant capacity<br />

reductions, from an industrywide<br />

capacity level of just over<br />

100 million MT in 1990 to 84<br />

million MT in 1998 (Chart<br />

3-3). Nearly all of the reduced<br />

capacity has been due to the<br />

closure of old open hearth<br />

furnaces. 15 A small amount of<br />

modern capacity (e.g., electric<br />

arc <strong>and</strong> basic oxygen furnaces)<br />

has been added despite the falloff<br />

in domestic dem<strong>and</strong> <strong>and</strong> the<br />

general poor economic<br />

conditions prevalent in Russia<br />

since 1991.<br />

Millions of Metric Tons<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

OH EF BOF<br />

1990 1991 1992 1993 1994 1995 1996 1997 1998<br />

OH = open hearth furnace; EF = electric arc furnace; BOF = basic<br />

oxygen furnace.<br />

Source: WSD, Infomine, Ekspert.<br />

3-3. Russian Gross Crude <strong>Steel</strong> Capacity by Process<br />

Despite the fall in domestic<br />

consumption <strong>and</strong> an overall<br />

reduction in productive capacity, according to the President of the Russian Miners <strong>and</strong> Metallurgical<br />

Workers Union, Russia did not shut down a single steel factory <strong>and</strong> did not lay off any workers. 16 (While<br />

low wages make it possible for mills to retain large staffs <strong>and</strong> avoid unpopular layoffs, there have been job<br />

losses in the industry through attrition—see box. 17 ).<br />

Overview of the Russian <strong>Steel</strong> Industry<br />

The Russian steel industry is made up of more than 100 steel plants that fall into three groups, each<br />

employing roughly a third of the steel workers.<br />

The three biggest, accounting for over 50 percent of production, are Severstal, Magnitogorsk, <strong>and</strong><br />

Novolipetsk. These large, integrated steel works make mostly flat products. They were the primary<br />

exporters to the United States in 1998. Overall, productivity of the top three is an estimated 60<br />

percent of U.S. productivity. Between 1990 <strong>and</strong> 1997, production for these companies dropped 25<br />

percent while employment fell 11 percent (apparently only through attrition).<br />

The next group, the middle six, produce about 40 percent of Russian steel. Mechel, Oskol, Nizhny Tagil,<br />

Nosta, Zapadno-Sibirsky (ZapSib) <strong>and</strong> Kuznetsk are also integrated steel companies, manufacturing<br />

mostly long <strong>and</strong> specialty products. Productivity is about 40 percent of the U.S. level. Production for<br />

these six has fallen 35 percent since 1990, while employment has declined only 1 percent.<br />

The remaining smaller companies operate at 21 percent of U.S. productivity, using mostly open hearth<br />

furnaces. Their production has plummeted 70 percent, while employment has fallen 28 percent.<br />

According to one study, elimination of government assistance would lead to the closure of at least<br />

one of the medium-sized companies <strong>and</strong> most of the smaller companies. If these companies were to<br />

close, an estimated 100,000 workers would lose their jobs.<br />

The Russian steel industry would have significant potential if it underwent real restructuring. Russia<br />

has the technical know- how, certain economies of scale, <strong>and</strong> abundant natural resources (natural<br />

gas, iron ore, <strong>and</strong> coal). Wage rates, especially after the depreciation of the ruble, are extremely low.<br />

World <strong>Steel</strong> Dynamics estimated in 1997 that if some former Soviet steel plants restructured, they<br />

could be the lowest-cost producers in the world.<br />

Chapter 3: Behind the Crisis—Russia 43