FEDERAL

Sixth Semiannual Report to the Congress - Federal Housing ...

Sixth Semiannual Report to the Congress - Federal Housing ...

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Even though the FHFA senior examiner raised<br />

concerns about Freddie Mac’s loan review<br />

process more than six months before the agency<br />

approved the Bank of America settlement, FHFA<br />

did not timely act on or test the ramifications<br />

of the examiner’s concerns before approving the<br />

settlement. Instead, the agency relied on the<br />

enterprise’s analysis of the settlement without testing<br />

its underlying assumptions. 168<br />

After we issued our report, Freddie Mac changed<br />

its loan review process for repurchase claims. The<br />

enterprise now reviews all nonperforming loans<br />

originated between 2004 and 2007 for repurchase<br />

claims without regard to when they defaulted. We<br />

found in a follow-up report that such an expanded<br />

review may generate as much as $3.4 billion in<br />

additional revenue for Freddie Mac. 169<br />

Going forward, FHFA has generally agreed with our<br />

recommendations to take a more proactive oversight<br />

stance in response to the issues our work has raised.<br />

We believe these positive steps will help the agency<br />

identify and manage risks, but we have also found<br />

that this must be accompanied by a steadfast will to<br />

enforce compliance.<br />

Enforce: Ensuring Regulatory Compliance<br />

Even when FHFA has identified risks and<br />

taken steps to manage them, the agency has not<br />

consistently enforced its directives to ensure that<br />

identified risks are, in fact, adequately addressed.<br />

As conservator and regulator, the agency’s authority<br />

over the enterprises is broad and includes the ability<br />

to enforce compliance with agency mandates.<br />

We have reported that FHFA’s supervision and<br />

regulation of the GSEs could be strengthened by<br />

better exercising this authority when warranted.<br />

For example, we determined that FHFA had<br />

not compelled Fannie Mae to comply with the<br />

requirement to have an effective program to manage<br />

operational risk—i.e., the risk of loss resulting from<br />

failed people, processes, systems, or external events.<br />

Effective operational risk management can help<br />

agency examiners to identify trends in such risks and<br />

focus their examinations accordingly. 170<br />

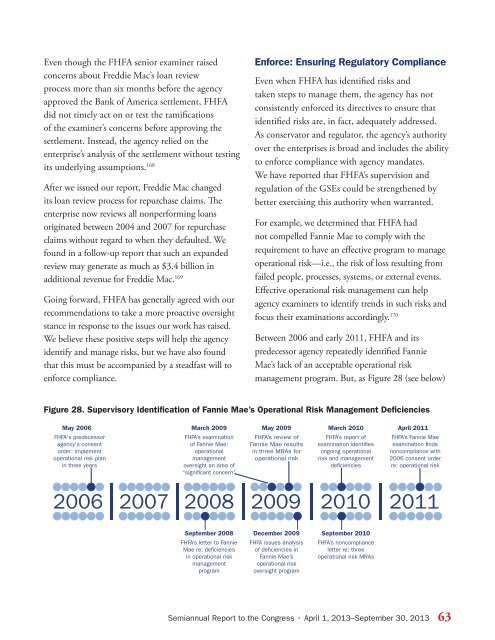

Between 2006 and early 2011, FHFA and its<br />

predecessor agency repeatedly identified Fannie<br />

Mae’s lack of an acceptable operational risk<br />

management program. But, as Figure 28 (see below)<br />

Figure 28. Supervisory Identification of Fannie Mae’s Operational Risk Management Deficiencies<br />

May 2006<br />

FHFA's predecessor<br />

agency's consent<br />

order: implement<br />

operational risk plan<br />

in three years<br />

March 2009<br />

FHFA’s examination<br />

of Fannie Mae:<br />

operational<br />

management<br />

oversight an area of<br />

“significant concern”<br />

May 2009<br />

FHFA’s review of<br />

Fannie Mae results<br />

in three MRAs for<br />

operational risk<br />

March 2010<br />

FHFA’s report of<br />

examination identifies<br />

ongoing operational<br />

risk and management<br />

deficiencies<br />

April 2011<br />

FHFA’s Fannie Mae<br />

examination finds<br />

noncompliance with<br />

2006 consent order<br />

re: operational risk<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

September 2008<br />

FHFA’s letter to Fannie<br />

Mae re: deficiencies<br />

in operational risk<br />

management<br />

program<br />

December 2009<br />

FHFA issues analysis<br />

of deficiencies in<br />

Fannie Mae’s<br />

operational risk<br />

oversight program<br />

September 2010<br />

FHFA’s noncompliance<br />

letter re: three<br />

operational risk MRAs<br />

Semiannual Report to the Congress • April 1, 2013–September 30, 2013 63