Annual Report - VÃB banka

Annual Report - VÃB banka

Annual Report - VÃB banka

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

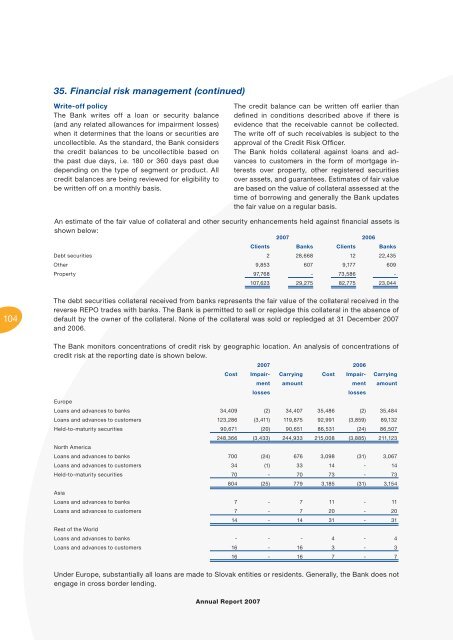

35. Financial risk management (continued)<br />

Write-off policy<br />

The Bank writes off a loan or security balance<br />

(and any related allowances for impairment losses)<br />

when it determines that the loans or securities are<br />

uncollectible. As the standard, the Bank considers<br />

the credit balances to be uncollectible based on<br />

the past due days, i.e. 180 or 360 days past due<br />

depending on the type of segment or product. All<br />

credit balances are being reviewed for eligibility to<br />

be written off on a monthly basis.<br />

The credit balance can be written off earlier than<br />

defi ned in conditions described above if there is<br />

evidence that the receivable cannot be collected.<br />

The write off of such receivables is subject to the<br />

approval of the Credit Risk Offi cer.<br />

The Bank holds collateral against loans and advances<br />

to customers in the form of mortgage interests<br />

over property, other registered securities<br />

over assets, and guarantees. Estimates of fair value<br />

are based on the value of collateral assessed at the<br />

time of borrowing and generally the Bank updates<br />

the fair value on a regular basis.<br />

An estimate of the fair value of collateral and other security enhancements held against fi nancial assets is<br />

shown below:<br />

2007 2006<br />

Clients Banks Clients Banks<br />

Debt securities 2 28,668 12 22,435<br />

Other 9,853 607 9,177 609<br />

Property 97,768 - 73,586 -<br />

107,623 29,275 82,775 23,044<br />

104<br />

The debt securities collateral received from banks represents the fair value of the collateral received in the<br />

reverse REPO trades with banks. The Bank is permitted to sell or repledge this collateral in the absence of<br />

default by the owner of the collateral. None of the collateral was sold or repledged at 31 December 2007<br />

and 2006.<br />

The Bank monitors concentrations of credit risk by geographic location. An analysis of concentrations of<br />

credit risk at the reporting date is shown below.<br />

2007 2006<br />

Cost Impair- Carrying Cost Impair- Carrying<br />

ment amount ment amount<br />

losses<br />

losses<br />

Europe<br />

Loans and advances to banks 34,409 (2) 34,407 35,486 (2) 35,484<br />

Loans and advances to customers 123,286 (3,411) 119,875 92,991 (3,859) 89,132<br />

Held-to-maturity securities 90,671 (20) 90,651 86,531 (24) 86,507<br />

248,366 (3,433) 244,933 215,008 (3,885) 211,123<br />

North America<br />

Loans and advances to banks 700 (24) 676 3,098 (31) 3,067<br />

Loans and advances to customers 34 (1) 33 14 - 14<br />

Held-to-maturity securities 70 - 70 73 - 73<br />

804 (25) 779 3,185 (31) 3,154<br />

Asia<br />

Loans and advances to banks 7 - 7 11 - 11<br />

Loans and advances to customers 7 - 7 20 - 20<br />

14 - 14 31 - 31<br />

Rest of the World<br />

Loans and advances to banks - - - 4 - 4<br />

Loans and advances to customers 16 - 16 3 - 3<br />

16 - 16 7 - 7<br />

Under Europe, substantially all loans are made to Slovak entities or residents. Generally, the Bank does not<br />

engage in cross border lending.<br />

<strong>Annual</strong> <strong>Report</strong> 2007