World Investment Report 2009: Transnational Corporations - Unctad

World Investment Report 2009: Transnational Corporations - Unctad

World Investment Report 2009: Transnational Corporations - Unctad

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

122 <strong>World</strong> <strong>Investment</strong> <strong>Report</strong> <strong>2009</strong>: <strong>Transnational</strong> <strong>Corporations</strong>, Agricultural Production and Development<br />

towards ensuring food security for their populations.<br />

In fact, historically there has been a recurring cycle<br />

of reliance on foreign investment in agriculture. 43<br />

However, inasmuch as the recent food crisis seems<br />

to be the result of a confluence of factors, the drivers<br />

of food-security-related FDI may be less volatile than<br />

before.<br />

Until recently, the availability of underutilized<br />

agricultural land was seen as perhaps the main hostcountry<br />

factor driving for food-security-related FDI<br />

in agriculture (Woertz et al, 2008). However, it is<br />

now increasingly recognized that perhaps the most<br />

crucial factor or driver is not land per se, but rather<br />

the availability of water resources to irrigate the<br />

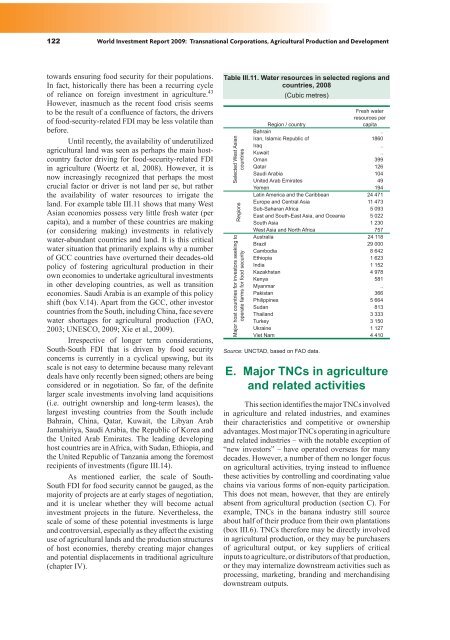

land. For example table III.11 shows that many West<br />

Asian economies possess very little fresh water (per<br />

capita), and a number of these countries are making<br />

(or considering making) investments in relatively<br />

water-abundant countries and land. It is this critical<br />

water situation that primarily explains why a number<br />

of GCC countries have overturned their decades-old<br />

policy of fostering agricultural production in their<br />

own economies to undertake agricultural investments<br />

in other developing countries, as well as transition<br />

economies. Saudi Arabia is an example of this policy<br />

shift (box V.14). Apart from the GCC, other investor<br />

countries from the South, including China, face severe<br />

water shortages for agricultural production (FAO,<br />

2003; UNESCO, <strong>2009</strong>; Xie et al., <strong>2009</strong>).<br />

Irrespective of longer term considerations,<br />

South-South FDI that is driven by food security<br />

concerns is currently in a cyclical upswing, but its<br />

scale is not easy to determine because many relevant<br />

deals have only recently been signed; others are being<br />

considered or in negotiation. So far, of the definite<br />

larger scale investments involving land acquisitions<br />

(i.e. outright ownership and long-term leases), the<br />

largest investing countries from the South include<br />

Bahrain, China, Qatar, Kuwait, the Libyan Arab<br />

Jamahiriya, Saudi Arabia, the Republic of Korea and<br />

the United Arab Emirates. The leading developing<br />

host countries are in Africa, with Sudan, Ethiopia, and<br />

the United Republic of Tanzania among the foremost<br />

recipients of investments (figure III.14).<br />

As mentioned earlier, the scale of South-<br />

South FDI for food security cannot be gauged, as the<br />

majority of projects are at early stages of negotiation,<br />

and it is unclear whether they will become actual<br />

investment projects in the future. Nevertheless, the<br />

scale of some of these potential investments is large<br />

and controversial, especially as they affect the existing<br />

use of agricultural lands and the production structures<br />

of host economies, thereby creating major changes<br />

and potential displacements in traditional agriculture<br />

(chapter IV).<br />

Table III.11. Water resources in selected regions and<br />

countries, 2008<br />

(Cubic metres)<br />

Selected West Asian<br />

countries<br />

Regions<br />

Major host countries for investors seeking to<br />

operate farms for food security<br />

Region / country<br />

Fresh water<br />

resources per<br />

capita<br />

Bahrain ..<br />

Iran, Islamic Republic of 1860<br />

Iraq ..<br />

Kuwait ..<br />

Oman 399<br />

Qatar 126<br />

Saudi Arabia 104<br />

United Arab Emirates 49<br />

Yemen 194<br />

Latin America and the Caribbean 24 471<br />

Europe and Central Asia 11 473<br />

Sub-Saharan Africa 5 093<br />

East and South-East Asia, and Oceania 5 022<br />

South Asia 1 230<br />

West Asia and North Africa 757<br />

Australia 24 118<br />

Brazil 29 000<br />

Cambodia 8 642<br />

Ethiopia 1 623<br />

India 1 152<br />

Kazakhstan 4 978<br />

Kenya 581<br />

Myanmar ..<br />

Pakistan 366<br />

Philippines 5 664<br />

Sudan 813<br />

Thailand 3 333<br />

Turkey 3 150<br />

Ukraine 1 127<br />

Viet Nam 4 410<br />

Source: UNCTAD, based on FAO data.<br />

E. Major TNCs in agriculture<br />

and related activities<br />

This section identifies the major TNCs involved<br />

in agriculture and related industries, and examines<br />

their characteristics and competitive or ownership<br />

advantages. Most major TNCs operating in agriculture<br />

and related industries – with the notable exception of<br />

“new investors” – have operated overseas for many<br />

decades. However, a number of them no longer focus<br />

on agricultural activities, trying instead to influence<br />

these activities by controlling and coordinating value<br />

chains via various forms of non-equity participation.<br />

This does not mean, however, that they are entirely<br />

absent from agricultural production (section C). For<br />

example, TNCs in the banana industry still source<br />

about half of their produce from their own plantations<br />

(box III.6). TNCs therefore may be directly involved<br />

in agricultural production, or they may be purchasers<br />

of agricultural output, or key suppliers of critical<br />

inputs to agriculture, or distributors of that production,<br />

or they may internalize downstream activities such as<br />

processing, marketing, branding and merchandising<br />

downstream outputs.