FEDERAL

Sixth Semiannual Report to the Congress - Federal Housing ...

Sixth Semiannual Report to the Congress - Federal Housing ...

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

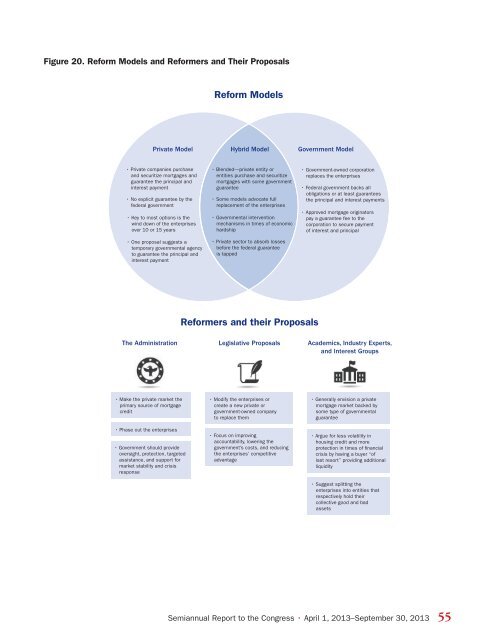

Figure 20. Reform Models and Reformers and Their Proposals<br />

Reform Models<br />

Private Model<br />

Hybrid Model<br />

Government Model<br />

• Private companies purchase<br />

and securitize mortgages and<br />

guarantee the principal and<br />

interest payment<br />

• No explicit guarantee by the<br />

federal government<br />

• Key to most options is the<br />

wind down of the enterprises<br />

over 10 or 15 years<br />

• One proposal suggests a<br />

temporary governmental agency<br />

to guarantee the principal and<br />

interest payment<br />

• Blended—private entity or<br />

entities purchase and securitize<br />

mortgages with some government<br />

guarantee<br />

• Some models advocate full<br />

replacement of the enterprises<br />

• Governmental intervention<br />

mechanisms in times of economic<br />

hardship<br />

• Private sector to absorb losses<br />

before the federal guarantee<br />

is tapped<br />

• Government-owned corporation<br />

replaces the enterprises<br />

• Federal government backs all<br />

obligations or at least guarantees<br />

the principal and interest payments<br />

• Approved mortgage originators<br />

pay a guarantee fee to the<br />

corporation to secure payment<br />

of interest and principal<br />

Reformers and their Proposals<br />

The Administration Legislative Proposals Academics, Industry Experts,<br />

and Interest Groups<br />

• Make the private market the<br />

primary source of mortgage<br />

credit<br />

• Phase out the enterprises<br />

• Government should provide<br />

oversight, protection, targeted<br />

assistance, and support for<br />

market stability and crisis<br />

response<br />

• Modify the enterprises or<br />

create a new private or<br />

government-owned company<br />

to replace them<br />

• Focus on improving<br />

accountability, lowering the<br />

government’s costs, and reducing<br />

the enterprises’ competitive<br />

advantage<br />

• Generally envision a private<br />

mortgage market backed by<br />

some type of governmental<br />

guarantee<br />

• Argue for less volatility in<br />

housing credit and more<br />

protection in times of financial<br />

crisis by having a buyer “of<br />

last resort” providing additional<br />

liquidity<br />

• Suggest splitting the<br />

enterprises into entities that<br />

respectively hold their<br />

collective good and bad<br />

assets<br />

Semiannual Report to the Congress • April 1, 2013–September 30, 2013 55