I Fiance Apicultural

I Fiance Apicultural

I Fiance Apicultural

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

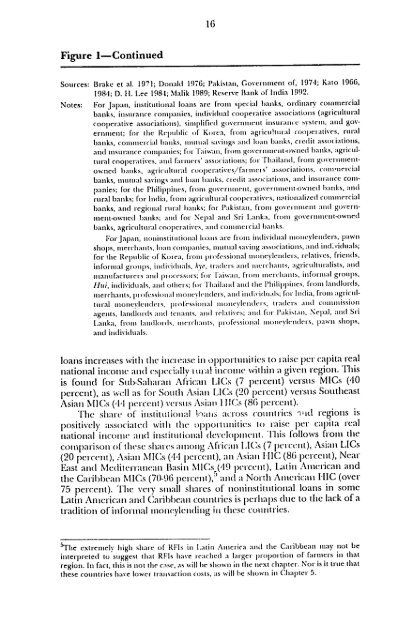

Figure 1-Continued<br />

16<br />

Sources: Brake et al.1971; Donald 1976; Pakistan, Government of, 1974; Kato 1966,<br />

1984; D. 1.Lee 198-1; Malik 1989; Reserve Bank of India 1992.<br />

Notes: For Japan, institutional loans are from special banks, ordinary commercial<br />

banks, insurance companies, individual cooperative associations (agricultural<br />

cooplerative associations), simplified government ilsuraitc system, and governnlent;<br />

for the Republic of Korea. from agricihmtal coopeiatives, rural<br />

banks, comoniercial banks, nmutial savings and loan banks, credit associatiois,<br />

attd insurance collima Iies; for Taiwan, fom goverinent-owne banks, agricultural<br />

cOoleratives. and failters' associations; folThailand, from goverlllitelitowned<br />

banks, agriculral cooperatives/fariltels' ssociations. commnercial<br />

banks, iuttal savings and luoa banks, ciedit associations, and insurance coimpanies;<br />

for the Philippines, from government, govcrnment-owned banks, and<br />

rural banks; for India, fiom agricutiural cooperatives, n:iiomtalized commercial<br />

banks, and regional rural batnks; for Pakistan, f|oni govelintent and governand<br />

Sri Lanka, from govetinment-owned<br />

nent-owned banks; and for Nepal<br />

banks, agricultural cooperatives, anid commeircial banks.<br />

For Japan, noninstittitional loans are frloin individual moneylenders, pawn<br />

shops, merchants, loan companies, mnutual saving associations, and individuals;<br />

for the Republic of Korea, fiom professionial illonieyleindels, relatives, friends.<br />

informal groups, individuals, kye, traders and nltmeclranits, agriculturalists, and<br />

itliilfacillels alldpilocessots; for l'aiwan, fronm Illechallts. ilnfollmal glollps,<br />

1h0,individuals, and others; fboThailand and the Phhilippines, fronm landlords,<br />

merchants, piofessionl toncylendels, and inldividitals; for India, fromi agriciil<br />

tilllal inoneltclideis, piofessiotial tonevlenders, timrcrs and conimission<br />

agents, landlords aind icianis, and relatives; aind for 'akistan, Nepal, and Sri<br />

Lanka, fronm landlords, iechatits, plofessional iioiyleldels, iawi shops,<br />

and individuals.<br />

loans increases withlieh inciease inop)portiities to iaise per capita real<br />

national income and espleci:lly til incoeie within a given region. This<br />

is foulnd foi" Stlb-Sahaiaii Afican LICs (7 p)erCent) versus MICs (40<br />

percent), as well as for Soith Asian LICs (20 peicent) versus Southeast<br />

Asian MICs (H1 )ercent) verstis Asiats I lTCs (86 percent).<br />

The shalt of itistittoliollal i.alis across countiries Ilid regions is<br />

positively associated with Ile oppotunitics to raise per capita real<br />

national incoie and institt ional devclopltlcit. This follows from tle<br />

copiarison of these sharcs aitiong Afiican Ll(]s (7 )etclcnt), Asian LICs<br />

(20 peicent), Asian MICs ('IH per'ct), an Asian [IC (86 percent), Near-<br />

East and Mediterranean Basin MICs ('19 )erceit), Liatin Anmican and<br />

the Caiihhean MICs (70-96 percent),' and a North Anericai HIC (over<br />

75 percent). The very small shares of noninstitutional loans in some<br />

Latin Ancrtican and (aribhcan counties is perhaps (luc to the lack of a<br />

tradition of informal tnoneylentding in these contitries.<br />

5 Thte extremely high share of RFIs in latin Ainerica and the Caribbean nay iot be<br />

in that<br />

interpreted to suggest that RFls have leached a larger propoitioni of farmers<br />

region. It fact, this is not the case, as will lie shown in tile next chapter. Nor is it true that<br />

these count ries have lower traisaction costs, as willIe shown illClhapter 5.