Clock - Uranium Supply Crunch and Critical ... - Andrew Johns

Clock - Uranium Supply Crunch and Critical ... - Andrew Johns

Clock - Uranium Supply Crunch and Critical ... - Andrew Johns

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

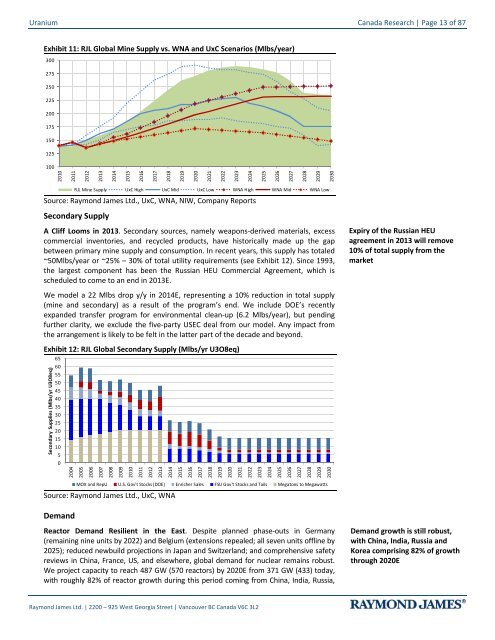

<strong>Uranium</strong> Canada Research | Page 13 of 87Exhibit 11: RJL Global Mine <strong>Supply</strong> vs. WNA <strong>and</strong> UxC Scenarios (Mlbs/year)300275250225200175150125100201020112012201320142015201620172018201920202021202220232024202520262027202820292030RJL Mine <strong>Supply</strong> UxC High UxC Mid UxC Low WNA High WNA Mid WNA LowSource: Raymond James Ltd., UxC, WNA, NIW, Company ReportsSecondary <strong>Supply</strong>A Cliff Looms in 2013. Secondary sources, namely weapons-derived materials, excesscommercial inventories, <strong>and</strong> recycled products, have historically made up the gapbetween primary mine supply <strong>and</strong> consumption. In recent years, this supply has totaled~50Mlbs/year or ~25% – 30% of total utility requirements (see Exhibit 12). Since 1993,the largest component has been the Russian HEU Commercial Agreement, which isscheduled to come to an end in 2013E.Expiry of the Russian HEUagreement in 2013 will remove10% of total supply from themarketWe model a 22 Mlbs drop y/y in 2014E, representing a 10% reduction in total supply(mine <strong>and</strong> secondary) as a result of the program’s end. We include DOE’s recentlyexp<strong>and</strong>ed transfer program for environmental clean-up (6.2 Mlbs/year), but pendingfurther clarity, we exclude the five-party USEC deal from our model. Any impact fromthe arrangement is likely to be felt in the latter part of the decade <strong>and</strong> beyond.Exhibit 12: RJL Global Secondary <strong>Supply</strong> (Mlbs/yr U3O8eq)65Secondary Supplies (Mlbs/yr U3O8eq)605550454035302520151050200420052006200720082009201020112012201320142015201620172018201920202021202220232024202520262027202820292030MOX <strong>and</strong> RepU U.S. Gov't Stocks (DOE) Enricher Sales FSU Gov't Stocks <strong>and</strong> Tails Megatons to MegawattsSource: Raymond James Ltd., UxC, WNADem<strong>and</strong>Reactor Dem<strong>and</strong> Resilient in the East. Despite planned phase-outs in Germany(remaining nine units by 2022) <strong>and</strong> Belgium (extensions repealed; all seven units offline by2025); reduced newbuild projections in Japan <strong>and</strong> Switzerl<strong>and</strong>; <strong>and</strong> comprehensive safetyreviews in China, France, US, <strong>and</strong> elsewhere, global dem<strong>and</strong> for nuclear remains robust.We project capacity to reach 487 GW (570 reactors) by 2020E from 371 GW (433) today,with roughly 82% of reactor growth during this period coming from China, India, Russia,Dem<strong>and</strong> growth is still robust,with China, India, Russia <strong>and</strong>Korea comprising 82% of growththrough 2020ERaymond James Ltd. | 2200 – 925 West Georgia Street | Vancouver BC Canada V6C 3L2